Recent wealth gains, plus QT and mortgages, Bitcoin, and 10-yr US Treasury

The Sandbox Daily (1.10.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

wealth gains should support consumer spending

potential QT wind-down should improve mortgage market outlook

spot Bitcoin set for trading

10-yr U.S. Treasury yield back above 4%

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +0.69% | S&P 500 +0.57% | Dow +0.45% | Russell 2000 +0.11%

FIXED INCOME: Barclays Agg Bond -0.19% | High Yield +0.18% | 2yr UST 4.364% | 10yr UST 4.032%

COMMODITIES: Brent Crude -1.07% to $76.76/barrel. Gold -0.18% to $2,029.4/oz.

BITCOIN: +0.49% to $45,834

US DOLLAR INDEX: -0.20% to 102.361

CBOE EQUITY PUT/CALL RATIO: 0.61

VIX: -0.55% to 12.69

Quote of the day

“Everyone has the brainpower to make money in stocks. Not everyone has the stomach.”

- Peter Lynch, Former PM of the Fidelity Magellan Fund

Wealth effects should support consumer spending

Total household wealth contracted sharply in 2022, following sell-offs in the equity market and declines in real estate prices. See below; left chart.

However, over the last year or so, stock and home prices have recovered from their declines, strengthening household balance sheets. This has left total household net worth as a share of disposable income at 740%, the highest level in history aside from 2022. See below; right chart.

The increases have been broad-based across the income distribution.

In particular, households in the lower half of the income distribution, who typically have about twice as much of their wealth in real estate as in equities, have benefited from the steady rise in home prices over the past few years and experienced a meaningful increase in their net worth-to-income ratio since 2019.

Source: Goldman Sachs Global Investment Research

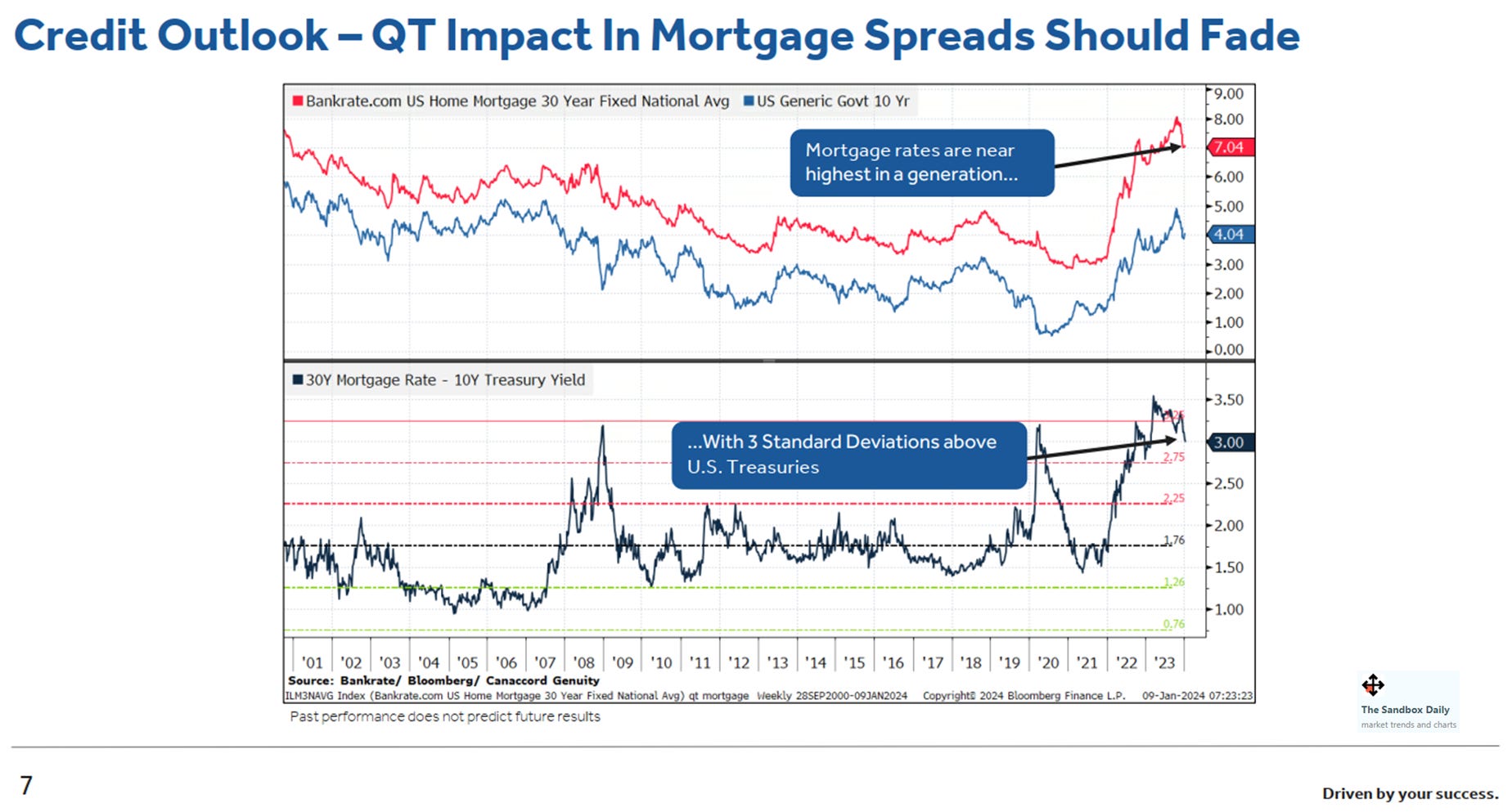

Disconnect between 10-yr Treasury and mortgage rates

What is the impact of Quantitative Tightening (QT)?

In respect to mortgages, the Fed switched gears starting June 2022 when the central bank transitioned from a net buyer of mortgage-backed securities (MBS) to net seller.

The Fed had been the largest buyer of U.S. mortgages (orange color in chart below) and the institution was buying these bonds hand over fist until early 2022 – effectively buying mortgages and doing Quantitative Easing (EQ) into the peak of a historically tight and booming housing market.

Now, with the invisible hand removed from the market, the net impact is a significant decoupling in mortgage rates.

Normally, 30-year fixed rate mortgages track the 10-year U.S. Treasury bond closely, adding a spread of roughly 150-200 basis points on top of the risk-free rate.

Today, mortgages are hovering around 7% having come down from a recent generational high of 8%, yet mortgages are still 3.0 standard deviations above/expensive to U.S. Treasuries.

The whole mortgage market became the Federal Reserve, but for nearly two years, the Fed had left the dinner table. This helped create a major dislocation in the mortgage market.

The good news?

A potential upshot here came last weekend when Lorie Logan, president of the Federal Reserve Bank of Dallas, made comments during a speech suggesting the Fed should consider slowing down its quantitative tightening (QT) policy in the coming months.

This is important because a softer Fed reduces pressure on mortgage rates in absolute terms as well as the relative spread against Treasuries as buyers re-emerge on the demand side, while also improving liquidity conditions to fuel better conditions for credit creation.

Source: Dwyer Strategy, Reuters

Spot Bitcoin set for trading

The Bitcoin spot ETF has finally been approved by the Securities and Exchange Commission (SEC).

This is a historic day for the burgeoning asset class very much in the nascent stage of its evolution.

The approval is a landmark event in the adoption of cryptocurrency by mainstream finance, as the ETF structure gives institutions, financial advisors, and individual investors a familiar and regulated way to buy exposure to bitcoin.

The SEC document approved 11 spot Bitcoin ETFs – with trading set to begin tomorrow.

Source: SEC, Eric Balchunas, The Block, Bloomberg

10-yr U.S. Treasury yield back above 4%

The 10-year U.S. Treasury yield peaked October 23rd at 5.0% after marching higher for 6 straight months in 2023.

Since then?

Yields collapsed for two straight months reaching a low of 3.7% in late December. In the face of this material breakdown in yields and the U.S. dollar, stocks went on to experience a historic breadth and momentum surge that helped improve everyone’s year-end account statement and P&L.

Recently, however, yields have reversed the declining channel, backing and filling around the 200-day moving average (DMA) and facing a key overhead support-turned-resistance line around 4.05%. Meanwhile, relative strength (RSI) has stalled around the midline.

The next move in yields will be informative for risk assets.

A breakdown in yields at these levels should support the next leg higher in risk assets, while a sustained move higher would result in the continued chop we’ve experienced thus far in 2024.

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.