The July jobs report, plus investment returns ≠ investor returns and the week in review

The Sandbox Daily (8.4.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

another mixed employment report

investment returns ≠ investor returns

a brief recap to snapshot the week in markets

It’s summer Friday, folks – hope everyone has a great weekend!

The setting tonight in Annapolis is incredible !!!

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 -0.20% | Dow -0.43% | Nasdaq 100 -0.51% | S&P 500 -0.53%

FIXED INCOME: Barclays Agg Bond +0.82% | High Yield +0.59% | 2yr UST 4.772% | 10yr UST 4.042%

COMMODITIES: Brent Crude +1.05% to $86.03/barrel. Gold +0.43% to $1,977.2/oz.

BITCOIN: -0.79% to $29,035

US DOLLAR INDEX: -0.51% to 102.023

CBOE EQUITY PUT/CALL RATIO: 0.62

VIX: +7.41% to 17.10

“Focusing on the performance or cost of a portfolio relative to something other than a plan is like decorating a house that has no foundation. Making poor decisions – even if at a low cost or even no cost – won’t do anyone any good.”

Josh Brown, A Portfolio is not a Plan

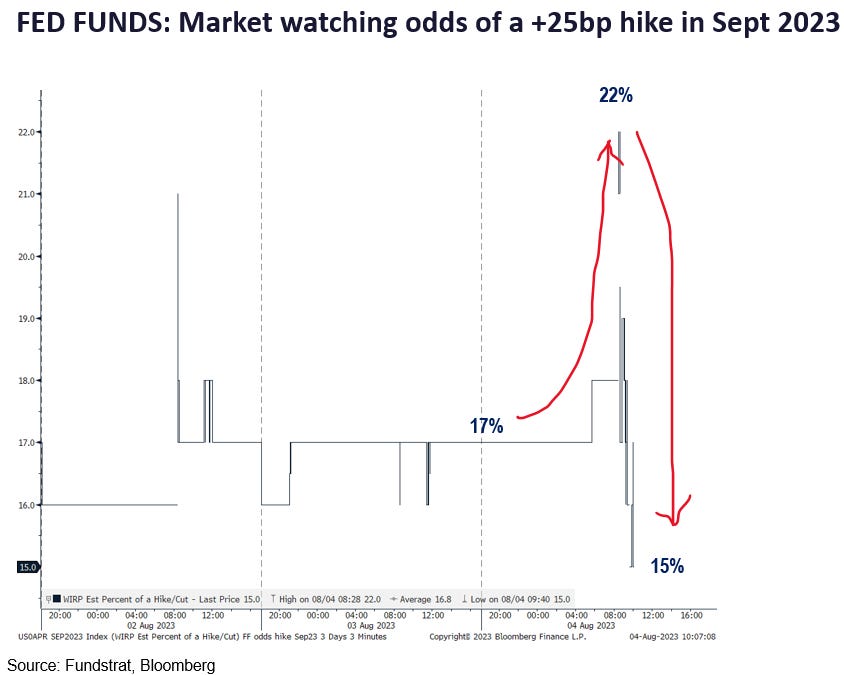

Another mixed employment report

Job growth is slowing, the labor market is tight, and wages are rising.

Non-farm payrolls climbed 187,000 in July, as the report printed below expectations of 200,000 and came in below the forecast for just the 2nd time in 16 months. Additionally, the prior two months were revised down by a total of 49,000; the jobs report now for the preceding 6 months have all been revised lower, a pretty surprising string of consecutive negative revisions. Elsewhere, the unemployment rate dropped to 3.5% from 3.6%.

There were signs of underlying wage strength that should keep the Federal Reserve on watch and data dependent as to whether further hikes are needed this fall. Average hourly earnings rose +0.4% MoM, keeping the YoY change at +4.4% – both above expectations and a key input in services inflation that has the FOMC’s attention.

On balance, these are modest signs of softness at the margin, at a time when job gains are still quite robust on an absolute basis. And from a market’s perspective, a downside “miss” is positive for stocks, as this is more consistent with what the Fed wants to see. In fact, the market’s interpretation of the September rate hike showed that this report doesn’t support a hawkish Fed.

The July jobs report confirms that the ‘tug of war’ between growth and inflation may take longer to play out, which many believe would give the Fed more room to hold at elevated levels while still meeting its dual mandate. Given heightened fiscal spending, rising geopolitical tensions, labor shortages, and the onset of a global energy transition, the transition towards slower growth and lower inflation will take longer and be bumpier this cycle than in the past.

Source: Ned Davis Research, Fundstrat, Bloomberg

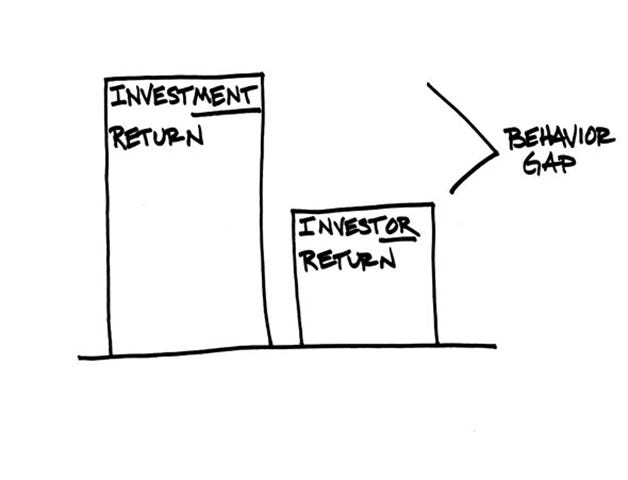

Investment returns ≠ investor returns

The only good investment plan is the plan that you can stick with and execute through adversity. After all, markets are just cycles of booms and busts cluttered with day-to-day headlines and short-term volatility that distract us from achieving our long-term financial goals.

There’s a difference between investment returns and investor returns – and only one of them matters. And the cause of this Behavior Gap can be reduced to a singular driver full of emotional conflict: risk tolerance.

Risk tolerance is an investor's ability to stick with the plan when their hard-earned savings have suffered a drawdown. This is portfolio adversity in the same we suffer adversity in our personal and professional lives. How do you respond after getting knocked down?

Conceptually, one’s risk tolerance seems rather straightforward, however it’s quite challenging to pinpoint in practice, because it is heavily affected by our human emotions which are difficult to simulate.

Here are two very powerful solutions for narrowing the Behavior Gap caused by fear and greed and all the complex emotions in between:

Keep your eye on the prize: develop a formal financial plan and review it frequently.

Focus on the probability of success, not on short-term performance.

Source: Carl Richards

The week in review

Talk of the tape: Market risk remains to the upside, although near-term softness to be expected given stretched technicals, sudden bullish investor sentiment, and a weak seasonal period for markets. Soft-landing expectations are the key driver of the bullish narrative. Disinflation traction cited as another tailwind. Consumer resilience, although showing some signs of fatigue, continues to be a bright spot. Improvement in market breadth following the longstanding scrutiny around 2023’s narrow mega-cap tech leadership flagged as another driver for markets.

Bears remain focused on the higher-for-longer Fed, liquidity headwinds, earnings/margin risk, and lagged effects of policy tightening. Some concerns linger about overbought conditions and stretched valuations. Fedspeak still tilts hawkish.

Markets have shifted their attention to 2nd quarter earnings season and the upcoming CPI/PPI reports due next week.

Stocks: Investors de-risked this week amid uneven economic data, the U.S. government debt downgrade, and mixed earnings reports. In the latest Investors Intelligence survey, the percent of bulls increased from 55.6% to 57.1%, which is the peak last seen during November 2021. Next week, investors will be closely monitoring the Consumer Price Index (CPI) report on Thursday and the Producer Price Index (PPI) report on Friday.

Bonds: The Bloomberg Aggregate Bond Index ended lower for the third straight week. June’s better-than-expected inflation and personal spending reports have traders believing the Federal Reserve is near the end of its campaign of raising interest rates, however the Fed continues to reiterate that it remains data dependent. Bond investors will be watching next week’s July inflation data to see if present deflation trends are still intact. This week’s Fitch downgrade of the U.S. government’s credit rating should not materially impact Treasuries or the U.S. dollar as we remain the safe haven market during periods of market stress.

Commodities: Energy prices ended the week mixed as the major metals (gold, silver, and copper) sold off. With U.S. stockpiles of crude oil and fuel products lower than expectations, reflecting stronger than expected demand, prices for West Texas Intermediate have climbed above $80 a barrel. In addition, as forecasts for a stronger economic recovery prove to be correct, oil demand should see a pickup in the U.S. and globally.

Source: Dwyer Strategy, LPL Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.