Stock performance around easing cycles, plus the alphabet portfolio, commercial real estate, housing market, and Warren Buffett

The Sandbox Daily (8.28.2024)

Welcome, Sandbox friends.

Congrats to Warren Buffett and the late Charlie Munger whose Berkshire Hathaway achieved $1 trillion in market cap today – a crowning achievement in their long and storied investment careers. 🎉🍾

Today’s Daily discusses:

the alphabet portfolio

rate cuts mean what exactly…

unthawing the commercial real estate market

housing becomes a key issue in upcoming U.S. election cycle

Let’s dig in.

Markets in review

EQUITIES: Dow -0.39% | S&P 500 -0.60% | Russell 2000 -0.65% | Nasdaq 100 -1.18%

FIXED INCOME: Barclays Agg Bond -0.09% | High Yield -0.05% | 2yr UST 3.873% | 10yr UST 3.844%

COMMODITIES: Brent Crude -0.92% to $78.82/barrel. Gold -0.42% to $2,542.2/oz.

BITCOIN: -4.83% to $59,162

US DOLLAR INDEX: +0.55% to 101.108

CBOE EQUITY PUT/CALL RATIO: 0.70

VIX: +10.89% to 17.11

Quote of the day

“Stock moves start with technicals, are confirmed by fundamentals, and end with emotion.”

- Darren Chabot

The alphabet portfolio

We are kicking off today’s newsletter with some fun – it’s trivia time !

While most of the investable universe of stocks, ETFs, and mutual funds use 2-, 3-, 4- and 5-digit tickers, the truly exclusive symbols sit atop the kingdom in the 1-letter universe. As fate would have it, all eleven major GICS sectors are represented in the Alphabet Portfolio.

Go ahead – see how many companies you can name on this list of 21 stocks.

We will reveal the unencumbered list tomorrow.

Source: Bespoke Investment Group

{kind=link}

The burning question on everyone’s mind

Like most things in life, it depends…

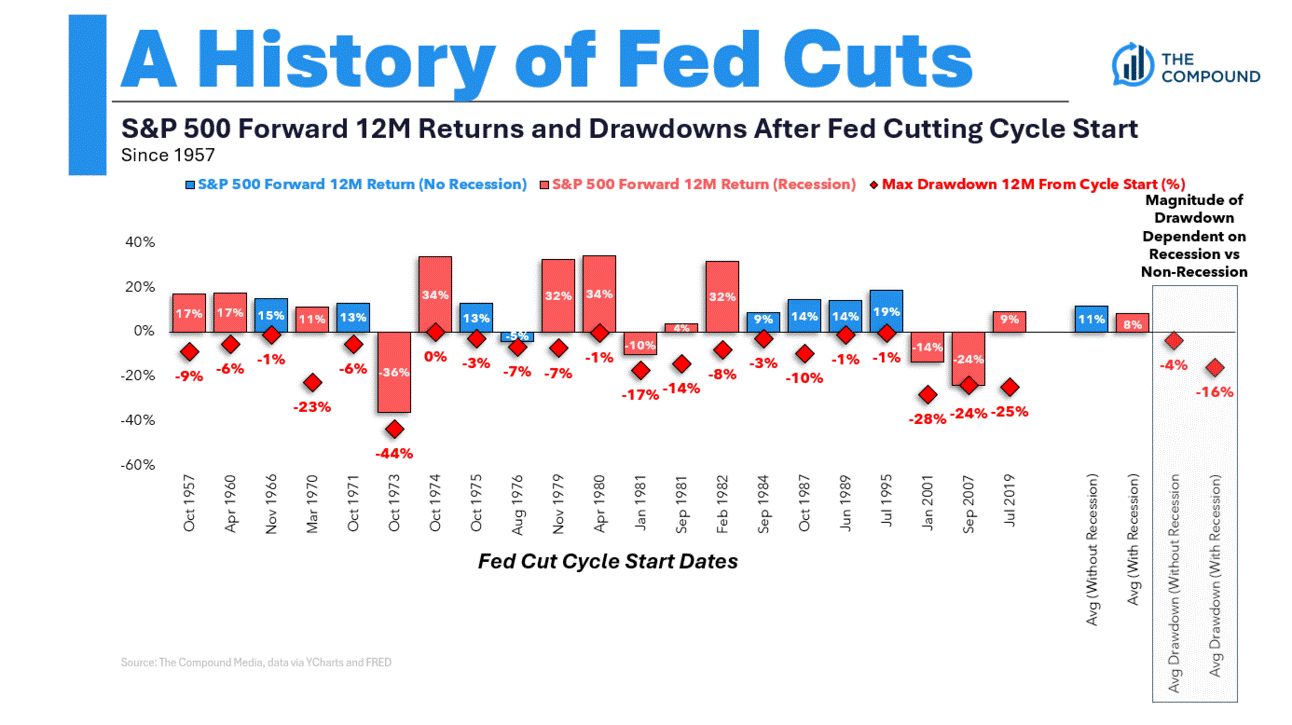

With the Federal Reserve set to cut interest rates on September 18, many investors are wondering what happens next. The question on everybody’s mind these days is “what happens to stocks after the first rate cut?”

The answer?

Well, that depends.

Unfortunately, the historical sample size of Fed rate cutting cycles is rather small (read: not ideal), but if we look for historical analogs to level set expectations on a go-forward basis, one doesn’t need a Ph.D. to see the forward 12-month stock performance after the first rate cut is all over the map.

Some cycles experienced blistering gains, others saw gut-wrenching selloffs, and the rest fell somewhere in the middle.

The significant caveat in the historical data depends on whether or not the U.S. economy was concurrently sliding into recession as the Fed downshifted its policy into an easing cycle. Are the cuts on a (reactionary) emergency basis or (proactive) normalization basis?

Recessionary environments are the X factor. If a recession is imminent, the market is fine but the pilot has switched on the safety belt light. If no recession, cue the bubbles and caviar.

Matt Cerminaro of Fundstrat and Ritholtz fame put together this unbelievable chart that tells it all. Since the 19050s, the key takeaways from the equity market are:

S&P 500 is higher 16 of 21 instances, or 76% of the time

average gain is +11% without recession

average gain is +8% with a recession

if no recession, the average drawdown is -4%

if recession, the average drawdown is -16%

You will also notice the vast amount of red diamonds – which represent the max drawdown from the start of the easing cycle – are relatively benign. In fact, many look like drawdowns that we experience every year in the market, such as the one we experienced earlier this month during the Yen carry trade unwind.

However, there are several pullbacks that pierce the -20% threshold that would represent a painful environment for any long investor.

This cycle has proven unique in many ways as the economy has become increasingly disjointed from history ever since the covid-19 pandemic disrupted time as we know it. In fact, it can often be hard to know what to make of the U.S. economy.

Inflation reached multi-decade highs after barely a scent of it for 20 years. A number of recession indicators, like an inverted yield curve and the Conference Board’s Leading Economic Indicators (LEI), have called for a looming recession the better part of two years. On the other hand, GDP growth and corporate profits have remained solid, while the job market has proven resilient amongst all its doubters.

Given the wide range of historical outcomes and chameleon-like nature of this economy, we should not be surprised when the market responds in ways that are entirely out of consensus from the base case narrative.

Source: Josh Brown, Ned Davis Research

Unthawing the commercial real estate market

No asset class is more excited at the prospects of lower interest rates than commercial real estate.

The “commercial property” category encompasses a diverse mix of property types beyond just offices – such as retail, hotel, multi-family, warehouses, light industrial, and distribution centers. Despite office valuation declines, most other property classes are performing quite well in local municipalities, helping to offset the post-pandemic decay from reduced office footprint.

U.S. commercial real estate prices have essentially troughed after declining over the last 1.5-2 years. At its nadir, the MSCI National All-Property Index posted a -10.8% YoY decline.

More recently, the index has posted three consecutive monthly increases from May to July.

Weakness in the office portion of commercial real estate will have a financial impact, but it is likely to be staggered over a number of years due to the lag in the reassessment processes and lack of transaction activity.

Commercial property tax revenues generally make up about 10% of the total tax bases of major cities, so early signs of stabilization are good for not just the lenders and investors but also the localized economy.

“The downturn in property prices appears to be behind us now, as pricing has stabilized this year,” said Peter Rothemund, Co-Head of Strategic Research at Green Street. “For most property types, values are modestly higher than they were at the beginning of the year.”

Source: MSCI, Green Street Commercial Property Price Index

Housing becomes a key issue in upcoming U.S. election cycle

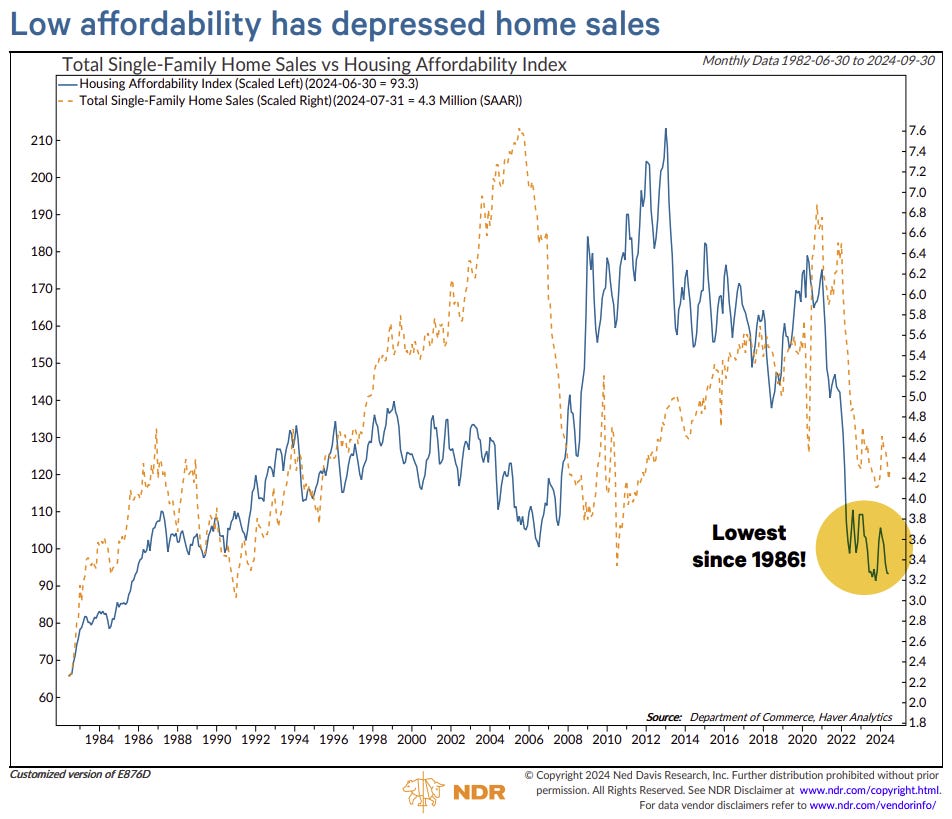

One of the pressing issues in the 2024 election cycle has been housing affordability, as high mortgage rates and elevated home prices, fueled by a housing shortage dating back to the Global Financial Crisis, have kept homeownership out of reach for many prospective homebuyers.

Housing affordability in the post-pandemic era has been near its lowest level since the 1980s and is weighing mightily on home sales.

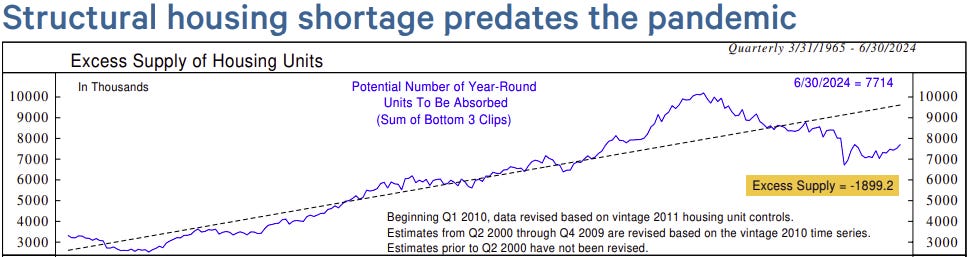

More than in other election cycles, both presidential hopefuls have acknowledged that the housing shortage and underinvestment in housing construction since the GFC is the root problem.

Based on a deviation from trend basis, Ned Davis Research estimates a housing shortage of ~1.9 million units.

Source: Ned Davis Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.