Recession indicator reaches a record, plus year-end headwinds, moats, earnings revisions, and the week in review

The Sandbox Daily (9.15.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

that pesky recession indicator

year-end headwinds

different kinds of moats

earnings revision trend

a brief recap to snapshot the week in markets

Let’s dig in.

Markets in review

EQUITIES: Dow -0.83% | Russell 2000 -1.05% | S&P 500 -1.22% | Nasdaq 100 -1.75%

FIXED INCOME: Barclays Agg Bond -0.23% | High Yield -0.37% | 2yr UST 5.036% | 10yr UST 4.336%

COMMODITIES: Brent Crude +0.55% to $94.22/barrel. Gold +0.63% to $1,945.0/oz.

BITCOIN: -0.63% to $26,436

US DOLLAR INDEX: -0.08% to 105.323

CBOE EQUITY PUT/CALL RATIO: 0.85

VIX: +7.57% to 13.79

Quote of the day

“The ultimate measure of a man is not where he stands in moments of comfort and convenience, but where he stands at times of challenge and controversy.”

- Martin Luther King, Jr.

That pesky recession indicator

Historically, inverted yield curves have been associated with recessions like peanut butter goes with jelly.

The chart below shows historical streaks of the 3-month/10-year U.S. Treasury spread inversion - meaning: higher rates on the short end, lower rates at the long end.

This part of the curve has been inverted for a record 213 straight days (a/o Friday, 9/15) and still going strong.

Eventually, this classic indicator may get it right. Or maybe it won’t. Use history as a guide, not gospel.

Source: Bloomberg, Bespoke Investment Group

Year-end headwinds

Goldman Sachs expects three developments to temporarily slow growth in the 4th quarter:

Resumption of student loan payments (-0.5% drag)

Federal government temporary shut down (-0.2% drag per week)

Reduced auto production and manufacturing from the UAW strike (-0.05% to -0.10% per week)

Taken together, the expectation is GDP growth slows from +3.1% in Q3 to +1.3% in Q4 (vs. consensus of +2.9% and +0.6%), yet the slowdown should be sallow and short-lived as the economy reaccelerates in 1Q24.

Source: Goldman Sachs Global Investment Research

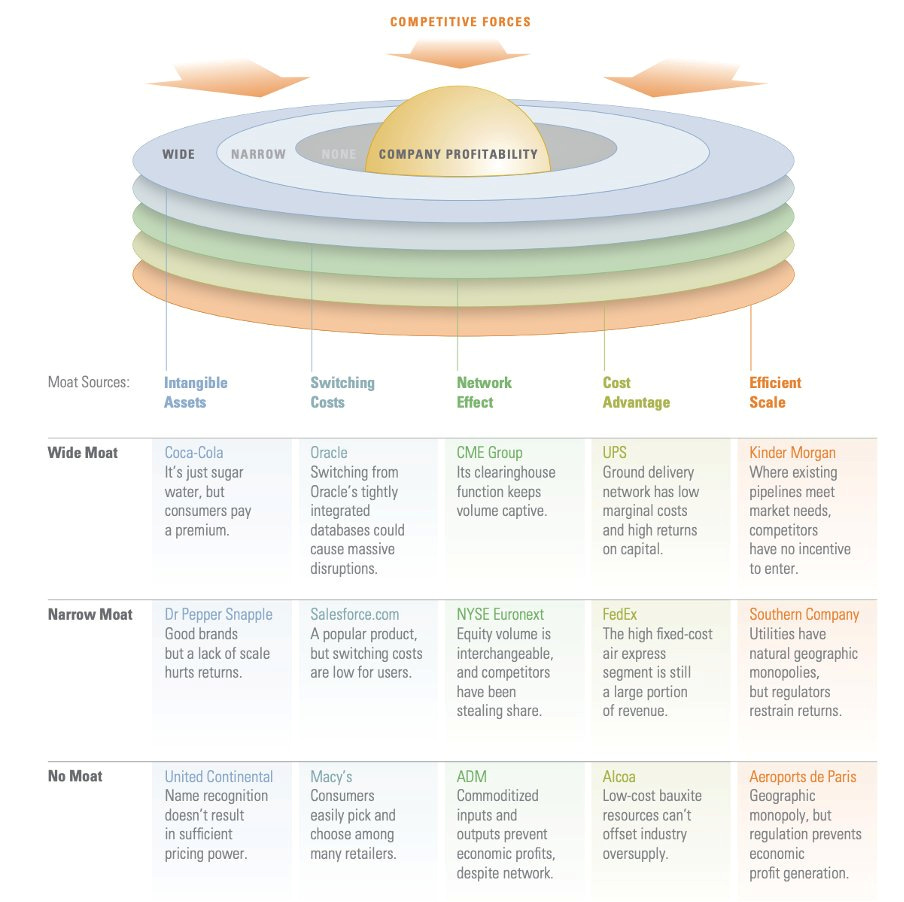

Different kinds of moats

In investing, it all starts with the economic moats. Determining the existence and durability of a competitive advantage is key to become a great investor.

A moat, or a company’s durable competitive advantage, is a condition that puts a company in a superior business position. This will allow the business to maintain and/or increase its profit margin and market share.

Here is a great framework from Morningstar:

Warren Buffett once said the company itself can be seen as the equivalent of a castle, while the value of the castle will be determined by the strength of its moat. Meaning, the moat protects those inside the castle and prevents outsiders from entering the fortress.

Source: Morningstar

Earnings revision trend is… trending higher

Earnings revisions, which can be a momentum factor, have not collapsed as expected. In fact, it’s quite the opposite – forward profit expectations have been steadily rising.

Economically sensitive areas look to be the most at-risk for earnings cuts, while growthier and more secular companies are improving.

In the chart below, five sectors are expected to report higher earnings today compared to June 30 (i.e. 3-month revisions) due to upward revisions to EPS estimates. The Consumer Discretionary sector has seen the largest increase in EPS estimates.

Source: Hi Mount Research, Goldman Sachs Global Investment Research, FactSet

The week in review

Talk of the tape: Risk assets continue to hang in there despite the continued upward pressure on rates and the strengthening U.S. dollar. Some focus on pickup in China recovery expectations and fresh stimulus measures. Peak policy another area of focus ahead of the Fed’s policy rate meeting next week. Big options expiration on Friday received a lot of attention in the press. UAW implemented targeted strikes at all three big US automakers in a move widely expected given big gap in negotiations.

Soft-landing expectations are the key driver of the bullish narrative. The 2H23/2024 earnings rebound, earnings revisions trend, and record amount of money market assets on the sidelines flagged as some of the bullish drivers. Disinflation traction cited as another tailwind. Consumer resilience, although showing some signs of fatigue, continues to be a higher-profile bright spot.

The backup in interest rates, liquidity headwinds, and the lagged effects of policy tightening (18 months now) are talking points among the bearish narrative. The higher-for-longer Fed another overhang as markets decide what to make of Fed Funds Rate expectations for 2024. Seasonal headwinds shouldn’t be dismissed. Geopolitical scrutiny continues to lurk in the shadows.

Stocks: The major markets ended mixed this week, with Apple’s challenges in China causing the information technology sector to be this week’s laggard. The S&P 500 remains in a sideways range of 4300-4600. According to the AAII Sentiment Survey, the percentage of bullish investors declined from 42.2% to 34.4% this week, tracking below the historical long-term average of 37.5%. Meanwhile, looking down the cap stack, small-caps have continued to struggle, on both an absolute and relative basis.

Bonds: The Bloomberg Aggregate Bond Index ended the week marginally lower. While consensus expectations continue to move towards a soft landing, the corporate credit markets are seemingly only pricing in a soft landing. Across the pond, the European Central Bank decided to raise interest rates by an additional 25 basis points, bringing the total to 4.50%.

Commodities: Energy prices ended the week positive as the major metals lost ground. The recent rally in energy has largely been underpinned by tightening supply expectations following Saudi Arabia and Russia’s decision to extend their production cuts until December; meanwhile, on the demand side of the equation, world oil demand is ‘scaling at record highs,’ according to the International Energy Agency.

Source: Dwyer Strategy, LPL Research

That’s all for today. Have a great weekend!

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, business, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.