S&P 500 around recessions, plus sector performance, equity positioning, wages, 10-yr Treasury, and the week in review

The Sandbox Daily (12.16.2022)

Welcome, Sandbox friends.

Today’s Daily discusses the S&P 500 index performance arounds recessions, sector drawdowns versus bear markets, NAAIM Exposure Index suggests relatively strong equity positioning, U.S. wage growth continues to slow, a look at the historical record of the U.S. 10-year Treasury, and a brief recap to snapshot the week in markets.

Today was quad witching day, which refers to the simultaneous expiration of market index futures, stock futures, market index options, and stock options at the end of every quarter. The event leads to higher trading volumes and significant volatility, giving speculators an opportunity for quick arbitrage opportunities from last-minute swings. Roughly $4 trillion dollars in options contracts were set to expire today, making Friday the busiest session for options traders this year, noted Rocky Fishman, head of index volatility research at Goldman Sachs.

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 -0.63% | Dow -0.85% | Nasdaq 100 -0.89% | S&P 500 -1.11%

FIXED INCOME: Barclays Agg -0.26% | High Yield -0.53% | 2yr UST 4.182% | 10yr UST 3.488%

COMMODITIES: Brent Crude -2.44% to $79.23/barrel. Gold +0.85% to $1,803.1/oz.

BITCOIN: -3.11% to $16,864

US DOLLAR INDEX: +0.27% to 104.837

CBOE EQUITY PUT/CALL RATIO: 0.73

VIX: -0.92% to 22.62

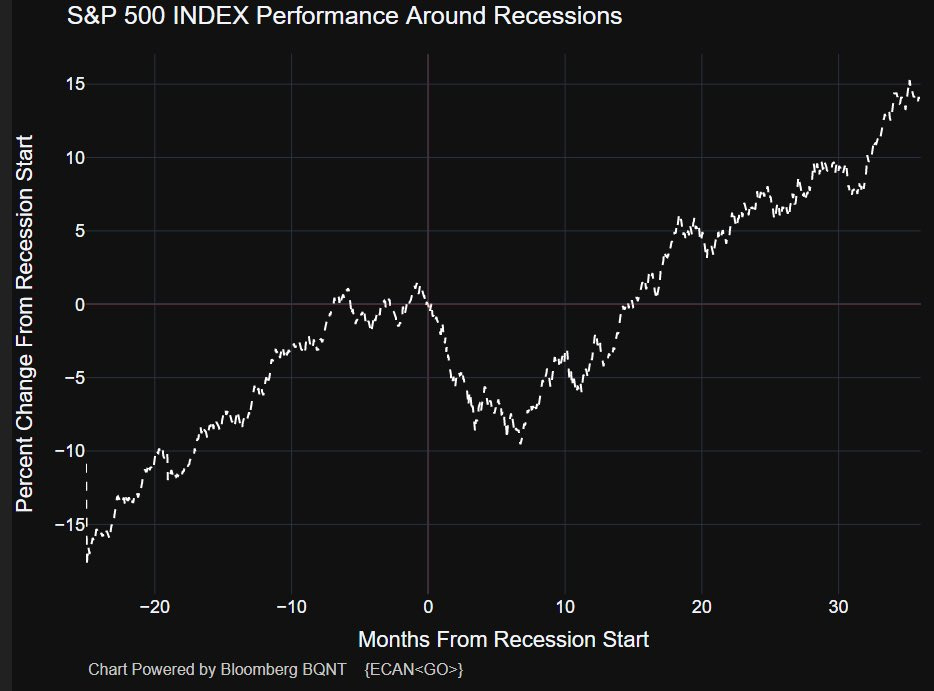

S&P 500 index performance around recessions

On average, the S&P 500 index peaks just before the start of a recession and bottoms about 3-7 months after it began (but before the recession ends). Keep in mind the average recession is ~12-18 months long.

Source: Liz Young

Sector drawdowns versus bear markets

For most sectors, a recession has not been priced in.

Only Consumer Discretionary and Communication Services have seen drawdowns in line with their recession bear averages. The next leg down could be led by more Value-oriented sectors.

Source: Ned Davis Research

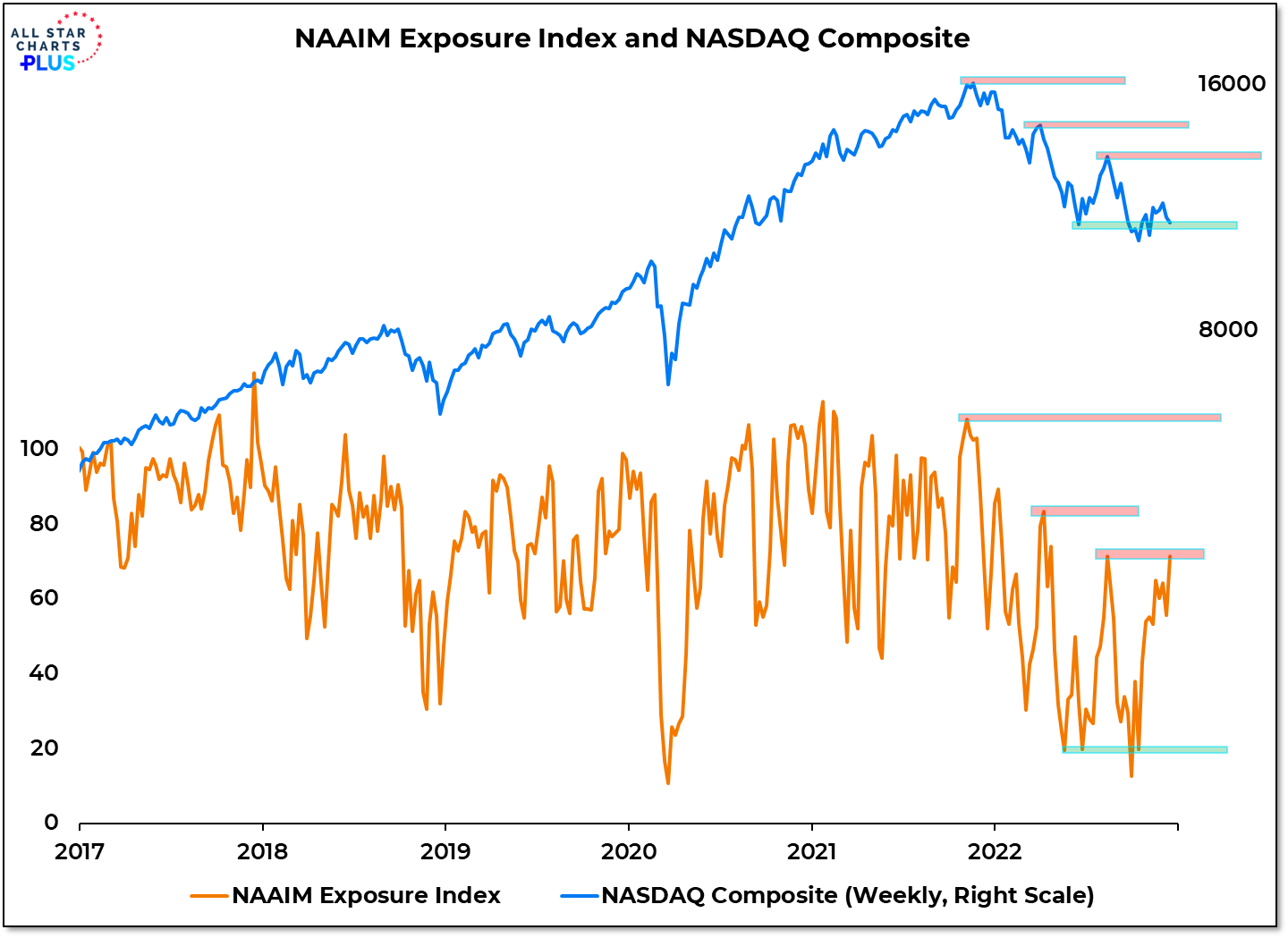

NAAIM Exposure Index suggests relatively strong equity positioning

The National Association of Active Investment Managers (NAAIM) Exposure Index, currently at 71.6, rests at its August high as the NASDAQ Composite tests its June low.

The NAAIM report shows the collective professional money manager’s weekly average exposure to equities.

Source: NAAIM, All Star Charts

U.S. wage growth continues to slow

U.S. wage growth is on track to fall back to pre-pandemic levels by the second half of next year, according to jobs platform Indeed, which has built a new index based on salaries for posts offered via its website.

Wages by that measure were up 6.5% in November from a year ago, after peaking at around 9% in March this year, the gauge shows. The slowdown is broad-based, with more than four in five categories of job seeing lower rates of pay growth than they were six months earlier.

The report stated, “On its current trajectory, the Indeed Wage Tracker would return to its pre-pandemic pace of 3% to 4% year-over-year growth by the second half of 2023. Our measure of wage growth has already peaked, but we are in the early innings of this wage slowdown.”

The Indeed tracker focuses on wages and salaries published in job postings rather than money actually paid to workers. That may make it a leading indicator of broader trends in wage growth, Indeed says.

Source: Indeed

The historical record of the U.S. 10-year Treasury

The U.S. 10-year Treasury note started the year at 1.52%. After topping out at 4.25% on October 24th – possibly the cycle high – the yield is currently 3.48%.

Here is its long, colorful history.

Source: Goldman Sachs Global Investment Research

The week in review

Market drivers: The week started out on a positive note, however, all four benchmark indices closed lower Wednesday through Friday, making it two consecutive weekly losses. With just nine trading days left in the month, the SPX is on track for its third-worst December since 1980. Sentiment continued to lean risk-off on hawkish takeaways from this week's central bank announcements and heightened growth fears. Technical dynamics were also in focus as $4 trillion in option contracts expired today. Some talk of frustrated bulls given the cooler inflation data and an expected seasonal tailwind. However, the path of least resistance has been lower for the better part of the year with bounce attempts repeatedly thwarted by Fed pushback against easing financial conditions and pivot expectations.

Stocks: The major markets finished lower this week as market participants remain concerned about the economic and profits landscape. Investors have been thwarted by the Federal Reserve’s pushback to pivot, given easing economic conditions, especially in light of Thursday’s weaker-than-expected November retail sales report.

Bonds: The Bloomberg Aggregate Bond Index finished the week higher as yields continue to decline on expectations of an economic slowdown. In addition, high-yield corporate bonds, as tracked by the Bloomberg High Yield index, gained ground for the week.

Commodities: Oil and natural gas prices finished the week higher on improved China COVID-19 headlines. As West Texas Intermediate crude oil lost over 42% from the March 8 highs through December 9, traders took advantage of the mark-down in the commodity’s price. The major metals, including gold, silver, and copper finished the week lower.

Source: Dwyer Strategy, LPL Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.