Soft landing scenario, plus World Bank, Baby Boomers, and emerging markets

The Sandbox Daily (1.11.2023)

Welcome, Sandbox friends.

Today’s Daily discusses the soft landing scenario, the World Bank cuts its 2023 forecast, Baby Boomers at retirement, and emerging markets are running with the bulls.

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +1.76% | S&P 500 +1.28% | Russell 2000 +1.17% | Dow +0.80%

FIXED INCOME: Barclays Agg Bond +0.62% | High Yield +0.66% | 2yr UST 4.221% | 10yr UST 3.543%

COMMODITIES: Brent Crude +3.57% to $82.96/barrel. Gold +0.17% to $1,879.7/oz.

BITCOIN: +0.74% to $17,563

US DOLLAR INDEX: +0.02% to 103.253

CBOE EQUITY PUT/CALL RATIO: 0.64

VIX: +2.48% to 21.09

Soft landing scenario

The macro backdrop remains incredibly uncertain as we begin 2023, with many cross currents suggesting a wide range of outcomes are plausible for both the markets and the economy.

Inflation coming down (somewhat quick and definitively permanent) underpins the soft landing narrative, as it allows the Fed to ease off the brakes and avoid over-tightening financial conditions.

If you are bullish on markets, here are 10 reasons to believe we avert a (deep) recession and/or major market selloff in 2023:

Inflation (both consumer and producer prices) is falling quickly and will approach a reasonable level not too distant from the Fed’s comfort level

Fed framework very likely to change sharply in 2023, as inflation is tracking lower and will lead to fewer hikes in 2023 and a lower terminal rate

The U.S. consumer (largest GDP input) maintains resilience around peak inflation narrative

Labor market strength persists despite corporate cost-cutting initiatives and unemployment rate does not materially move higher

Tailwinds exist for earnings-per-share (EPS) due to weaker dollar, bottoming PMIs, and supply chains easing

The reset is done: the forward P/E multiple is now 16.65x, in line with the 25-year average of 16.82x and well off the recent high of 22x

Historically weak investor sentiment and positioning offer contrarian catalysts

Equities post a +22% average gain following a negative high-yield return year as credit rebounds

Rare for back-to-back negative equity years; since WWII, 21 instances of annual declines yet only 3 times of 2 consecutive years (1973-1974, 2000-2002)

China pivoting away from zero-Covid policy opens up the 2nd largest economy

Having reviewed both the bull and bear cases, it’s fair to say risks remain to both the upside and downside.

Source: Fundstrat, Canaccord Genuity

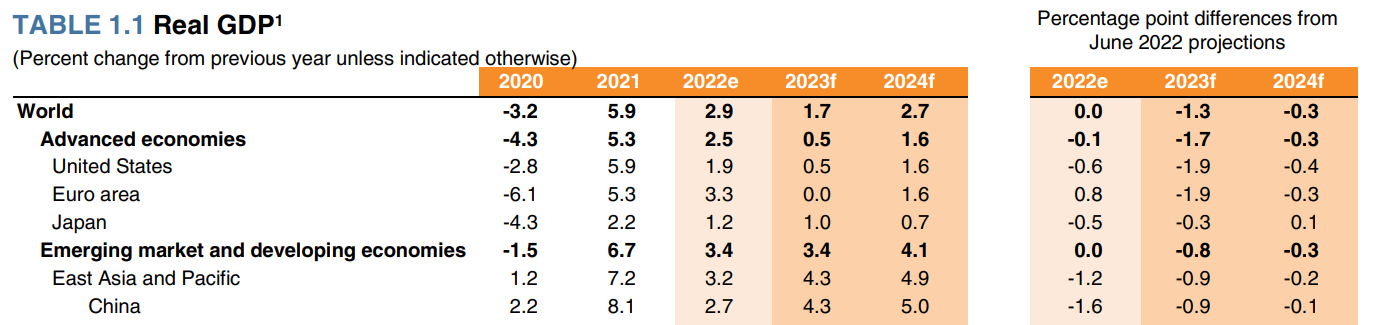

World Bank cuts 2023 forecasts and warns of global recession

The World Bank has slashed its global growth forecasts – down to +1.7% from its mid-2022 projection of +3.0% – on the heels of what it sees as broadly worsening economic conditions. The adjustment was led by a significant downgrade to its prospects for the U.S. economy — it now forecasts +0.5% growth from an earlier estimate of +2.4%.

The downgraded estimates would mark “the third weakest pace of growth in nearly three decades, overshadowed only by the global recessions caused by the pandemic and the global financial crisis,” the World Bank said.

It noted the combination of slower growth, tightening financial conditions, elevated geopolitical tensions, and heavy indebtedness is likely to weaken new investment and weigh on the business cycle.

The World Bank said that tighter monetary policies from central banks around the world may have been necessary to tame inflation, but they have “contributed to a significant worsening of global financial conditions, which is exerting a substantial drag on activity.”

*Note: EMDEs are emerging market and developing economies

Source: World Bank, Wall Street Journal

Baby Boomers

The U.S. job market has staged a remarkable rebound since the start of the pandemic almost three years ago. The latest government data showed that 2022 was one of the best years on record in terms of raw job growth – adding an average of 375,000 jobs per month.

Yet the number of people available to work remains substantially smaller as a share of the population than before the pandemic, and some key economic policymakers seem to have all but given up hope that it will grow much in the years ahead. Last month, Federal Reverse chair Jerome Powell noted the country has a “structural labor shortage” that is unlikely to be resolved anytime soon. If correct, the Fed’s prediction has big implications for the U.S. economy.

One area of focus is the Baby Boomer generation – the outsize importance of this cohort is the result of the generation’s size with some 76 million Americans being born between 1946 and 1964. Today, nearly all of them are in their 60s and 70s, and well over half are past the traditional retirement age of 65, as this chart shows:

Baby Boomers are now juggling a confluence of factors when considering their future employment prospects: greater life longevity (money shortfall risk), better healthcare, shifting industry patterns (more office jobs, less factory jobs), higher wages, work-from-home arrangements, financial necessity (like 2009, this bubble has deflated many retirement accounts), and opportunity costs.

Source: New York Times

Emerging markets are running with the bulls

It’s hard to ignore the recent strength of certain asset classes since the U.S. dollar internals peaked in the fall of 2022. Since October 24th, the MSCI Emerging Markets index is up +20.32%, which clears the textbook definition of a new bull market. China’s reopening hasn’t hurt either, given the country’s enormous weighting (33.36%) in the index.

There’ve been plenty of false alarms over the last decade or two, but emerging market stocks are in a rally that looks like it could end a slump against U.S. stocks that has stretched back to 2010.

This is only the 8th time in 35 years that EM has jumped 20% or more from at least a two-year low, according to Jason Goepfert of SentimenTrader. Further, this has been the longest the index has had to wait before making such a rally. Both bullish technical developments.

Source: Bloomberg

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.