Small-caps, housing market, Taylor Swift, and the week in review

The Sandbox Daily (7.14.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

no need to hide in large-caps as rally broadens down the cap table

the tight housing market

Taylor Swift makes the Fed Beige Book

a brief recap to snapshot the week in markets

It’s summer Friday. Hope everyone has a great weekend !!

Let’s dig in.

Markets in review

EQUITIES: Dow +0.33% | Nasdaq 100 -0.04% | S&P 500 -0.10% | Russell 2000 -1.01%

FIXED INCOME: Barclays Agg Bond -0.48% | High Yield -0.73% | 2yr UST 4.772% | 10yr UST 3.834%

COMMODITIES: Brent Crude -2.11% to $79.64/barrel. Gold -0.21% to $1,959.7/oz.

BITCOIN: -4.20% to $30,246

US DOLLAR INDEX: +0.21% to 99.976

CBOE EQUITY PUT/CALL RATIO: 0.48

VIX: -1.98% to 13.34

Quote of the day

“If all investment research is based on past data (there is no other data), then any portfolio deemed ‘optimal’ is out of date before it even begins because we are investing into the future. If there are no facts about the future, why bother trying to optimize something that is entirely unoptimizable?”

- Ashby Daniels, CFP®

No need to hide in large-caps as rally broadens down the cap table

Since early May, U.S. small-caps have caught a bid, rallying over 12% and bringing the asset classes’ year-to-date performance to ~10%.

While large-cap indexes have consistently been trading to 52-week highs, small-caps on the other hand are still ~4-5% below their 2023 highs made back in early February.

But, as shown below, the iShares Russell 2000 ETF (IWM) is currently breaking above the top end of the sideways range it has been in over the last month, after successfully holding the key support line cloud around $165-$168.

And the move coincides as momentum – as measured by 14-day Relative Strength Index (RSI) – is continuing to improve off the lows from March and April when the regional banking crisis spiked fears about the economy and credit cycle/conditions, disproportionately affecting small-caps at the time.

The shift in small-cap performance also fits into the broader narrative of breadth expanding from historically narrow leadership in 2023.

Not only does a broadening support the increased risk appetite showcased in recent weeks, but it also supports mean reversion from oversold areas like small-caps. The Russell 2000/1000 ratio (small-caps to large-caps) has held above long-term trend support at the March 2020 lows and has recently moved above its 50-day moving average.

It’s also worth noting that on an absolute basis, the Russell 2000’s pullback during the regional banking crisis did not break the June 2022 lows.

Small-caps tend to be economically sensitive. Recent data has pushed recession risks into 2024, giving small-caps a bigger window to catch up. While not cheap on an absolute basis, small-caps are inexpensive relative to large-caps.

Source: Grindstone Intelligence, Ned Davis Research

No slack in the housing market

The housing market remains tight because 61% of all mortgages outstanding have an interest rate below 4%.

Meaning, this cohort of American homeowners has very little incentive to move homes when they are locked into generational low borrowing rates for the most substantial asset in their personal AND financial lives, especially with mortgage rates currently at 7.25%.

23% of all mortgages outstanding have an interest rate below 3%, while 38% are between 3% and 4%. Just 9% of all mortgages outstanding were originated with an interest rate above 6%.

This is a key reason why the supply in the housing market continues to be so low.

Source: Apollo Global Management

Taylor Swift makes the Fed Beige Book

Taylor Swift is an economy unto itself.

The Fed “Beige Book,” a report published 8 times per year, is a comprehensive review in which each of the 12 regional Federal Reserve banks gather anecdotal information and provide a qualitative assessment of the current economic conditions in their respective districts. Things like local business activity, employment, pricing power, demand, housing, etc.

Here are comments from the Federal Reserve Bank of Philadelphia:

For the uninformed, it is highly unusual for a single person to be called out by the Federal Reserve for impacting local economic conditions.

Swifties are driving business one city at a time as Taylor tours North America on her “Eras” tour.

Source: Federal Reserve, Sam Ro

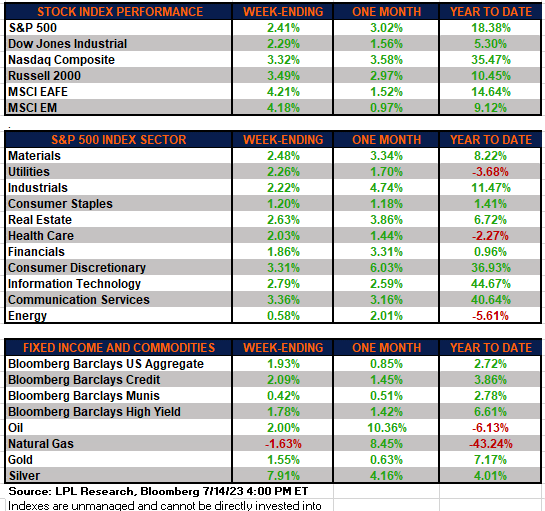

The week in review

Talk of the tape: Market risk remains to the upside. Soft-landing expectations are the key driver of the bullish narrative. Disinflation traction, which was the driver of headlines this week with softer CPI and PPI prints, cited as another tailwind. Consumer resilience, although showing some signs of fatigue, continues to be a bright spot. The Treasury General Account (TGA) rebuild has not been the big drag on reserves and liquidity that many feared. Improvement in market breadth following the longstanding scrutiny around 2023’s narrow mega-cap tech+ leadership flagged as another driver for markets.

Bears remain focused on the higher-for-longer Fed, liquidity headwinds, earnings/margin risk, and lagged effects of policy tightening. Some concerns linger about overbought conditions and stretched valuations. Fedspeak still tilts hawkish.

Markets will shift their attention to 2nd quarter earnings over the coming weeks.

Stocks: All major market indexes ended the trading week higher. June’s improving inflation reports (CPI, PPI) along with better-than-expected earnings from Delta Airlines, PepsiCo, and today’s reports from J.P. Morgan and United Healthcare, helped the averages advance solidly in the green this week. The AAII Investor Sentiment Survey noted that that the percentage of bulls declined over 5% to 41% last week, however it is the sixth consecutive week above the historical 37.5% average.

Bonds: This week’s better-than-expected inflation report had traders believing the Federal Reserve is near the end of its campaign of raising interest rates. Treasury yields were generally lower during the week.

Commodities: Energy prices ended mixed this week with oil higher but natural gas prices lower. The rally in oil could resume – as easing inflation, plans to refill the U.S. strategic reserve, supply cuts from OPEC, and production disruptions curb oil supplies. The major metals (gold, silver, and copper) finished the week higher. The U.S. dollar index reached a 15-month low this week.

Source: Dwyer Strategy, LPL Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.