Personal savings fall, plus banks selloff, work-from-home, top cities for economic output, and long-term returns

The Sandbox Daily (3.9.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

consumer demand supported by falling savings

banks take a drubbing

WFH ripple effects continue to disrupt economy

top 15 cities producing the biggest economic output

long-term returns

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 -1.80% | S&P 500 -1.85% | Russell 2000 -2.81% | Dow -1.66%

FIXED INCOME: Barclays Agg Bond +0.36% | High Yield -0.56% | 2yr UST 4.876% | 10yr UST 3.907%

COMMODITIES: Brent Crude -1.32% to $81.57/barrel. Gold +0.91 % to $1,834.6/oz.

BITCOIN: -7.36% to $20,369

US DOLLAR INDEX: -0.44% to 105.246

CBOE EQUITY PUT/CALL RATIO: 0.73

VIX: +18.32% to 22.61

Quote of the day

“Probability has always carried this double meaning, one looking into the future, the other interpreting the past. One concerned with our opinions, the other concerned with what we actually know.”

- Peter Bernstein, Against the Gods: The Remarkable Story of Risk

Consumer demand supported by falling savings

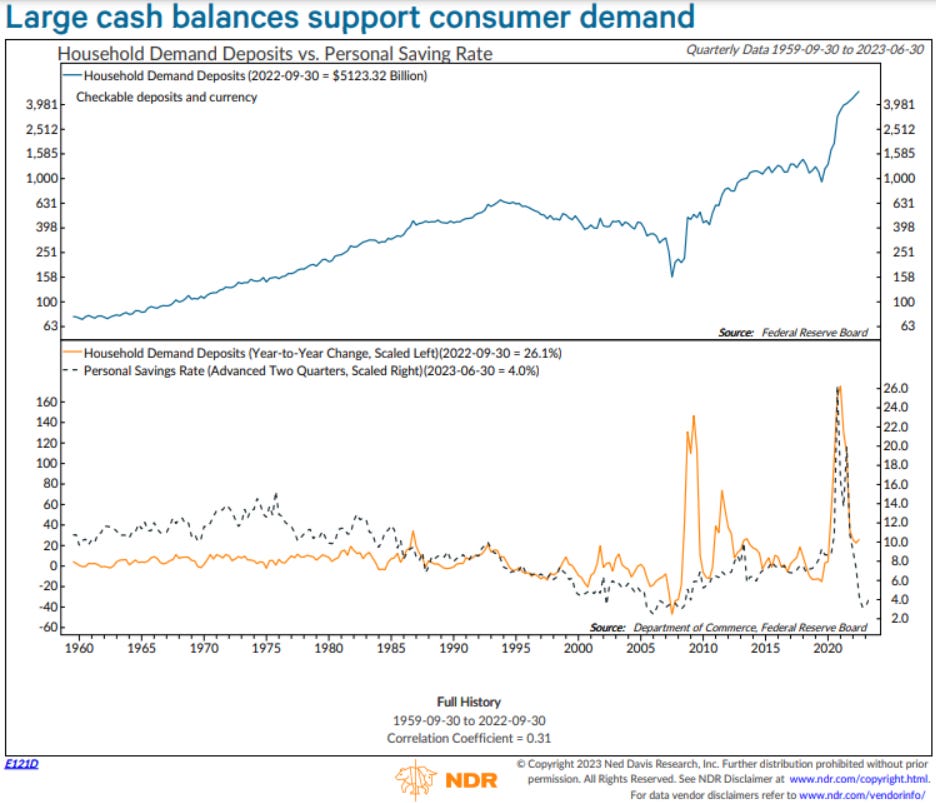

Demand is being supported by consumers tapping into their savings which had swelled during the pandemic. As of 3rd quarter 2022, households had more than $5.1 trillion in bank deposits. The amount had more than quadrupled since the 4th quarter of 2019, largely thanks to the generous fiscal stimulus during the pandemic.

But since the stimulus mostly ended in 2021 and the personal savings rate has plummeted, the rate of growth in demand deposits has slowed considerably – as the chart below shows. Excess savings remain concentrated in the top tiers of the wealth distribution, while those at the bottom have mostly exhausted theirs. Bank deposits for households in the bottom quintile are now at their lowest level since the Global Financial Crisis.

Source: Ned Davis Research

Banks take a drubbing

Pressure in the financial sector has been mounting this week after Silvergate Bank – an FDIC insured crypto-friendly bank – announced it would voluntarily wind down and liquidate its businesses after liquidity ensnared its balance sheet and return deposits to customers.

Today, the banking sector came under heavy selling pressure on the heels of a surprise announcement from Silicon Valley Bank. Silicon Valley Bank said it will need to raise capital to meet short-term liquidity needs. In response, bank stocks tumbled on concerns about interest rate risk and what it could mean for lenders’ balance sheets.

Here is a look at the SPDR S&P Bank ETF (KBE), which just registered its worst single-day performance since 2020, reaching new multi-year lows on both absolute and relative terms:

Not only is the relative trend resolving to the downside as KBE hits its lowest level since 2020 versus the S&P 500, but momentum (as represented by the one-day rate of change in the lower panel) is at its most negative since the depths of the pandemic drawdown in March of 2020.

The Federal Reserve will be closely monitoring the banks, liquidity, and any further fallout ahead of its upcoming policy announcement and interest rate adjustment on March 22nd.

Source: All Star Charts

WFH ripple effects continue to disrupt economy

Three years into the pandemic, business leaders and city officials around the world are still trying just about everything to lure employees back into offices and revive local economies. But in a number of cities across the United States, the effort by companies to shift from work-from-home (WFH) to return-to-office (RTO) has had less than desirable results.

WFH Research, which conducts surveys and research projects on working arrangements and attitudes, recently released findings on its survey to capture the impacts of WFH and RTO. According to WFH Research co-founder Jose Maria Barrero, the distribution of workers suggests that 59.1% are full-time on site, 28.2% of employees are hybrid (working some days in the office and some days remotely), and 12.7% are fully remote. For context, just 5% of paid work hours were remote pre-pandemic.

In-person workdays have declined the most, compared with pre-pandemic levels. For example, workers are spending 37% less time on their work premise versus pre-pandemic in the Washington, D.C. area. White collar industries such as the information technology, finance, and law lead in working-from-home arrangements.

Nowhere is the economic cost of work-from-home more pronounced than the world’s leading financial center: New York. Manhattan workers are spending at least $12.4 billion less a year due to ~30% fewer days in the office, according to a Bloomberg News analysis. That means the average worker is spending $4,661 less per year on meals, shopping, and entertainment near their offices in New York. That compares to $4,051 in Washington D.C., $3,040 in San Francisco, and $2,387 in Chicago. Here are worker attendance patterns by using badge-tracking data from Kastle Systems, where they estimate attendance was 43% of pre-pandemic levels on average during the 4th quarter of 2022:

My interpretation of this structural shift in the labor force and the economic fallout is much is still to come. It’s difficult to project with any high degree of certainty how large metro areas handle lower foot traffic, how businesses rethink opening storefronts and maintaining office space, how entrepreneurs decide to continue to innovate organically, how managers effectively build corporate culture and implement training programs and maintain high levels of employee productivity, how counties redesign budgets based on a shift in income tax collection, and on and on. Much is still to be decided.

Source: Survey of Working Arrangements and Attitudes, Bloomberg, CNBC

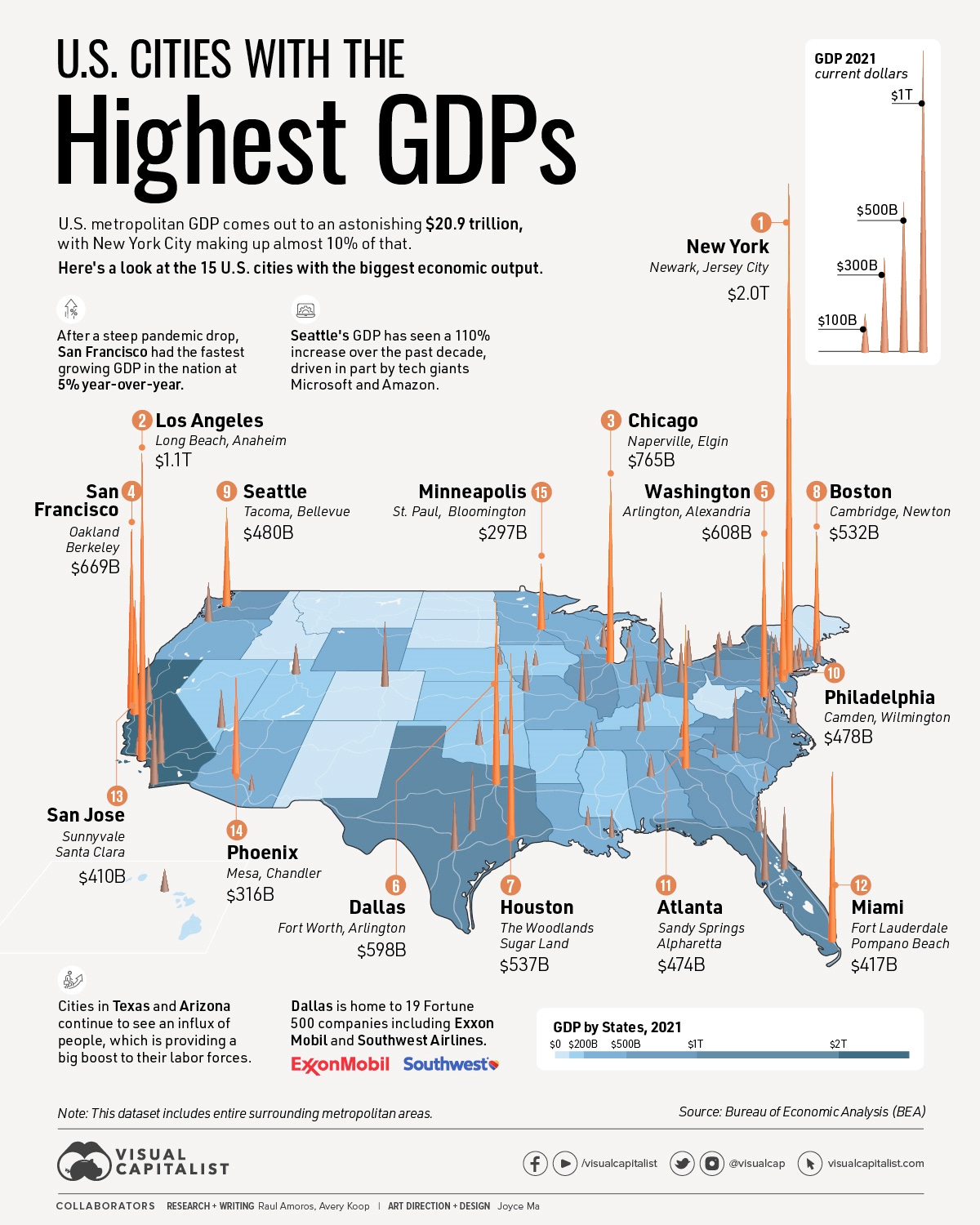

Top 15 cities producing the biggest economic output

The United States has the largest GDP in the world in nominal terms. Using data from the U.S. Bureau of Economic Analysis, this chart ranks the economic output of the top 15 U.S. cities.

The economic center of gravity within the United States could be shifting away from the traditional centers of power towards booming cities in the South and West as populations migrate to these regions, as well as the aforementioned shift away from in-office work arrangements towards flexible work-from-home opportunities.

Source: Visual Capitalist

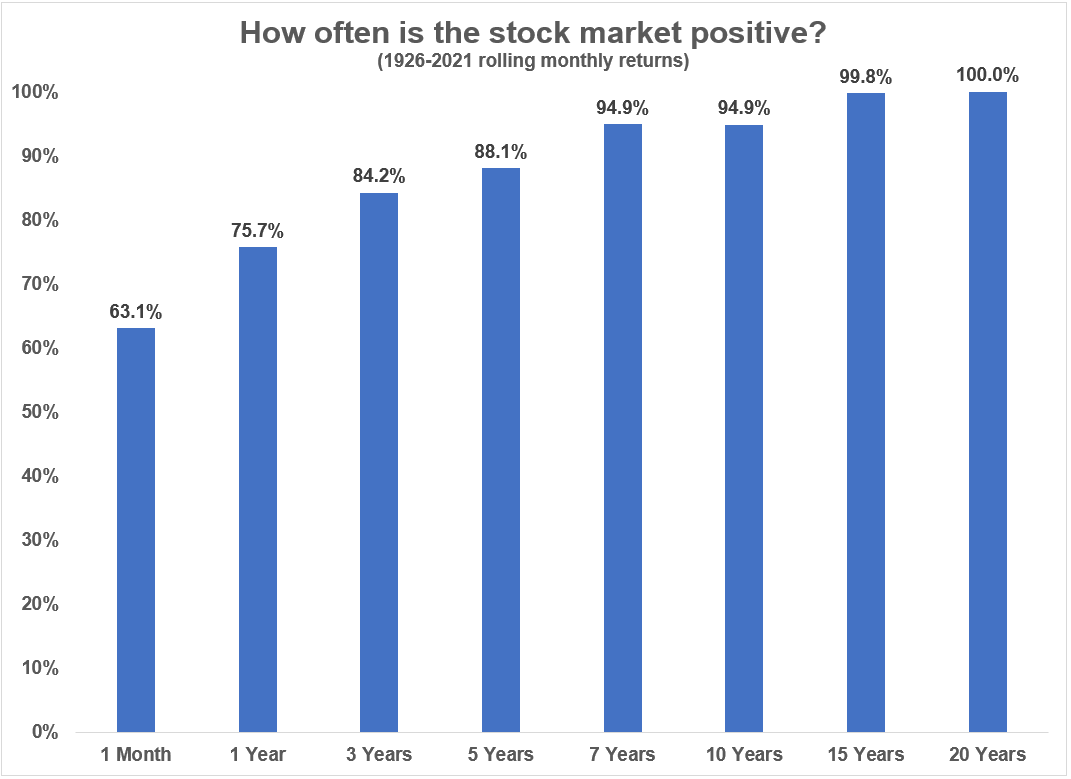

Long term is the best term

Over the long run, the stock market remains the best game in town for beating inflation, compounding your wealth, and meeting your goals.

Of course, investors must consider other important matters like risk tolerance and capacity, taxes, time horizon, liquidity needs, and regulatory requirements.

But still, a long-term time horizon is your biggest ally as an investor, and the stock market handsomely rewards your patience. Rolling monthly returns over a 5-year period from 1926-2021 showed the stock market higher 88.1% of the time, and the results only improve the longer you hold.

Source: A Wealth of Common Sense

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.