Selling exhausted, plus the final hike, Treasury refunding, venture, emergency expenses, and the week in review

The Sandbox Daily (11.3.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

incremental signs selling exhausted

equity markets like “the final hike”

Treasury refunding update gives rise to bid in bond market

venture valuations beginning to stabilize

$400 emergency expense

the week in review

Yesterday I met a personal hero of mine, Mark Newton, CMT, an absolute knowledge wizard of financial markets and the discipline of technical analysis. I have tremendous respect for Mark’s work and perspectives on markets.

Then it was over to Making Money to chop it up with Charles Payne.

Fun day in Manhattan.

For now, let’s dig in.

Markets in review

EQUITIES: Russell 2000 +2.71% | Nasdaq 100 +1.21% | S&P 500 +0.94% | Dow +0.66%

FIXED INCOME: Barclays Agg Bond +0.61% | High Yield +0.98% | 2yr UST 4.845% | 10yr UST 4.577%

COMMODITIES: Brent Crude -1.95% to $85.15/barrel. Gold +0.32% to $1,999.8/oz.

BITCOIN: -0.79% to $34,642

US DOLLAR INDEX: -1.01% to 105.047

CBOE EQUITY PUT/CALL RATIO: 0.77

VIX: -4.79% to 14.91

Quote of the day

“You don’t achieve happiness by getting rid of your problems – you achieve it by learning from them.”

-Ray Dalio, Principles

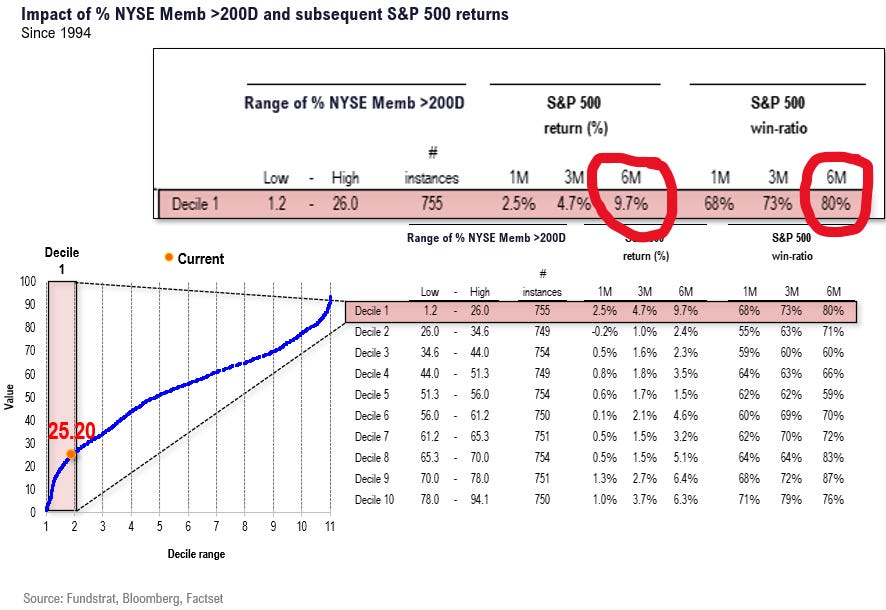

Incremental signs selling exhausted

One structural reason to expect stocks to gain positive traction in the coming weeks focuses on market breadth.

Below is a chart showing the percentage of stocks trading on the NYSE that are trading above their 200 daily-moving-average (DMA), which fell to 25% on October 31st.

The weak breadth measure is a bottom decile reading since 1994.

Over the next 6 months, the median gain for the S&P 500 is +9.7% with an 80% win-ratio.

Source: FS Insight

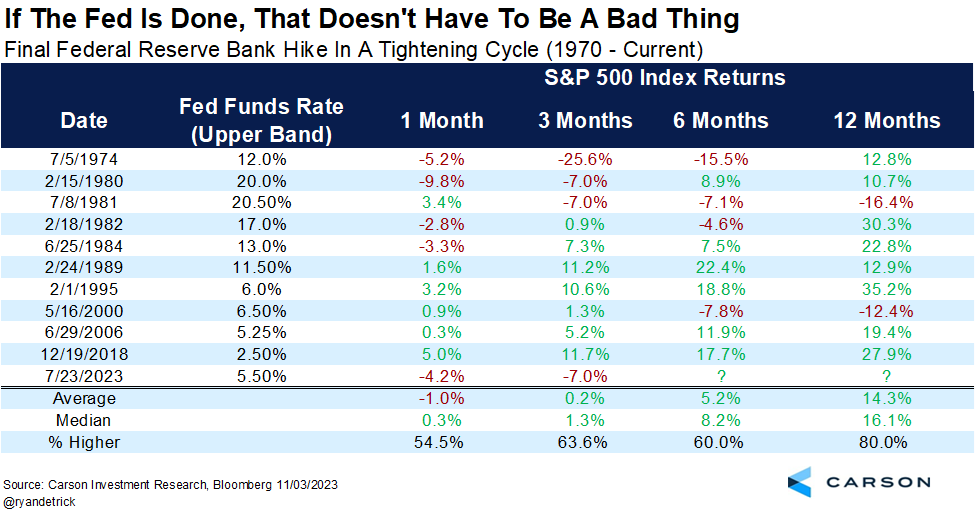

Equity markets like “the final hike”

If the Federal Reserve is in fact done with their interest rate hiking cycle, historical data from the previous 10 tightening campaigns shows the S&P 500 index was up +14.3% on average 12 months later.

Source: Ryan Detrick, CMT

Treasury refunding update gives rise to bid in bond market

Investors were fixated this week on a routine quarterly announcement of how the government plans to finance itself, a sign of how sensitive Wall Street has become to the rapid run-up in interest rates. The update of Treasury’s quarterly process of rolling over maturing debt and financing any new deficits – known as the "quarterly refunding" – helped propel a major move lower in yields this week.

The Treasury is set to borrow $776 billion next quarter, lower than the $1.01 trillion the department borrowed in the July-through-September period which rattled markets over the summer. More importantly, it was lower than market expectations.

Here are the upcoming U.S. Treasury auctions by month:

Also of essential importance was the Treasury announced plans to sell a more modest amount of long-term debt, instead favoring a boost in its plans for shorter-dated maturities – an obvious acknowledgement of the sharp rise in term premium in recent weeks.

The move was immediately celebrated by markets, with the 10-Year Treasury down a whopping ~50 basis points since late October from 5% to 4.5%:

Source: U.S. Department of the Treasury, Bloomberg, Ned Davis Research, The Kobeissi Letter

Venture valuations beginning to stabilize

Venture Capital and Growth Equity managers took the largest markdowns in the 2nd quarter of 2022.

Cumulatively, late stage VC experienced the largest reset in 2022, while early stage VC marks have generally held up well.

Source: StepStone

$400 emergency expense

The share of U.S. adults who said they could cover a $400 emergency expense with cash has dropped for the 3rd quarter in a row to 44%.

Meanwhile, 18% of households outright cannot afford it.

Source: Morning Consult, Bloomberg

The week in review

Talk of the tape: The big story this week was the rally in stocks on the back of a rate reprieve from 1) the removal of Treasury refunding overhang, 2) softer macro data, 3) dovish Jay Powell takeaways, and 4) a less hawkish BoJ policy tweak. The rally in both bonds and stocks were likely helped by positioning dynamics with institutional trading desks flagging the outsized CTA short positions. Stocks are also finding support on favorable seasonal dynamics, the end of October year-end mutual fund selling, and more companies exiting their buyback blackouts. Some mixed sentiment surrounding earnings as while beat rates remain elevated, concerns are growing in regards to underwhelming guidance and the pickup in macro uncertainty messaging.

Stocks: Markets experienced a solid broad-based rally, with a myriad of excuses for the bounce. All sectors were green this week. Unfortunately, the bounce only gets the market back to where it was trading in mid-October!

According to the most recent AAII Sentiment Survey, the percentage of bullish investors declined from 29% to 24%, well below the historical long-term average of 37.5%. At the same time, bearish investors jumped to over 50%, well above the historical average. The overall report reflects strong bearish market sentiment.

Bonds: Rates came off the boil meaningfully this week. The Federal Open Market Committee (FOMC) decided to keep the target range at 5.25 to 5.50%, as expected. While many were closely monitoring the Fed’s decision and subsequent Powell Q&A, the larger move lower in yields came from a Treasury refunding announcement that removed a big overhang on bonds.

Commodities: Commodities had a mixed week as investors deal with a lot of moving pieces and a dangerous geopolitical crisis in the Middle East.

Source: Dwyer Strategy, LPL Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

👍