Stocks at critical technical levels, plus GDP growth, gas prices, ChatGPT, and financial security

The Sandbox Daily (1.26.2023)

Welcome, Sandbox friends.

Today’s Daily discusses the S&P 500 index challenging multiple levels of interest, 4th quarter GDP growth, the recent rise in gas prices, the buzz surrounding ChatGPT, and exploring financial security.

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +2.00% | S&P 500 +1.10% | Russell 2000 +0.67% | Dow +0.61%

FIXED INCOME: Barclays Agg Bond -0.17% | High Yield +0.25% | 2yr UST 4.189% | 10yr UST 3.504%

COMMODITIES: Brent Crude +1.65% to $87.54/barrel. Gold -0.66% to $1,946.5/oz.

BITCOIN: +0.42% to $23,045

US DOLLAR INDEX: +0.17% to 101.815

CBOE EQUITY PUT/CALL RATIO: 0.75

VIX: -1.83% to 18.73

S&P 500 challenges resistance

The S&P 500 (SPY) started the year on strong footing, but more recently price is halting at a logical level of overhead supply.

As you can see, the 200-day moving average (MA), the anchored VWAP from all-time highs, and a downward-sloping trendline are all converging in the same area, setting up a powerful confluence of resistance.

As long as we're below this critical level, the trend could remain lower at the index level.

However, if and when buyers absorb all the overhead supply and reclaim this level, it could confirm the recent rally and lead to sustained moves higher.

Despite the overwhelming supply for the S&P 500, we operate in a "market of stocks" rather than a "stock market," with prospects varying among different industry groups and sectors.

Source: All Star Charts

Solid Q4 real GDP growth but momentum slowing

The U.S. economy beat expectations in the last quarter of 2022, posting the kind of mild slowdown that the Federal Reserve wants to see as it attempts to tame inflation without choking off growth.

Real GDP increased at a +2.9% annualized rate in Q4, slightly above the consensus of +2.8%, as the economy finished the year on a positive note. While growth was slower than the +3.2% annualized gain in the previous quarter, it confirmed that the economy was not in recession in Q4. Growth in the 2nd half of 2022 more than reversed the two consecutive quarterly declines in the first half of the year.

As a result, on a total annual basis, real GDP increased 2.1% in 2022.

In Q4, there were positive contributions to growth from consumer spending (PCE in the chart below), inventory investment, net exports, and government spending. Capex growth slowed, while residential investment (!!) continued to contract.

For the Fed, which has hiked interest rates at the steepest pace in a generation over the past year, the data suggest that there’s still a path to what’s known as a “soft landing.” That’s a scenario in which tighter monetary policy cools household spending and lowers inflation – but avoids squeezing the economy so hard that it ignites mass layoffs nationwide.

Source: Bloomberg, Ned Davis Research

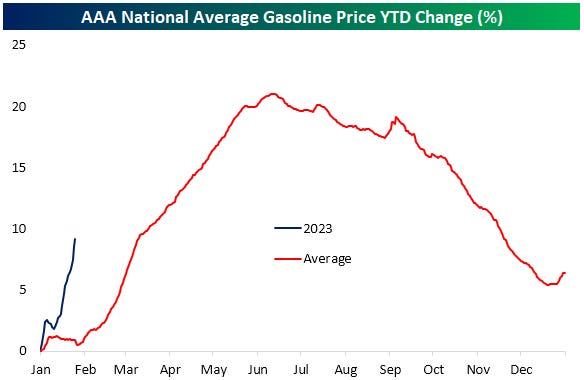

Gas prices starting to rise again

The second half of 2022 saw gas prices give up more than the cumulative increases from the first six months of 2022, as AAA's reading on the national average for a gallon of regular hit a low of $3.096 on December 22nd – the lowest price since June 2021. Although prices at the pump are much lower than 1H22, they are starting to rise again.

Roughly one month out from the lows, national average gas prices have risen +12.9% for the sharpest 1-month increase since last June. As shown below, double-digit MoM increases in gas prices are far from without precedent – in fact, gas prices month-to-month are volatile.

What’s somewhat unusual is when during the year that increase has taken place. Trends in gas prices tend to be seasonal with increases in the first half of the year and declines in the second half. In what has been a seasonally unusual pattern, prices are rocketing higher already. Whereas prices have historically risen an average of less than 1% year to date through 1/26, this year the increase has been 9.16%.

Source: AAA, Bespoke Investment Group

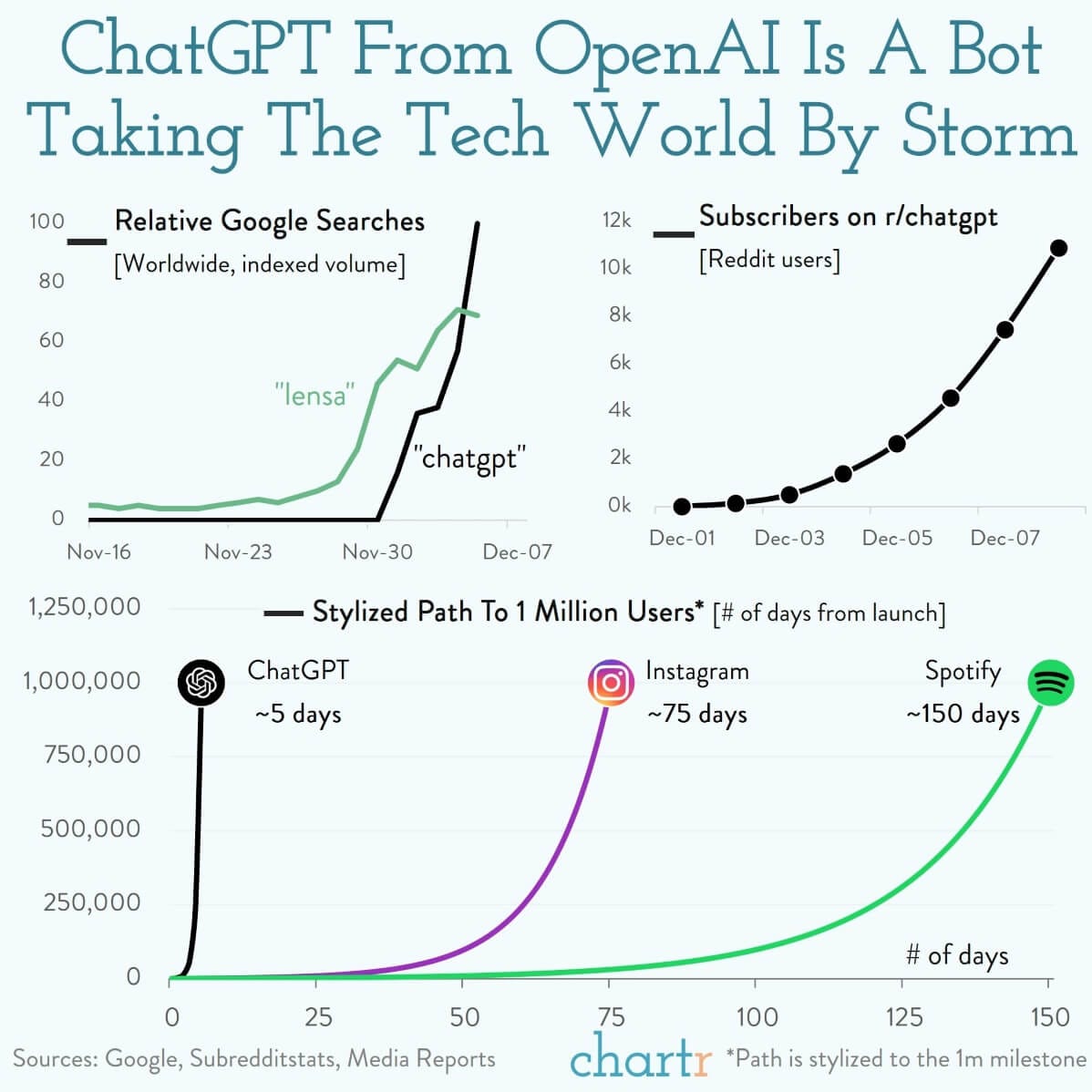

ChatGPT is all the buzz

The super-easy-to-use functionality of ChatGPT has gone viral, with OpenAI reporting that ChatGPT hit 1 million users in just the first 5 days.

Roughly two months after its release, ChatGPT may have pushed artificial intelligence into the mainstream. Its ability to hold long dialogues, answer questions, and compose almost any kind of written material are the reasons for gravitational pull towards adoption. So much so that Microsoft is pouring $10 billion dollars into OpenAI, which has Google nervous about its own search engine.

ChatGPT seemingly knows enough to write academic essays, create/debug code, and explain quantum mechanics in a way that our physics teachers never could. Now more than ever the question of when, not if, AI will replace jobs is at the forefront of people’s minds.

But just how popular is this chatbot worldwide? Searches for ChatGPT have skyrocketed. Data from Google Trends shows the top 5 countries with the largest search interest in ChatGPT are China, Nepal, Singapore, Israel, and Lebanon. The United States only comes in at 29!

Google Trends also shows us the first major uptick in popularity came at the end of November, and it only took 1 month to reach peak popularity by January. Is this the peak or will we see continued durable interest in the months and years to come?

The possible uses for ChatGPT, and the future versions of it to come, are equal-parts exciting and daunting. If optimized further, it’s not hard to see a way it could threaten the dominance of search giant Google for certain queries, or the potential to revolutionize some manual tasks in nearly every knowledge-based industry.

Source: Chartr, Genuine Impact

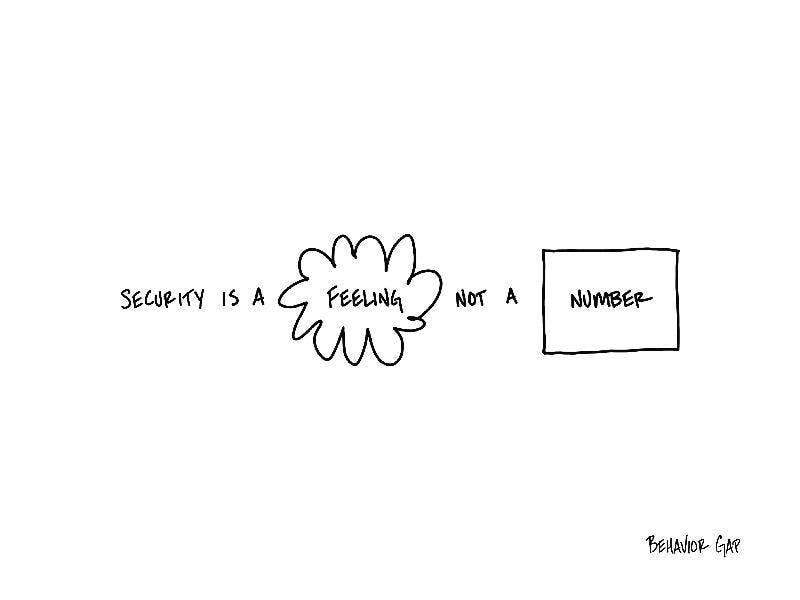

One simple graphic

Here is behavioral finance guru, Carl Richards, with some food for thought.

Here’s a paradox:

I know people who have more money than they will ever need but are totally insecure.

I know people who have almost nothing but are totally secure.

The conclusion this forces me to draw is that if security exists at all, it is a feeling… not a number.

The good news is that means we can have some control over it.

The bad news is that means it’s up to us to learn how.

Source: Carl Richards

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.