Sector rotation and the bull case

The Sandbox Daily (6.15.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

sector rotation arrives

historical narratives supporting the bull case

Vanguard’s capital market assumptions

5 years of legal sports betting

Retail Sales continue to show consumer strength

Let’s dig in.

Markets in review

EQUITIES: Dow +1.26% | S&P 500 +1.22% | Nasdaq 100 +1.20% | Russell 2000 +0.81%

FIXED INCOME: Barclays Agg Bond +0.70% | High Yield +0.48% | 2yr UST 4.644% | 10yr UST 3.721%

COMMODITIES: Brent Crude +3.27% to $75.59/barrel. Gold +0.09% to $1,970.7/oz.

BITCOIN: -0.83% to $25,369

US DOLLAR INDEX: -0.79% to 102.131

CBOE EQUITY PUT/CALL RATIO: 0.74

VIX: +4.47% to 14.50

Quote of the day

“I wonder if the greatest trick the devil ever played on investors is making them think it is the investing part that matters most.”

- Ryan Krueger, Freedom Day Solutions

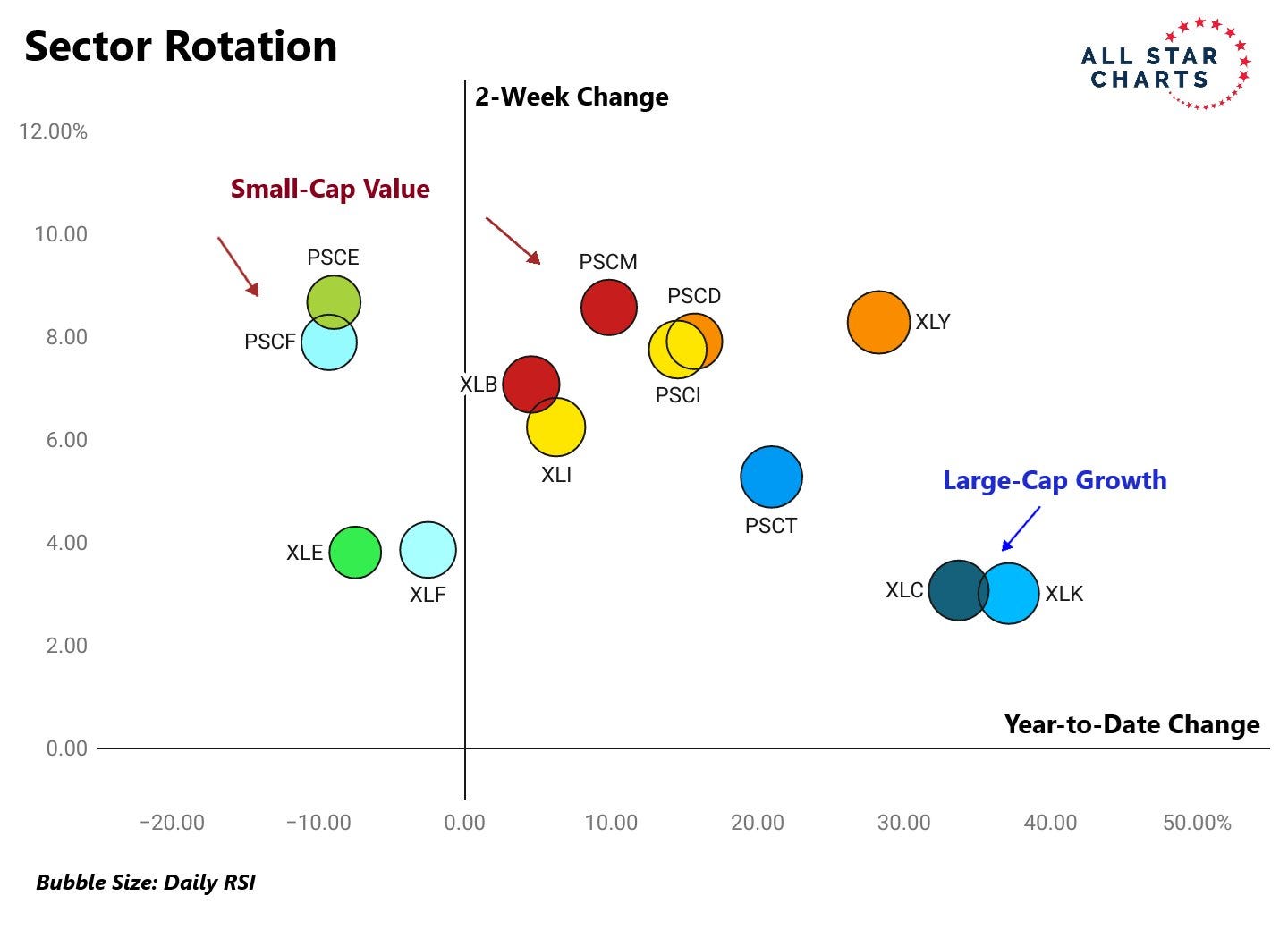

Sector rotation arrives

While many bears and non-believers are questioning the validity of this year’s stock market gains, we continue to see steady improvement recently in lagging sectors catching up to the leaders. After all, they say that sector rotation is the lifeblood of a bull market.

One way to visualize this theme is by looking at the bubble chart below from All Star Charts, as it shows the 2-week performance on the Y-axis and the year-to-date return on the X-axis for a handful of large and small-cap sector ETFs:

As you can see, Technology (XLK) and Communications (XLC) have booked solid gains this year but have lagged over shorter time frames. The opposite is true when looking at the value-oriented sectors and other laggards like small-caps, which have performed the best in the past two weeks.

While this bubble chart illustrates relative strength from the weakest groups over shorter timeframes, the more important takeaway is that all of these sector indexes have been moving higher in recent weeks. This is the kind of expansion in participation that could fuel the stock market rally higher.

Source: All Star Charts

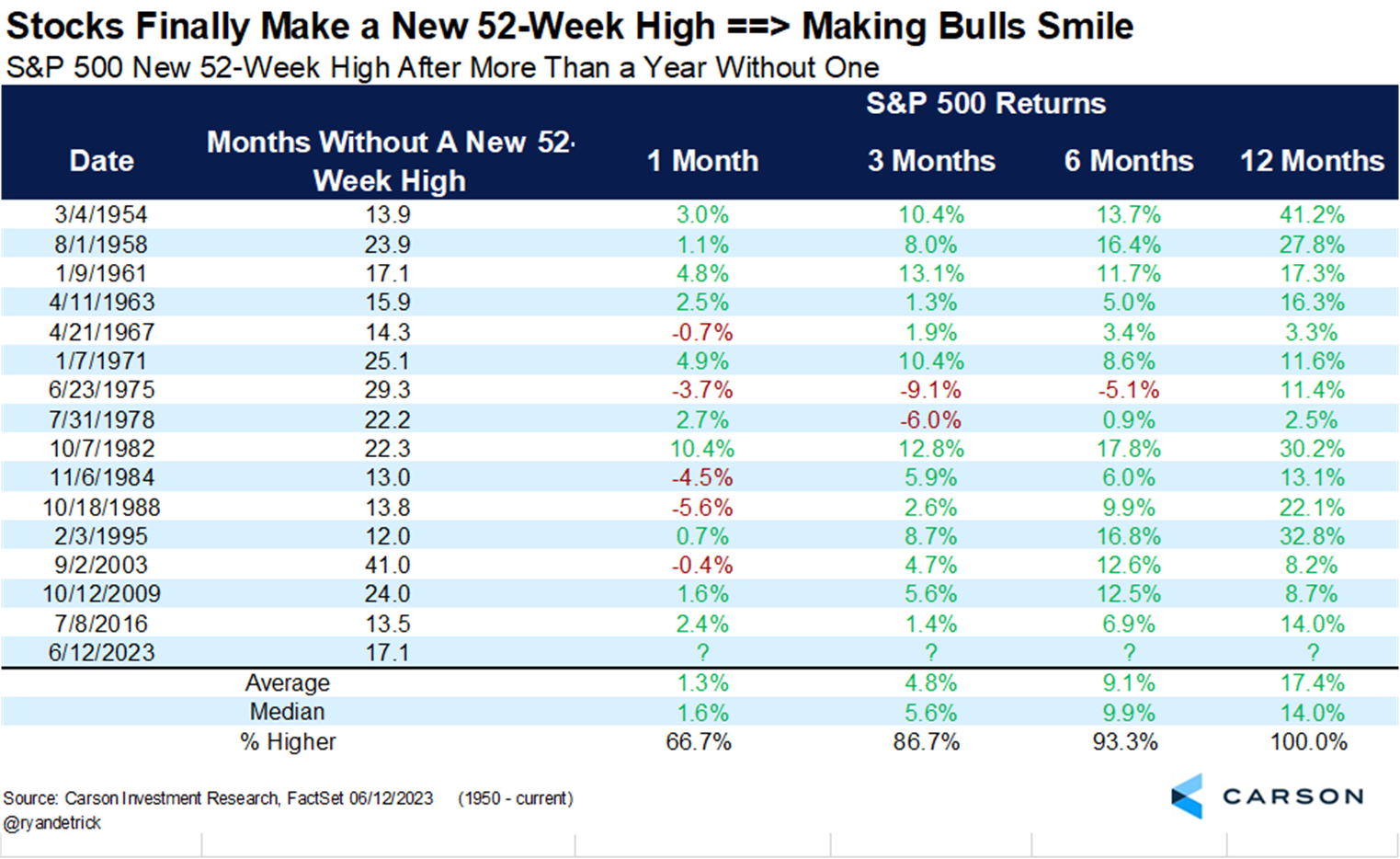

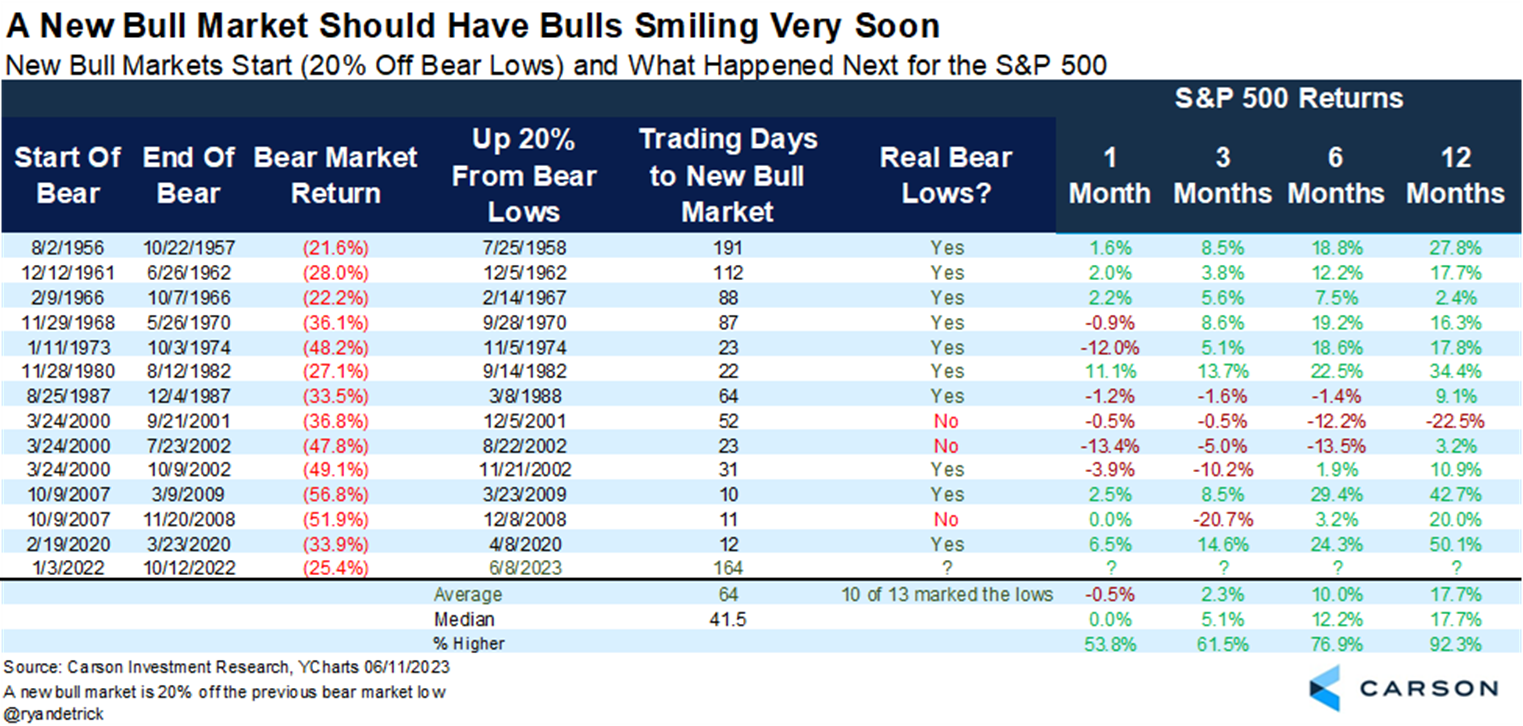

Historical narratives supporting the bull case

Ryan Detrick of the Carson Group puts out excellent data to provide us with historical context around timely and pertinent themes on investor’s minds.

This table below shows that when the S&P 500 Index (SPX) makes a new 52-week high after a year without one – aka the stock market at present time – the index is higher a year later in 15 of 15 instances with a median gain of +14.0%.

But what happens when the S&P 500 Index is up 20% from a bear market low (again, the stock market at present time)? Well, the index is higher a year later in 12 of 13 instances with a median gain of +17.7%.

The new emerging bull market has bulls smiling and bears frowning.

Source: Ryan Detrick

Vanguard’s capital market assumptions

Capital market assumptions quantify the forward-looking risk and return prospects of various investable asset classes. Weighted together, the collection of these assets are the essential inputs to formulating a strategic asset allocation framework – aka, a broadly diversified multi-asset portfolio. After all, asset allocation is the primary determinant of long-run portfolio performance.

Vanguard, one of the world’s largest asset managers, makes their asset class return and volatility assumptions public. Below are the 10-year forward looking forecasts.

One key takeaway here is that Vanguard expects international equities to outperform U.S. equities over the next decade.

Source: Visual Capitalist

5 years of legal sports betting

Just five short years ago, the Supreme Court overturned the Professional and Amateur Sports Protection Act, launching what has become a massive legal sports betting industry.

Business is booming, and it’s a concentrated pool of sportsbook operators at the top – with 90% of the U.S. market controlled by 4 enterprises: FanDuel, DraftKings, BetMGM, and Caesars.

Americans have legally wagered over $220 billion dollars on sports; here are the amounts wagered by state since June 2018:

Source: Axios

Retail Sales continue to show consumer strength

Retail sales – an economic metric that tracks consumer demand for goods – surprised to the upside, climbing +0.3% in May. It was the 2nd consecutive gain, nearly reversing the pullback in spending in late Q1.

While growth has been choppy so far this year, the gains in Q2 point to recent consumer resilience which is supporting overall economic growth.

Retail sales were up +1.7% on a year-over-year trend basis, the slowest pace since July 2020 and weaker than the +4.2% gain per annum in the previous expansion. It shows that consumers have pulled back on spending compared to earlier in this cycle, which consistent with slower economic growth but not yet a recession.

Source: Ned Davis Research, Bloomberg

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.