October nonfarm payrolls report, plus Goldman cuts 2023 EPS forecast to 0%, no stress in credit, Marty Zweig's rules, and the week in review

The Sandbox Daily (11.4.2022)

Welcome, Sandbox friends.

Today’s Daily discusses the October nonfarm payrolls report, Goldman Sachs cuts their 2023 S&P 500 EPS growth forecast to 0%, no stress in credit spreads, Marty Zweig’s investing rules, and a brief recap to snapshot the week in markets.

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +1.56% | S&P 500 +1.36% | Dow +1.26% | Russell 2000 +1.13%

FIXED INCOME: Barclays Agg Bond -0.01% | High Yield +0.69% | 2yr UST 4.658% | 10yr UST 4.163%

COMMODITIES: Brent Crude +4.31% to $98.75/barrel. Gold +2.80% to $1,676.6/oz.

BITCOIN: +4.43% to $21,168

US DOLLAR INDEX: -1.90% to 110.788

CBOE EQUITY PUT/CALL RATIO: 0.69

VIX: -2.96% to 24.55

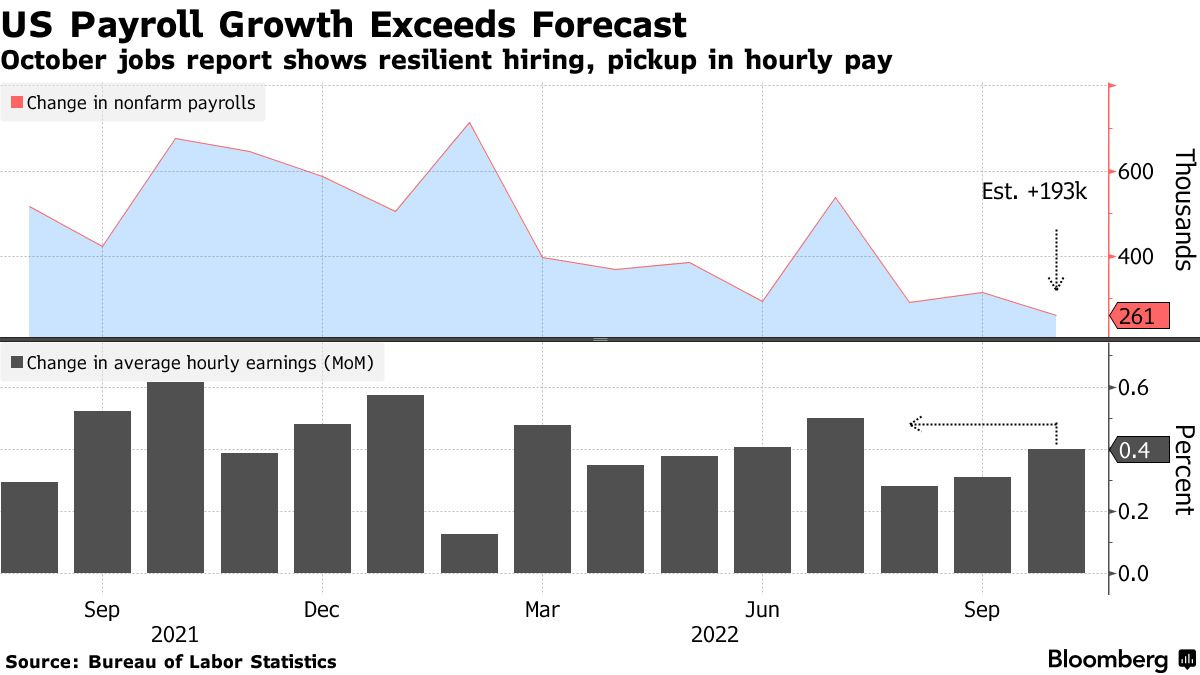

October nonfarm payrolls report show payrolls surged by 261k while unemployment rate rises to 3.7%

U.S. businesses reported strong hiring and wage increases in October although the unemployment rate climbed, offering a mixed picture as Federal Reserve officials debate how long to extend their campaign to curb elevated inflation. Markets responded positively to the report.

Nonfarm payrolls jumped by 261,000 in October - the slowest monthly gain since December 2020 when the economy outright shed jobs – though still above the consensus of 205,000. Additionally, the prior two months were revised up by 29,000. Monthly wages rose +0.4%, but the YoY change matched expectations of +4.7%, down from +5.0% in September. And the unemployment rate bounced back to August’s level of 3.7% after taking a quick detour to 3.5%. Continued tight labor market conditions will keep the Fed on its hiking path, but could allow for a downshift to 50 bp in December.

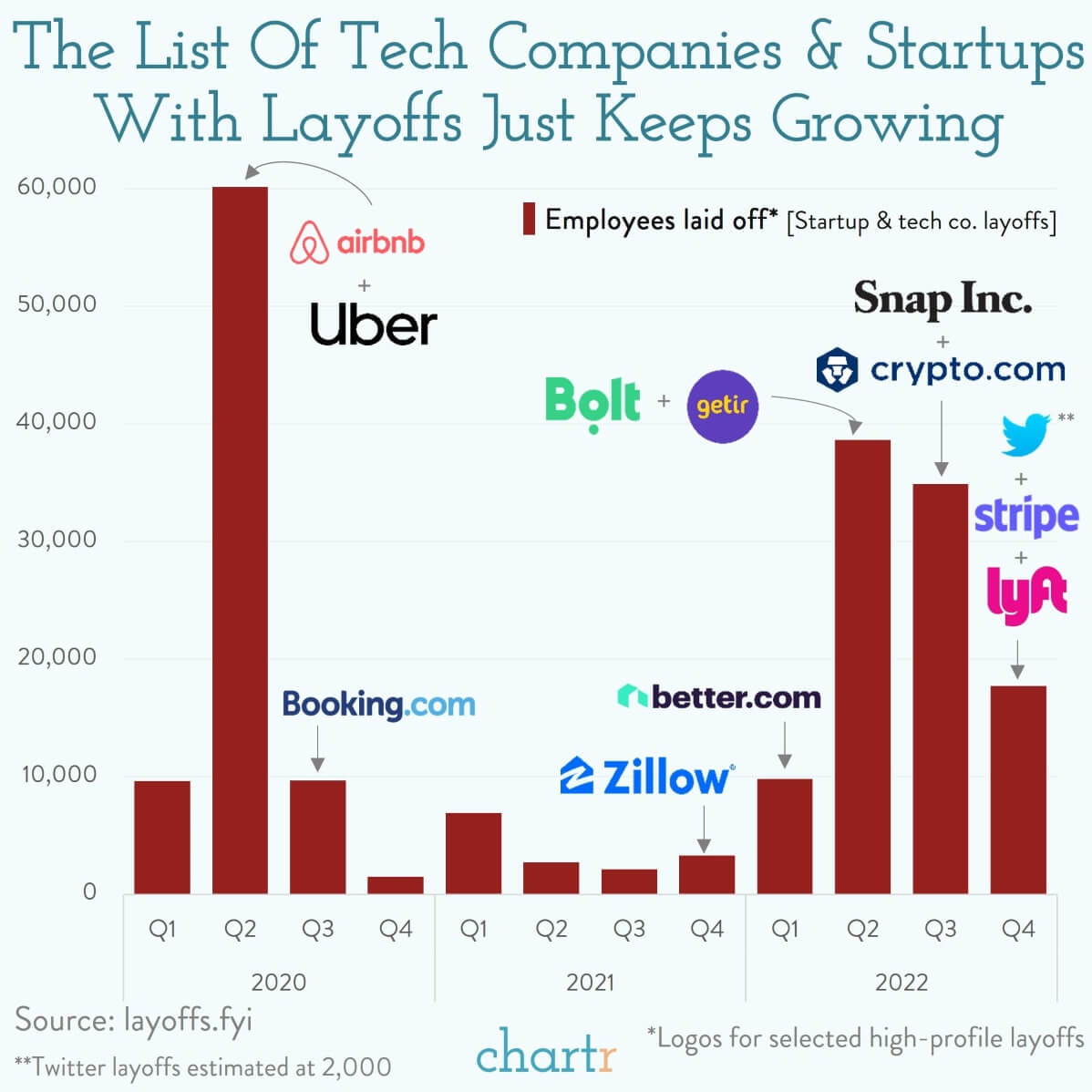

Layoffs, while rising, are still historically low, and competition to fill millions of vacant positions has driven rapid wage gains. However, it is the once high-flying tech sector where a flurry of layoff announcements have swept over the ecosystem.

In the span of a few days, these tech-centric headlines flashed across the news wires:

Amazon pauses hiring for its corporate workforce

Lyft is cutting 13% of its workforce

Dapper Labs, the NFT company behind NBA Top Shot, is laying off 22% of its workforce

Stripe lays off 14% of its workforce

Opendoor slashes 18% of staff

Elon Musk letting go half of Twitter’s employee base today

Even the megacap tech giants Meta, Amazon, Alphabet and Apple have all announced hiring freezes this year. It is crystal clear that corporate leadership is taking proactive measures amidst an uncertain macro backdrop, slowing growth, and the possibility of a recession in 2023.

Source: Bloomberg, Ned Davis Research, Chartr

Goldman Sachs cuts 2023 S&P 500 EPS growth forecast to 0% as weak 3Q margins presage a headwind next year

Following a weak 3Q earnings season in which S&P 500 net margins declined YoY for the first time since the pandemic, Goldman Sachs is lowering their EPS forecasts for 2022 (to $224 from $226), 2023 (to $224 from $234), and 2024 (to $237 from $243). The revised estimates reflect annual growth of +7%, 0%, and +5%, respectively. Their top-down estimates are below bottom-up consensus forecasts for 2023 and 2024. Goldman Sachs maintains their year-end 2022 and 2023 index targets of 3600 (-5%) and 4000 (+6%).

Regarding 3Q22 reporting season, the S&P 500 EPS rose by +3% YoY and posted the smallest aggregate beat since 1Q 2020 driven entirely by Energy. 85% of firms have now reported. On an equal-weighted basis, results appeared relatively resilient: 46% of stocks beat EPS by at least a standard deviation of consensus estimates, compared with the 47% long-term average. However, notable misses from some of the largest stocks weighed on aggregate results. Consensus expected S&P 500 EPS to grow by +3% at the start of earnings season, a low bar that companies largely met. But excluding the +140% EPS growth of Energy, S&P 500 EPS fell by -4%, slightly worse than the -3% decline expected at the start of the season.

Source: David Kostin, Goldman Sachs Portfolio Strategy Research

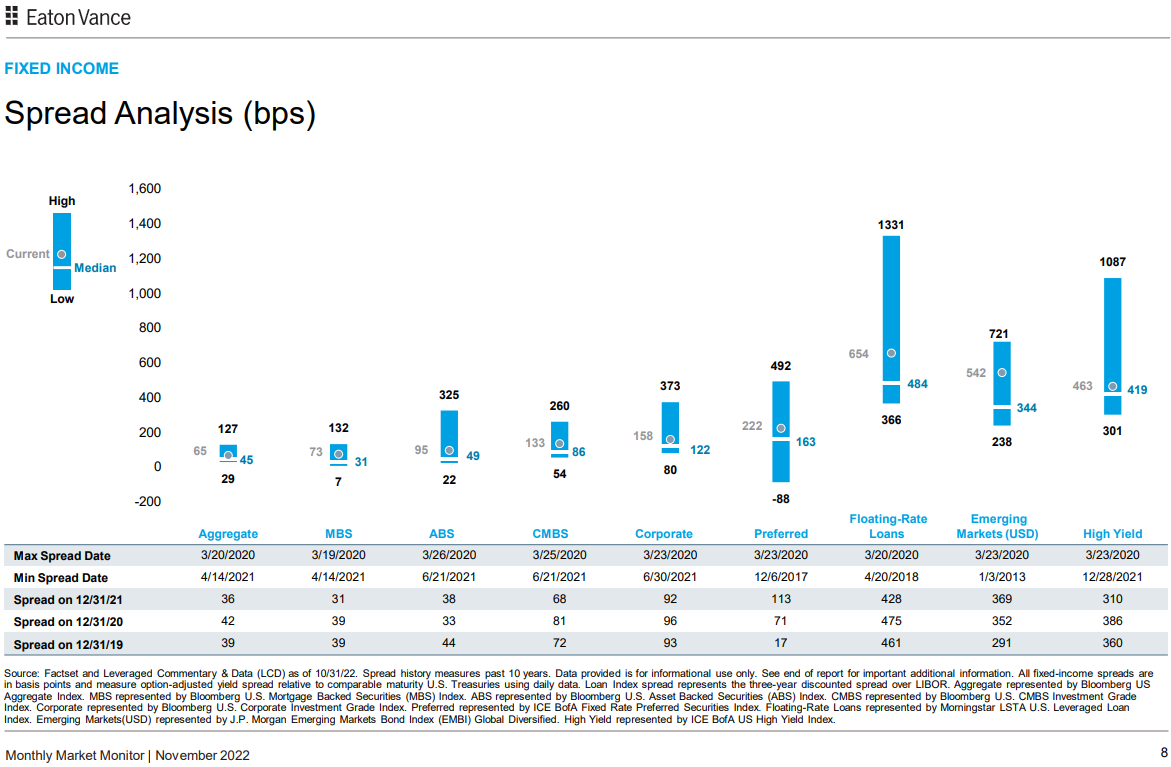

No stress in credit

The bond market is the biggest market of them all and is often known as being the smart money that sniffs out moves ahead of the equity market. Paying attention to fractures in the credit markets is one way to stay ahead in cycles. If there's real stress out there in financial markets, you are going to see it show up in bonds.

Credit spreads are holding in, not blowing out. As you can see in the chart above, spreads are no where near their worst levels when looking at spread history measures over the past 10 years – which does not include 2008, where the upper band would be even higher across each seector.

This is a feather in the cap if you’re a bull.

Source: Eaton Vance

Marty Zweig’s investing rules

Here’s a copy of Marty Zweig’s list of investing rules from a meeting held at the Market Technicians Association in 1990, which is what they called the CMT Association back then.

This is perhaps one of the best lists of rules from one of the best all-time stock investors. #6 is a candidate for most quoted investing principles of all time, however many on this list are worthy candidates.

Source: All Star Charts, Marty Zweig

The week in review

Stocks: Stocks finished lower after Federal Reserve (Fed) Chair Powell’s comments on Wednesday caused traders to sell off domestic equities mid-week. Market participants expected Powell to signal a slower pace of rate hikes beginning in December, however the Chairman stated that it is “very premature” to discuss a pause in rate hikes. Moreover, Powell stated that interest rates may need to rise above the 4.6% that was previously estimated given inflation pressures.

Emerging markets caught a welcomed bid this week. On Friday, the Shanghai Composite finished over 2% higher, and the Hang Seng Index (Hong Kong) rallied nearly 5.5% as Bloomberg reported China is working toward curtailing regulations that penalize airlines for carrying COVID-19 positive passengers. In addition, China’s former chief epidemiologist stated he expects “big and substantive” changes to the country’s zero-COVID-19 policy, though these comments were later retracted.

Bonds: The Bloomberg Aggregate Bond Index finished the week lower as yields increased as traders sold off bonds given Chairman Powell’s comments on Federal Reserve policy this week. High-yield corporate bonds, as tracked by the Bloomberg High Yield index, lost ground for the week, falling in sympathy with their equity counterparts.

Commodities: Oil and natural gas prices finished the week higher. Many commodity analysts have noted that 2022 has seen much volatility for natural gas prices and this week proved to be no exception. The U.S. market for natural gas has shifted from concerns about tight supplies amid the geopolitical landscape now to the potential for lower heating fuel demand given warmer weather forecasts. The major metals – gold and silver – finished higher.

Source: LPL Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.