Recession odds fall below 50%, plus Growth/Value ratio, mortgage rates hit 8%, bond returns vs interest rates, and the U.S. saving rate

The Sandbox Daily (10.18.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

recession no longer consensus view per WSJ

Growth continues breakout against Value

mortgage rates hit 8.00%

the impact of a 1% rise or fall in interest rates

U.S. saving rate has fallen below pre-pandemic level

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 -2.11% | Nasdaq 100 -1.41% | S&P 500 -1.34% | Dow -0.98%

FIXED INCOME: Barclays Agg Bond -0.47% | High Yield -0.48% | 2yr UST 5.221% | 10yr UST 4.913%

COMMODITIES: Brent Crude +1.56% to $91.29/barrel. Gold +1.35% to $1,948.6/oz.

BITCOIN: -0.67% to $28,309

US DOLLAR INDEX: +0.30% to 106.569

CBOE EQUITY PUT/CALL RATIO: 0.80

VIX: +7.49% to 19.22

Quote of the day

“All of investing consists of dealing with the future, and the future is something we can't know much about. But the limits on our foreknowledge needn't doom us to failure as long as we acknowledge them and act accordingly.”

- Howard Marks, Oaktree Capital in You Can't Predict. You Can Prepare.

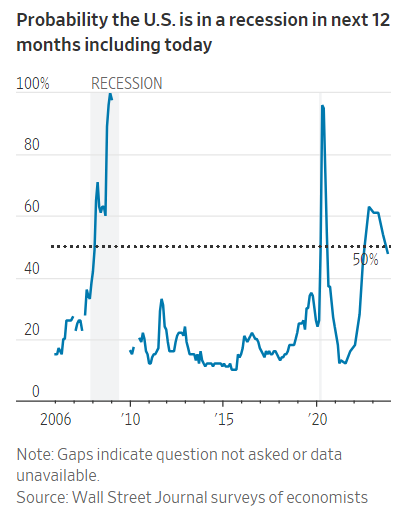

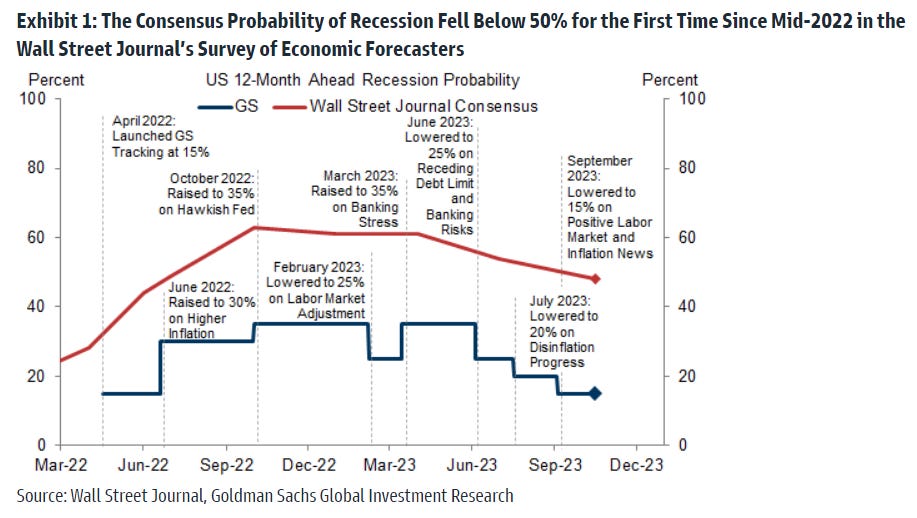

Recession no longer consensus view per WSJ

The consensus probability of recession over the next 12 months declined from 54% in July to 48% in the October Wall Street Journal survey of economic forecasters, the 1st time it has been below 50% since mid-2022.

Goldman Sachs continues to be one of the lowest on the street at 15%, roughly the historical unconditional average.

Source: Wall Street Journal, Goldman Sachs Global Investment Research

Growth continues breakout against Value

The Russell 1000 Growth Index (i.e. Large Cap Growth) has outpaced the Russell 1000 Value Index (Large Cap Value) by 27.8% points so far in 2023.

If the year ended today, it would be the 3rd best year – after 2020 and 1999 – for Growth versus Value since Russell data began in 1979.

The Growth-to-Value ratio is still trading below the COVID pandemic highs but has reversed course in 2023. More recently, the Russell 1000 Growth/Value ratio broke out of a 4-month trading range to its highest level since January 2022.

The breakout has not been confirmed by Small-Cap Growth/Value or breadth expansion within each style box.

Source: Ned Davis Research

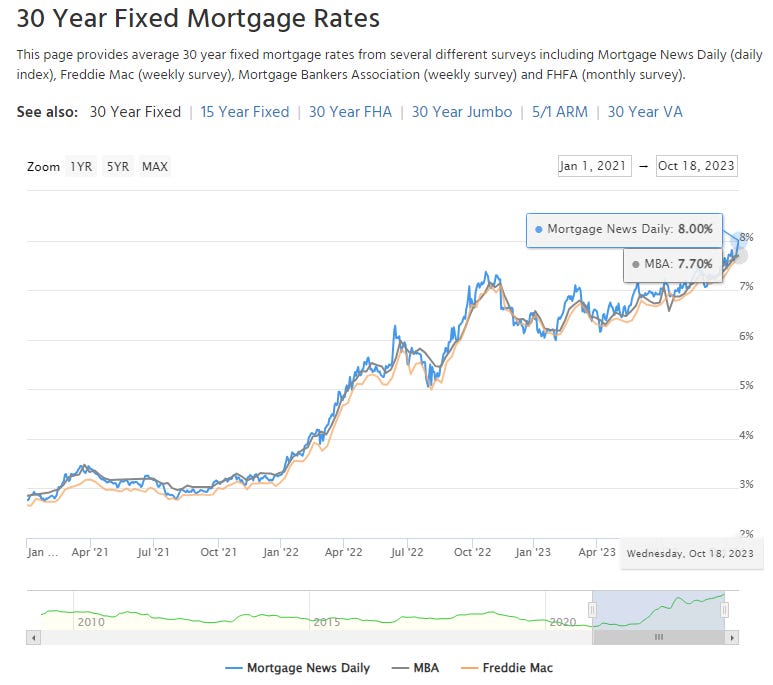

Mortgage rates hit 8.00%

According to Mortgage News Daily, the average 30-year fixed mortgage rate hit 8.00% this morning, the highest level since mid-2000.

Quotes were as low as 2.75% in January 2021.

The climb in mortgage rates is more bad news for prospective home buyers, who have been contending with low inventory, relatively stable prices, and higher financing costs. We have already seen higher rates hurt demand for new loans.

Joel Kan, MBA’s deputy chief economist, had this to say: “Homebuying activity continues to pull back given reduced purchasing power from higher rates and the ongoing lack of available inventory.”

Source: Mortgage News Daily

The impact of a 1% rise or fall in interest rates

When interest rates rise by 1%, bond prices tend to fall. The inverse is also correct; when interest rates fall by 1%, bond prices rise.

This inverse relationship between interest rates and bond prices is known as interest rate risk.

But these relationships are not exactly 1-to-1 – things like duration, convexity, and other factors must be considered, but that is for another discussion.

In the graphic below, J.P. Morgan captures this relationship between bond prices and interest rates in rather simple mathematical terms, showing the asymmetric movement in bond returns at these higher interest rate levels.

Assuming a parallel 1% move in interest rates higher and lower from current rates, here is how different sectors across fixed income would perform.

For example: a 1% rise in rates would cause Investment Grade Corporate bonds to fall -0.8%, while a 1% decline in rates would create a positive return of +12.8%.

Source: J.P. Morgan Guide to the Markets

U.S. saving rate has fallen below pre-pandemic level

The U.S. saving rate has dropped below its pre-pandemic average, while saving rates among other major high-income economies have remained above their pre-pandemic averages.

Household saving, which measures the difference between disposable income (money in) and consumer spending (money out), spiked during 2020-2021 as consumers cut back on spending and government policies provided various fiscal stimulus measures.

We knew saving rates would come down from there, but it’s only the United States where the present rate has fallen below the 2015-2019 rate (grey bar below blue bar).

The next chart tracks how excess savings have changed by year among the United States and other major high-income economies since the pandemic.

After excess savings (as a percentage of disposable income) peaked in the 3rd/4th quarters of 2021 at 14.37%, this number has fallen under 10% over the last two years.

Source: Liberty Street Economics

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Interesting JP Morgan graphic today. Thanks much.