Rate cuts on the horizon (??!?), plus Fed's dovish posturing this week, unprofitable firms, and wholesale inflation

The Sandbox Daily (10.11.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

history suggests peak rates during Fed tightening cycles are rather brief

Fed committee members' dovish posturing

the risk from unprofitable firms

wholesale inflation (PPI) accelerates more than expected in September

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +0.72% | S&P 500 +0.43% | Dow +0.19% | Russell 2000 -0.15%

FIXED INCOME: Barclays Agg Bond +0.46% | High Yield -0.01% | 2yr UST 4.986% | 10yr UST 4.562%

COMMODITIES: Brent Crude -1.73% to $86.13/barrel. Gold +0.64% to $1,872.9/oz.

BITCOIN: -2.43% to $26,704

US DOLLAR INDEX: -0.09% to 105.729

CBOE EQUITY PUT/CALL RATIO: 0.63

VIX: -5.52% to 16.09

Quote of the day

“The whole problem with the world is that fools and fanatics are always so certain of themselves, and wiser people so full of doubts.”

- Bertrand Russell, British mathematician and philosopher

History shows peak rates during Fed tightening cycles are rather brief

Looking at the past eight Fed tightening cycles, bond yields were down each time by an average of 100 bps following the final rate hike, irrespective of whether the recession or the soft landing followed.

Reviewing these past cycles shows the Fed cuts rates rather quickly following that final hike, down over 50 bps after 3 months and 100 bps after 8 months – meaning, the peak for interest rates in the cycle is rather fleeting.

Of course, each cycle is unique and presents its own opportunities and risks so calibrating the appropriate level of interest rates to balance each is difficult.

While the U.S. fiscal deficit is significant coupled with a deteriorating supply-demand picture for government bonds (as noted in yesterday’s note), yields at present are trading much above the inflation forwards and above the levels of economic activity, with growth at risk of softening post the strong Q3 prints.

Source: J.P. Morgan

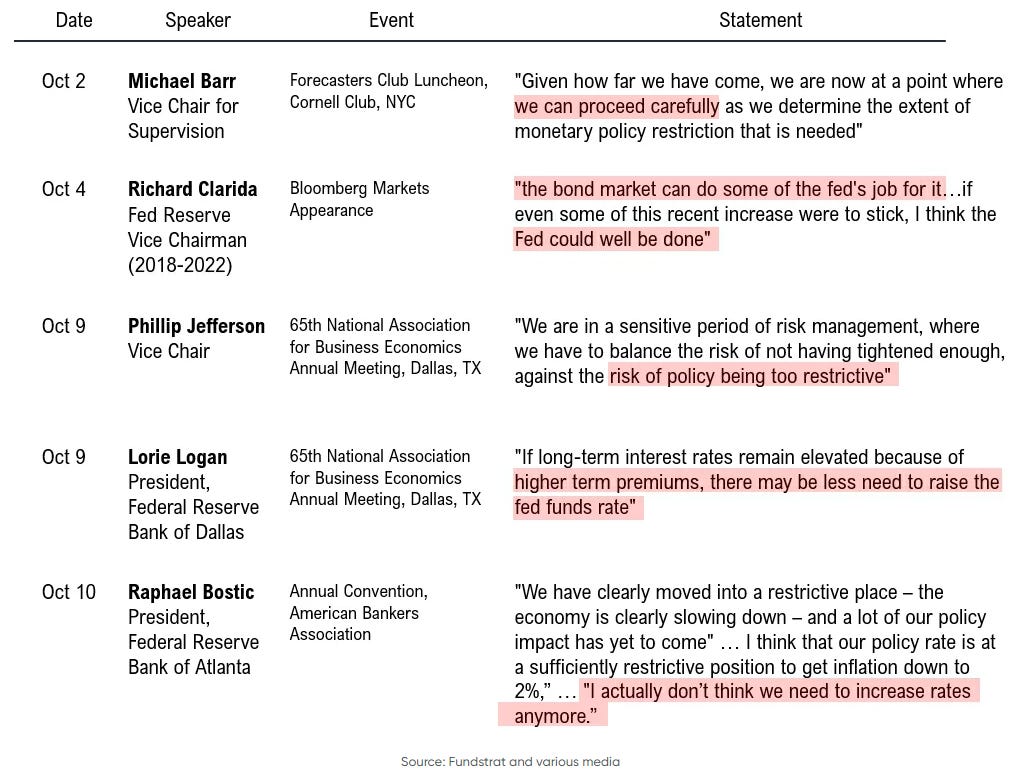

Fed committee members' dovish posturing

Fed speak over the last week or so has been quite dovish (i.e. favorable) for markets.

To wit:

These comments from various Fed committee members have effectively reversed much of Federal Reserve Chairman Jerome Powell’s hawkish comments in the presser following the FOMC policy announcement and updated Summary of Economic Projections (SEP) statement on September 20th.

On the day of the FOMC meeting (9/20), the U.S. 10-year Treasury surged higher from 4.31% to the peak of 4.89% – an explosive march higher in rates. Since then, yields have retraced roughly 50% of that move down to ~4.6%.

This has been incrementally supportive for equities over the last few trading sessions and likely extends the Fed rate pause given the push higher in bond yields.

Source: FS Insight

The risk from unprofitable firms

Almost half of publicly listed U.S. corporations have negative profit margins, with the number of unprofitable firms having risen each decade since the 1960s.

They have been able to survive in artificially low interest rates and ample liquidity environment. Things have changed though.

Fortunately, in respect to market risk contagion, their share of overall revenues remains economically insignificant at just 10%.

Source: Goldman Sachs Global Investment Research

Wholesale prices (PPI) for September rise more than expected

The Labor Department released its latest Producer Price Index (PPI) report for September, tracking inflation from the standpoint of manufacturers and wholesalers.

Headline PPI rose +0.5% from the prior month, a slowdown from August’s +0.7 increase but still above economists’ expectations for +0.3% growth. On a year-over-year basis, PPI climbed higher for the 3rd consecutive month to +2.2%, the highest level since April. Meanwhile, Core PPI (ex-food and energy) rose +0.3% MoM and +2.7% YoY.

Both headline and core price pressures have come down substantially from peak levels earlier in this cycle, while the pickup in recent months reflect rising costs which may lead to higher inflation pressures at the consumer level.

The cycle peak was +11.7% back in March 2022, with the index down 15 consecutive months before modestly turning higher the last 3 months. Looking back at a longer time frame of the data series, the current readings are below historical measures.

The PPI report differs from the CPI report in that it measures prices that producers pay for the goods and services they need.

Source: Bureau of Labor Statistics, Ned Davis Research, Bloomberg

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.