Revisiting Technical Analysis with "The Mooch," plus cheap fixed-rate debt, China, and Retail Sales

The Sandbox Daily (8.15.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

revisiting Technical Analysis with Anthony Scaramucci

cheap fixed-rate debt puts borrowers in better financial position

China unexpectedly cuts rates to support faltering economy

hot Retail Sales report shows resilient consumer

Let’s dig in.

Markets in review

EQUITIES: Dow -1.02% | Nasdaq 100 -1.10% | S&P 500 -1.16% | Russell 2000 -1.29%

FIXED INCOME: Barclays Agg Bond -0.27% | High Yield -0.32% | 2yr UST 4.959% | 10yr UST 4.219%

COMMODITIES: Brent Crude -1.36% to $85.04/barrel. Gold -0.55% to $1,933.3/oz.

BITCOIN: -0.65% to $29,170

US DOLLAR INDEX: +0.01% to 103.201

CBOE EQUITY PUT/CALL RATIO: 0.70

VIX: +11.07% to 16.46

Quote of the day

“Much (perhaps most) of the risk in investing comes not from the companies, institutions, or securities involved. It comes from the behavior of investors.”

- Howard Marks, Oaktree Capital Management in Ditto

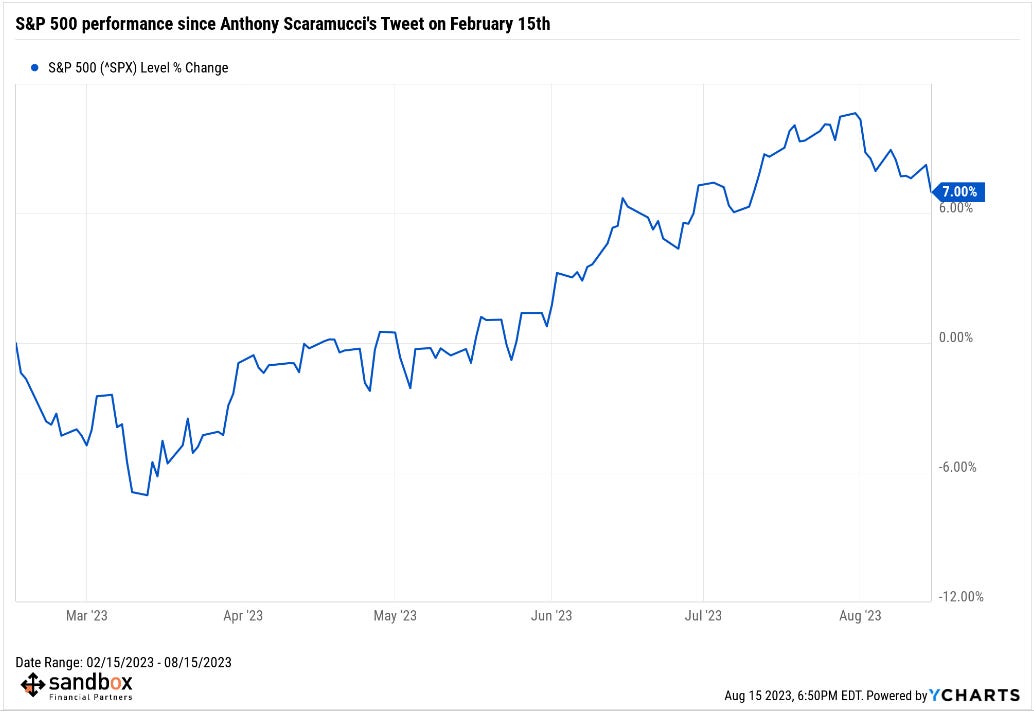

Revisiting Technical Analysis with “The Mooch”

Too often in market research, we read about what to expect from the market going forward given an analysis of various historical examples – but we never follow up on whether those results actually materialized.

Today I was reminded of this because of some great data that closet market technician Anthony Scaramuccio – aka “The Mooch” – put on Twitter 6 months ago today.

That day, the S&P 500 closed at 4,147.60 and above its 200-day moving average for the 18th session in a row.

The former White House Communications Director made the point that “the low” was in because the S&P 500 closed above its 200-day moving average for 18 consecutive sessions.

This tweet sparked quite a bit of interest across FinTwit, so SentimenTrader got to work crunching the data on this claim. Of the 11 prior instances since 1950, the S&P 500 had never been lower 3, 6, or 12 months later. In fact, the median return was quite encouraging across all three time horizons.

Here we are 6 months later and it sure feels like the bear market low is in. In terms of market performance, the S&P 500 is up +7% – not quite the median return of 11.1% but still a strong result.

Strength begets strength.

We’ll check back in February 2024 to close the loop.

Source: Anthony Scaramucci, SentimenTrader

Cheap fixed-rate debt puts borrowers in better financial position

Here is Michael Cembalest, Chairman of Market and Investment Strategy for J.P. Morgan Asset & Wealth Management, providing one reason (of many) for the resilience of the global economy and stock market:

Rising interest rates will take time to flow through to profit margins and household balance sheets. In contrast to some U.S. banks that made extremely poor decisions to extend asset duration at the lows in rates, many U.S. and European companies extended liability duration and enjoy the lowest levels of interest expense to cash flow in decades.

As shown below, for the first time on record, corporate interest expense is falling as the Fed is hiking rates.

U.S. household debt service costs are also low. One reason: the average coupon on outstanding residential mortgages is ~3.5%, immunizing many homeowners from the spike in mortgage rates to ~7%. Credit card and auto delinquencies are rising, but from low levels and are now back at 2010-2020 averages.

That means the vast majority of corporate America and American households with existing fixed rate mortgages, auto loans, or student loans have not been exposed by the Federal Reserve’s 11 interest rate hikes since March 2022.

Source: Michael Cembalest, Wall Street Journal

China unexpectedly cuts rates to support faltering economy

China's economic activity data over recent months – consumer spending, industrial output, real estate, exports, and unemployment come to mind – all tell the same story of an economy slowing down, prompting some economists to flag risks that China will struggle to meet its stated growth target of 5% for the year without more stimulative measures.

In response, China’s central bank unexpectedly announced a flurry of interest rate cuts for the 2nd time in 3 months to shore up its sputtering economic recovery after abruptly abandoning their zero-COVID policy in December of last year.

Given China's debt-fueled investment in infrastructure and property has peaked, and as exports are slowing, China seems to be aiming to stimulate the only source of demand left remaining to maneuver: household consumption. By cutting interest rates again, Chinese authorities are attempting to stimulate demand for new loans from households and businesses.

U.S. Treasury Secretary Janet Yellen said China’s slowdown is a “risk factor” for the American economy.

Source: Bloomberg

Retail Sales shows resilient consumer

Retail sales – an economic metric that tracks consumer demand for goods – jumped well above expectations, climbing +0.7% in July vs. +0.4% estimated.

June marked the 4th straight monthly gain in sales, the longest winning streak since April 2022 and indicating that consumer spending power remains intact despite a choppy 1st quarter.

Today’s report shows that consumer demand for goods is still solid, despite more than a year of Fed rate hikes and more stringent bank lending standards. Demand is drawing support from low unemployment, real income growth, and still-lingering excess savings from the pandemic.

Source: Ned Davis Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided herein should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regards the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.