Q1 earnings update, plus Baby Boomer wealth transfer, manufacturing, Fed policy, and Apple

The Sandbox Daily (5.15.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

Q1 earnings season update

the Baby Boomer wealth transfer

Empire state manufacturing contracts sharply

Fed policy – what comes next?

Apple worth more than the entire Russell 2000 index

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 +1.19% | Nasdaq 100 +0.55% | S&P 500 +0.30% | Dow +0.14%

FIXED INCOME: Barclays Agg Bond -0.25% | High Yield -0.03% | 2yr UST 4.013% | 10yr UST 3.506%

COMMODITIES: Brent Crude +1.73% to $75.45/barrel. Gold +0.05% to $2,020.9/oz.

BITCOIN: +1.47% to $27,352

US DOLLAR INDEX: -0.24% to 102.439

CBOE EQUITY PUT/CALL RATIO: 0.70

VIX: +0.53% to 17.12

Quote of the day

“Game theory says that the true source of uncertainty lies in the intentions of others.”

- Peter Bernstein, Against the Gods: The Remarkable Story of Risk

Q1 earnings update

As earnings season winds down, the performance of S&P 500 companies continues to be best described as mixed and better-than-feared.

Of the 91% of companies in the S&P 500 that have reported, 77% have reported actual EPS above their estimates, which is in line the 5-year average of 77% and above the 10-year average of 73%. In aggregate, companies are reporting earnings that are +6.7% above estimates, which is below the 5-year average of +8.4%, but above the 10-year average of +6.4%.

In other words, more companies are beating estimates and by larger amounts, at least against their 10-year averages. It must be noted these higher beat rates come against some unimpressive expectations that had been revised downward for several months.

The blended earnings decline (blended combines actual results for companies that have reported and estimated results for companies that have yet to report) for the 1st quarter is -1.7% today – versus consensus estimates for -7% – which would mark the 2nd consecutive quarter in which the index has reported a year-over-year decline in earnings. So, the earnings valley/recession is here, as expected, but shallow thus far.

5 of the 11 sectors are reporting year-over-year earnings growth, led by the Consumer Discretionary and Industrials sectors. On the other hand, 6 sectors are reporting a YoY decline in earnings, led by the Materials and Utilities sectors.

Looking beyond Q1, analysts still predict earnings growth of +1% for calendar year 2023, despite Q1’s decline of -1.7% and Q2’s projected drop of -6.4% – that’s because of a reacceleration in the 2nd half where analysts are projecting earnings growth of +1.5% and +7.1% in the 3rd and 4th quarters.

Key themes have emerged from the results themselves and from the C-Suite on the conference calls: A.I. is the squishy buzzword of 2023, corporate cost-cutting and efficiency actions are paramount, a weaker Dollar strengthens demand abroad, lower interest rates are a tailwind, and deploying cash on stock buybacks satisfies shareholders. Wages remain a lingering key issue against margins.

One major development is fewer companies are citing “inflation” on their earnings calls, with mentions peaking in 2Q22 (like the underlying inflation data itself) and the current count (278) firmly on its way down to pre-pandemic levels – even if it takes another quarter or two to get there.

Source: FactSet, Fundstrat, Lance Roberts, Bloomberg

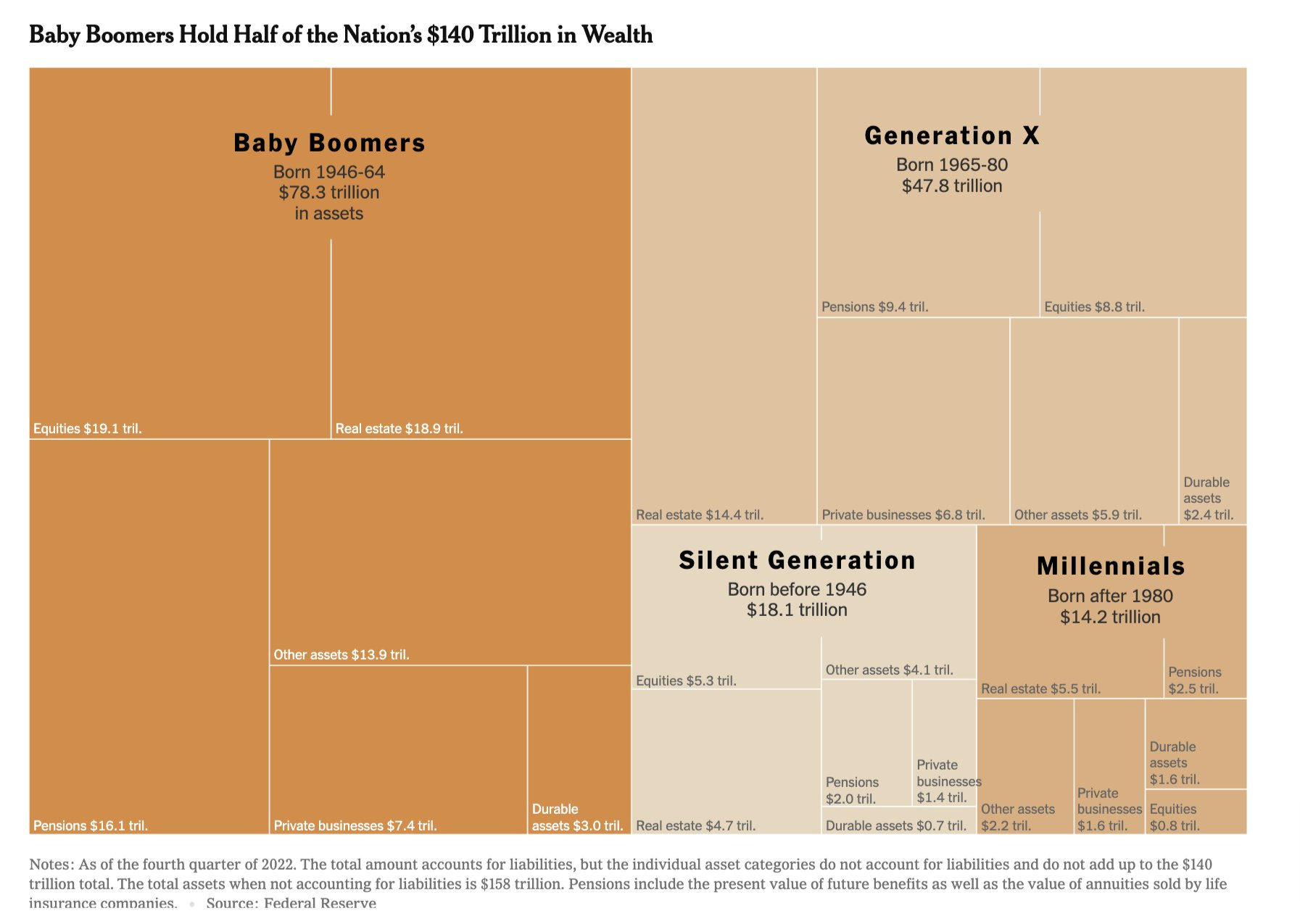

The Baby Boomer wealth transfer

The wealth transfer from Baby Boomers to their children, mostly Gen X-ers and Millennials, is currently in motion and will dwarf any intergenerational transfer of the past.

Baby Boomers hold a disproportionate amount of the country’s wealth, estimated at ~$78.3 trillion in assets. A few key reasons for this massive number were financial discipline, price growth in financial assets, and the housing market.

In 1989, total family wealth in the United States was about $38 trillion, adjusted for inflation. By 2022, that wealth had more than tripled, reaching $140 trillion. Over the coming decades, that money will need a new home, and the implications for our country and the economy are profound: taxes, inflation, household formation, real estate, business transfers, etc.

There are 73 million baby boomers; the eldest are approaching 80 while the youngest are turning 60.

Source: New York Times

Empire state manufacturing contracts sharply

The Federal Reserve Bank of New York released its Empire State Manufacturing Survey for May, which is a survey conducted from a wide swathe of business leaders across the manufacturing sector to summarize general business conditions in New York state – looking for insights into the state and direction of manufacturing.

Manufacturing activity in New York State plunged this month. The Fed’s Empire State Manufacturing Survey index of general business conditions tumbled nearly 43 points from April to -31.8. The decline was almost nine times more than economists had forecasted. A level above zero indicates improving conditions, while a reading below zero indicates worsening conditions.

The survey found just 17% of respondents said business conditions had gotten better in May, while 49% reported they were worse.

After a surge in activity in 2020 and 2021, related to the reopening of the economy, the index fell in contraction territory in January 2022. It has recorded negative readings in 12 of the 17 months since then, averaging -10.3 over the past 12 months. It shows that despite occasional bouts of rebound, factory activity has mostly contracted in the past year.

Source: Federal Reserve Bank of New York, Ned Davis Research

What comes next?

After the historic volatility and policy tightening of the past 12-18 months or so, monetary policy is now entering a period of the unknown.

Fed Chair Jerome Powell’s May 3rd press conference, and the subsequent incoming data, have strengthened the market’s conviction that the FOMC will pause its rate hiking cycle at the June 13-14 meeting. Markets are appropriately priced for this near-term view, but not for what is likely to happen thereafter.

And this is where the Fed’s jobs get much harder. We knew interest rate hikes were coming when the economy was printing a 9% handle on consumer price growth – that was the easy part. But what does the FOMC committee do now and going forward in the face of tighter credit conditions, a manufacturing malaise, a resilient labor market and poor market sentiment; how does the Fed engineer the soft landing – that’s the much harder part.

If the economy continues to grow, the unemployment rate remains below 4%, and underlying inflation comes down only slowly, Fed officials are likely to keep rates unchanged at what they view as a restrictive level well into 2024. The risks to this baseline forecast are clearly on the downside, as the Fed Funds Rate is much more likely to go from the current 5% to 3% than to 7%. But even on a probability-weighted basis, markets are likely pricing too much easing in late 2023 and 2024.

Source: Goldman Sachs Global Investment Research

Apple worth more than the entire Russell 2000 index

The market capitalization of Apple Inc. (AAPL) has surpassed that of the entire Russell 2000 index.

Apple’s market capitalization, which measures how much the company is worth based on the value of all its outstanding stock, surpassed that of the Russell 2000 index and has held a higher value for the last two weeks. Apple is worth roughly $2.7 trillion, which is roughly $100 billion more than the combined value of all 2,000 stocks in the Russell 2000.

Apple (AAPL) is up +32.8% in 2023, while the small-cap index (R2000) is down -0.9%.

Source: Bespoke Investment Group

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.