State of the Union, plus credit spreads, mortgage applications, Fed Funds, and 99% of investing

The Sandbox Daily (2.8.2023)

Welcome, Sandbox friends.

Today’s Daily discusses the State of the Union, credit spreads remain in check, easing mortgage rates cause mortgage application to rise, understanding the Fed Funds curve (reality vs. expectations), and 99% of good investing is doing nothing.

Let’s dig in.

Markets in review

EQUITIES: Dow -0.61% | S&P 500 -1.11% | Russell 2000 -1.52% | Nasdaq 100 -1.83%

FIXED INCOME: Barclays Agg Bond +0.14% | High Yield -0.42% | 2yr UST 4.427% | 10yr UST 3.601%

COMMODITIES: Brent Crude +1.10% to $85.02/barrel. Gold +0.18% to $1,887.3/oz.

BITCOIN: -1.32% to $22,948

US DOLLAR INDEX: +0.04% to 103.470

CBOE EQUITY PUT/CALL RATIO: 0.60

VIX: +5.20% to 19.63

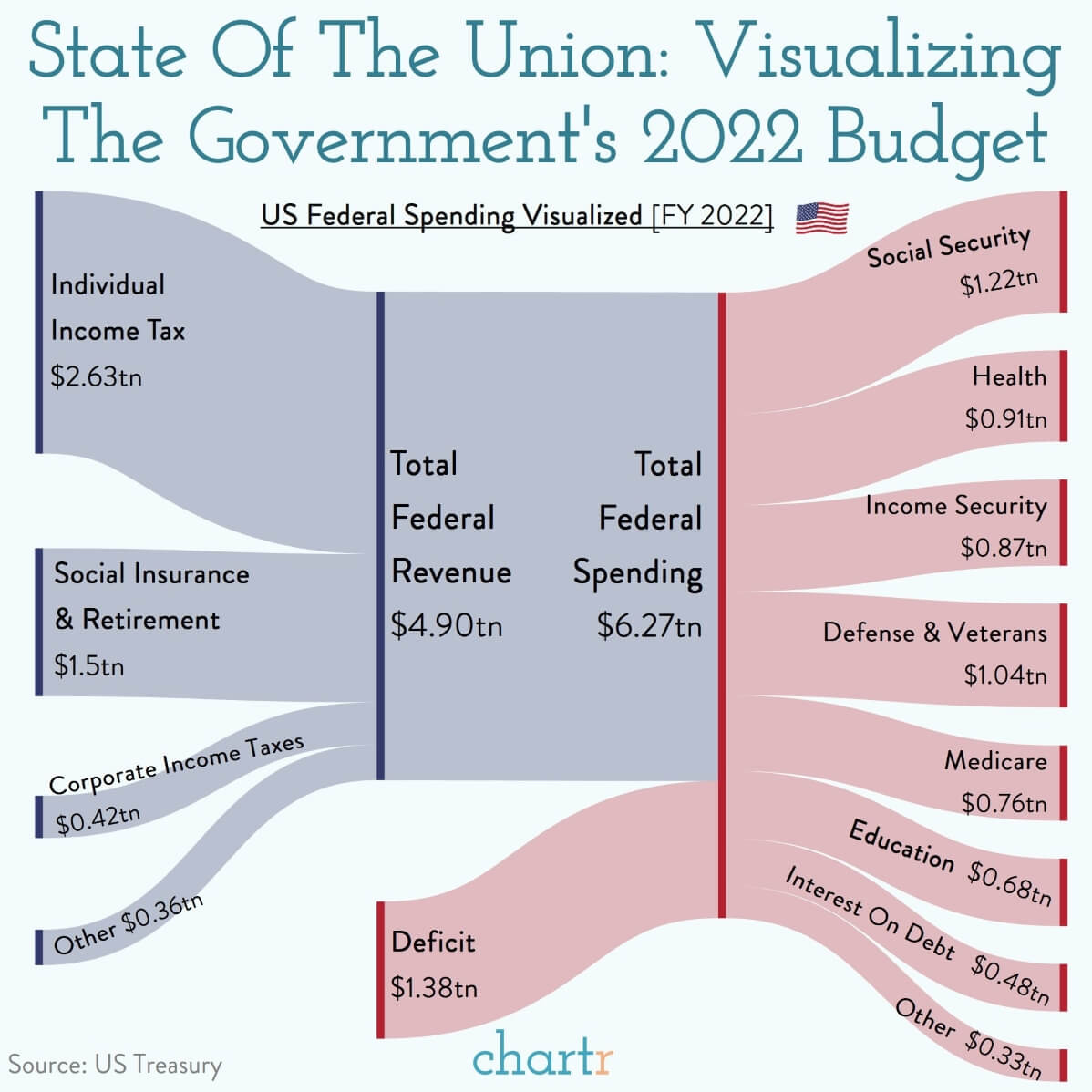

State of the Union

Last night, President Biden held the annual State of the Union, addressing the country on what is often dubbed the biggest night of the year in Washington. A big theme from the 72-minute speech, Biden’s longest of his presidency so far, was the economy.

The latest budget from the U.S. Treasury reveals that, in fiscal year 2022, the federal government collected nearly $5tn in revenue, with more than 50% of that coming from individual income taxes. However, the US government spent even more, leading to a nearly $1.4tn deficit. That’s a hard-to-comprehend-number, but it is substantially lower than the $3tn+ deficit recorded in 2020 during the depths of the pandemic.

To make up the difference the US government does what everyone who overspends their budget does — they borrow. This then adds to the already enormous tab (AKA the national debt), which currently sits at the $31.4tn debt ceiling limit, a topic which received a fair amount of audience participation when brought up in Biden’s speech.

With a debt pile that big, the interest payments aren’t small. Indeed, last year the US government spent ~$480bn on net interest payments, just shy of Ireland, Norway or Nigeria’s annual GDP.

Source: Chartr

Bonds aren’t stressed

When markets are under stress, it shows in credit spreads.

The bond market is the biggest segment of the capital markets, with a total valuation approaching $120 trillion. If there’s serious systemic risk in the stock market, credit spreads will notify investors. So far, these spreads are narrowing, not widening.

Below is an overlay chart of the S&P 500 ETF (SPY) with the High Yield Corporate Bond ETF (HYG) and U.S. Treasury Bond ETF (IEI):

Notice how these lines have moved in tandem over the trailing twelve months. When the HYG/IEI ratio is falling (and credit spreads are widening), stocks tend to come under increased selling pressure.

On the flip side, equities benefit when credit spreads contract, and that’s exactly the environment they’re in now.

With more stocks making new 52-week highs and participation expanding to last year’s laggards, stock market bears have little to support their thesis.

Source: All Star Charts

Mortgage applications increase

Mortgage rates continued to decline last week, spurring more volume in mortgage applications. The conventional mortgage rate fell for the 4th consecutive week to 6.18%, its lowest level since last September, and down nearly 1% from its peak in November of 2022.

As a result, mortgage applications increased +7.4% from one week earlier. The Refinance Index gained +17.7%, while the Purchase Index was up +3.1%.

However, on a YoY trend basis, refinance and purchase applications are down -77.8% and -35.1%, respectively. Although this reflects that housing market activity is much weaker than a year ago, it also shows a marginal improvement from the lows observed in late 2022.

Mortgage applications are one gauge that gives investors an early look at housing demand. The readings are of particular interest as the housing market approaches its normally busy spring season. Higher rates tempered buyer demand in late 2022, but recent data, including the Mortgage Bankers Association gauges as well as pending home sales and comments from builders, have indicated that buyers could be returning to the market.

Source: Mortgage Bankers Association, Ned Davis Research

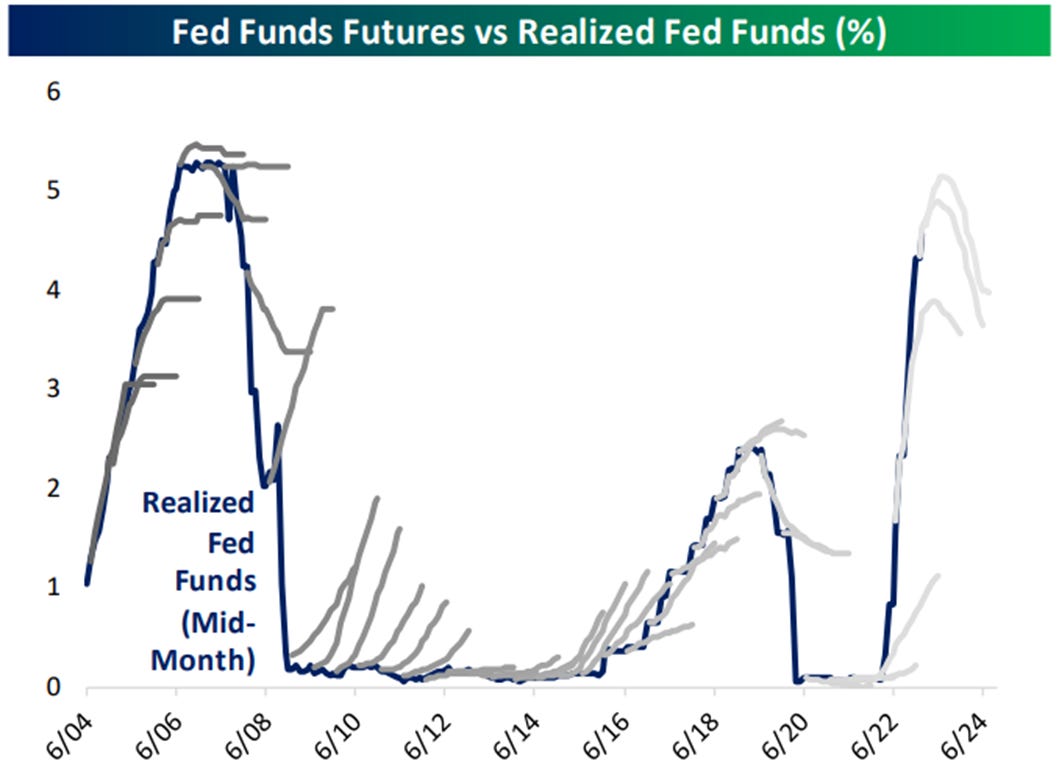

What the short-term interest rate market is pricing

Here is a chart that shows the pricing of Fed Funds futures for 18 months forward. Curves are presented every 6 months and compared to the actual Fed Funds rate that played out. A few things to note about history and what to expect later this year when the Fed hits the “pause” button on their rate hikes.

First, the current hiking cycle has been broadly similar to the last two, with the Fed Funds market persistently underpricing the trajectory of the Fed Funds rate.

It’s also notable that around monetary policy turning points in both 2006 and 2019, Fed Funds futures did a decent job capturing the turn in monetary policy as it happened.

Finally, the current market pricing for the Fed Funds rate involves much more aggressive cuts than what was priced at the last two finales; in both the mid-2000s and the late-2010s the market never priced more than 50 bps of cuts, yet this time around the pricing is more like 175 bps (i.e. three times as steep as the last two peak Fed Funds rates periods).

Source: Bespoke Investment Group

99% of good investing is doing nothing

It’s hard to sit there and do nothing. Often, it feels impossible.

The urge to tinker with a new idea or indulge our latest impulse often overwhelms our senses, especially in financial markets where the information changes every minute and someone is always stating something to the contrary.

While counterintuitive to most things in life, sometimes the best path forward for your portfolio is to sit there and do nothing.

Block out the noise.

Source: Brian Feroldi

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.