Temporary shock, permanent rally?

The Sandbox Daily (4.20.2026)

Welcome, Sandbox friends.

After a brief spring break hiatus, we are back to our regularly scheduled programming.

Today’s Daily discusses:

what the market is pricing in

Let’s dig in.

Blake

Markets in review

EQUITIES: Russell 2000 +0.58% | Dow -0.01% | S&P 500 -0.24% | Nasdaq 100 -0.31%

FIXED INCOME: Barclays Agg Bond -0.01% | High Yield -0.09% | 2yr UST 3.721% | 10yr UST 4.252%

COMMODITIES: Brent Crude +5.32% to $95.19/barrel. Gold -0.92% to $4,834.8/oz.

BITCOIN: -1.57% to $75,973

US DOLLAR INDEX: -0.04% to 98.05

CBOE TOTAL PUT/CALL RATIO: 0.66

VIX: +7.95% to 18.87

Quote of the day

“We don’t heal in isolation, we heal in connection.”

- Esther Perel

What the market is telling us

Step back and the market’s message is actually quite consistent:

The Iran conflict is not being treated as a growth shock. It’s being treated as a temporary inflation shock.

That distinction matters.

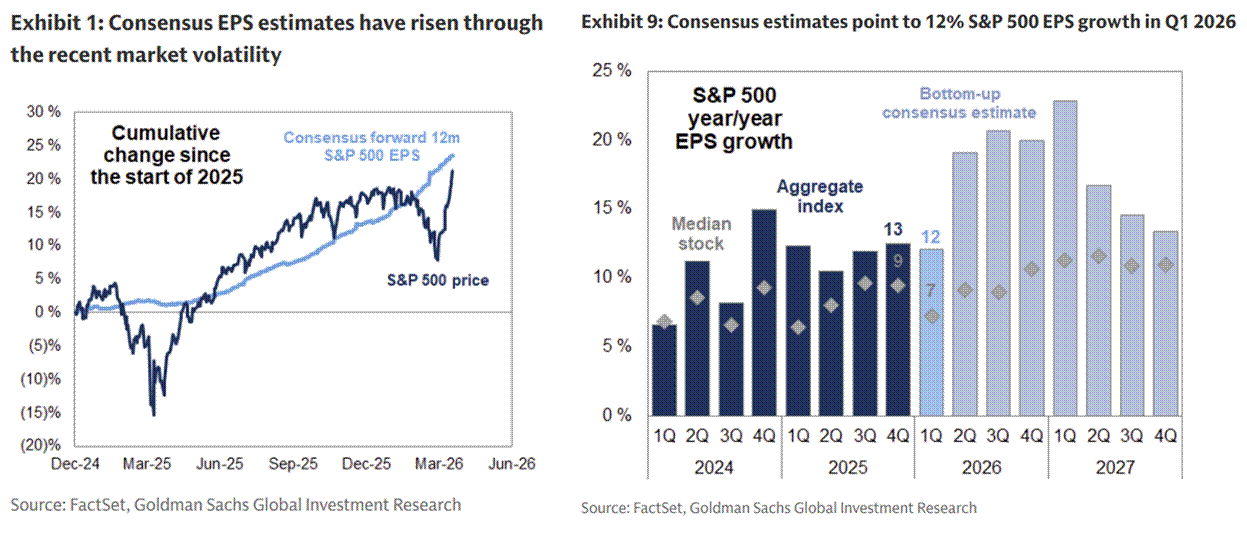

Over the past few weeks, despite rising oil prices and geopolitical uncertainty, earnings estimates have continued to move higher, not lower. That tells you everything you need to know about how investors are framing the environment.

Markets are looking through the noise.

They’re betting the economic slowdown remains shallow, inflation pressure from energy is temporary, and, most importantly, earnings will hold.

Because historically, markets don’t sell off on short-term disruptions. They sell off on sustained earnings deterioration or an abrupt tightening in financial conditions.

So far, neither has materialized.

That brings us to where we are today.

The setup is no longer theoretical. It’s execution-dependent.

From here, the market needs:

The ceasefire to hold, or at least not materially worsen

The U.S. economy to prove it hasn’t rolled over

Mega-cap tech to deliver on elevated expectations

After the surge in Technology stocks and a sharp market recovery, the bar has been raised. Expectations remain high.

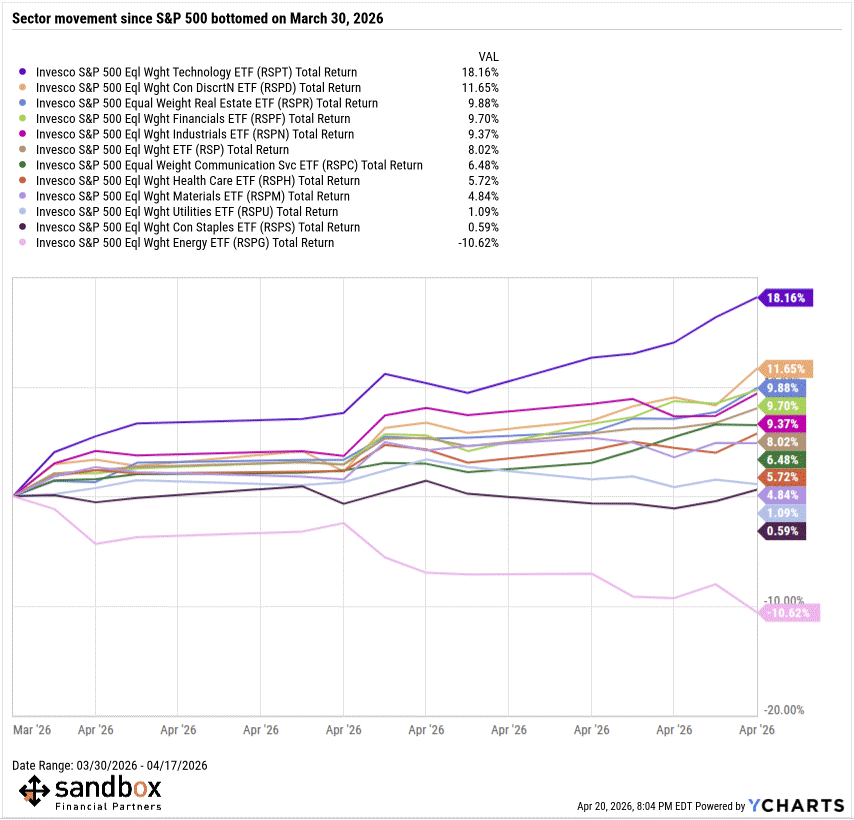

There’s also a powerful technical layer supporting this market right now: positioning and flows.

After significant degrossing throughout Q1, systematic strategies have aggressively added equity exposure, professional money managers have been covering shorts, and rising prices reinforce FOMO.

It’s the classic reflexive loop: higher prices -> more buying -> higher prices.

This dynamic is real, but it has a shelf life.

As positioning fills up, the marginal buyer becomes harder to find. At that point, the burden shifts back to fundamentals – earnings and economic data – to sustain the move.

Of course, leadership in the market still matters.

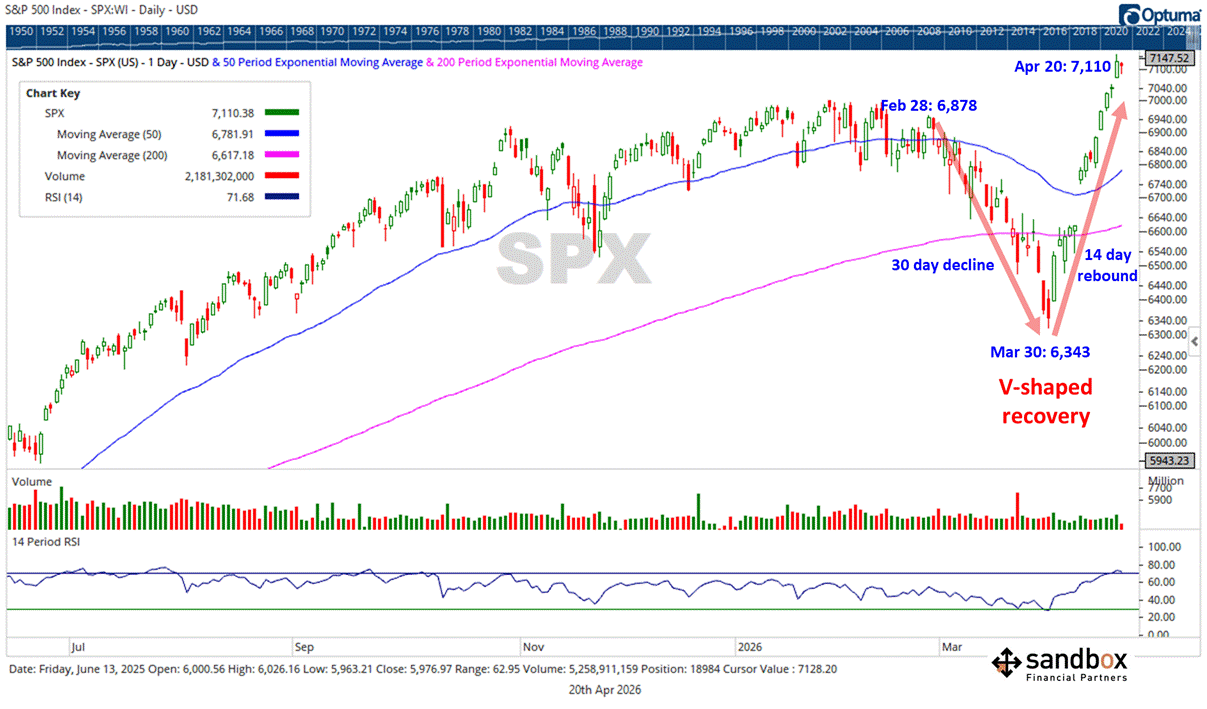

Large-cap tech has snapped back into gear, reasserting its leadership on this v-shaped recovery and once again anchoring the indexes with robust revenue and earnings growth.

That’s an important shift, because since last fall, the market’s core engine had been slowly and steadily losing momentum. Now, it’s back, and that’s a big reason the index-level strength looks so convincing.

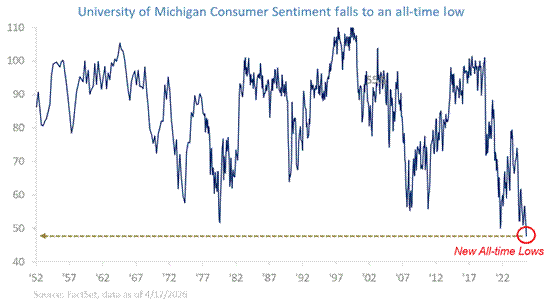

What’s most impressive is this market recovery has taken hold while sentiment remains at its lowest point in modern market history.

Earlier this month, the University of Michigan Consumer Sentiment Index plunged 5.7 points in the preliminary April survey to 47.6, a record low and well below expectations.

This is a data series going back to the 1950s, so it seems a month-long war with Iran has weighed more severely on sentiment than recessions, the dotcom bust, the Global Financial Crisis, the European Debt Crisis, Covid-19, and everything in-between.

While the economy continues to grow and job layoffs remain low, public confidence has completely collapsed.

The disconnect between the reality (data) and the mood (vibes) is so profound that I had to discuss with Nicole Petallides last week on Schwab Network TV.

So, what’s the lesson for investors at home?

Despite the ongoing Iran conflict – and the very real risks that come with it – the broader message hasn’t changed: staying invested and staying the course remains the best option for investors.

Periods of uncertainty feel uncomfortable in real time, but they’re often when opportunities are most attractive for long-term investors.

Geopolitical shocks tend to move prices faster than they move fundamentals. And, more often than not, earnings expectations don’t fall as much as stock prices do during these episodes.

For investors, the implication is straightforward: maintain a long-term perspective, stay balanced, and resist the urge to overreact to short-term noise.

Because in markets like this, patience isn’t just a virtue. It’s an edge.

Sources: Goldman Sachs, Optuma, YCharts, University of Michigan

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures (click here)

Please see our SEC Registered firm brochure (click here)

Please see our SEC Registered Form CRS (click here)