The market's strong start to 2024, plus S&P 500 valuations, corporate net interest expense, and rate cuts

The Sandbox Daily (2.26.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

strength begets strength

2024 valuations in perspective

potential headwind to corporate profit margins

one simple chart

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 +0.61% | Nasdaq 100 -0.02% | Dow -0.16% | S&P 500 -0.38%

FIXED INCOME: Barclays Agg Bond -0.22% | High Yield -0.32% | 2yr UST 4.727% | 10yr UST 4.281%

COMMODITIES: Brent Crude +1.12% to $82.53/barrel. Gold -0.40% to $2,041.3/oz.

BITCOIN: +5.83% to $54,739

US DOLLAR INDEX: -0.15% to 103.782

CBOE EQUITY PUT/CALL RATIO: 0.66

VIX: -0.07% to 13.74

Quote of the day

“You miss 100% of the shots you don’t take.”

- Wayne Gretzky

Strength begets strength

In honor of Ryan Detrick’s amazing guest spot on the recent episode of The Compound and Friends podcast, what better way to start the final week of February with some stats !

The S&P 500 was up +1.59% in January and is currently up another +4.62% in February.

So, what happens after the market starts the year strong with both a positive January and February?

More strength, at least according to history.

Higher 26 of 28 instances for the remaining 10 months of the year (median gain = +11.3%) and higher 27 of 28 times for the next 12 months (median gain = +11.6%).

Source: Ryan Detrick, CMT (Carson Group)

2024 valuations in perspective

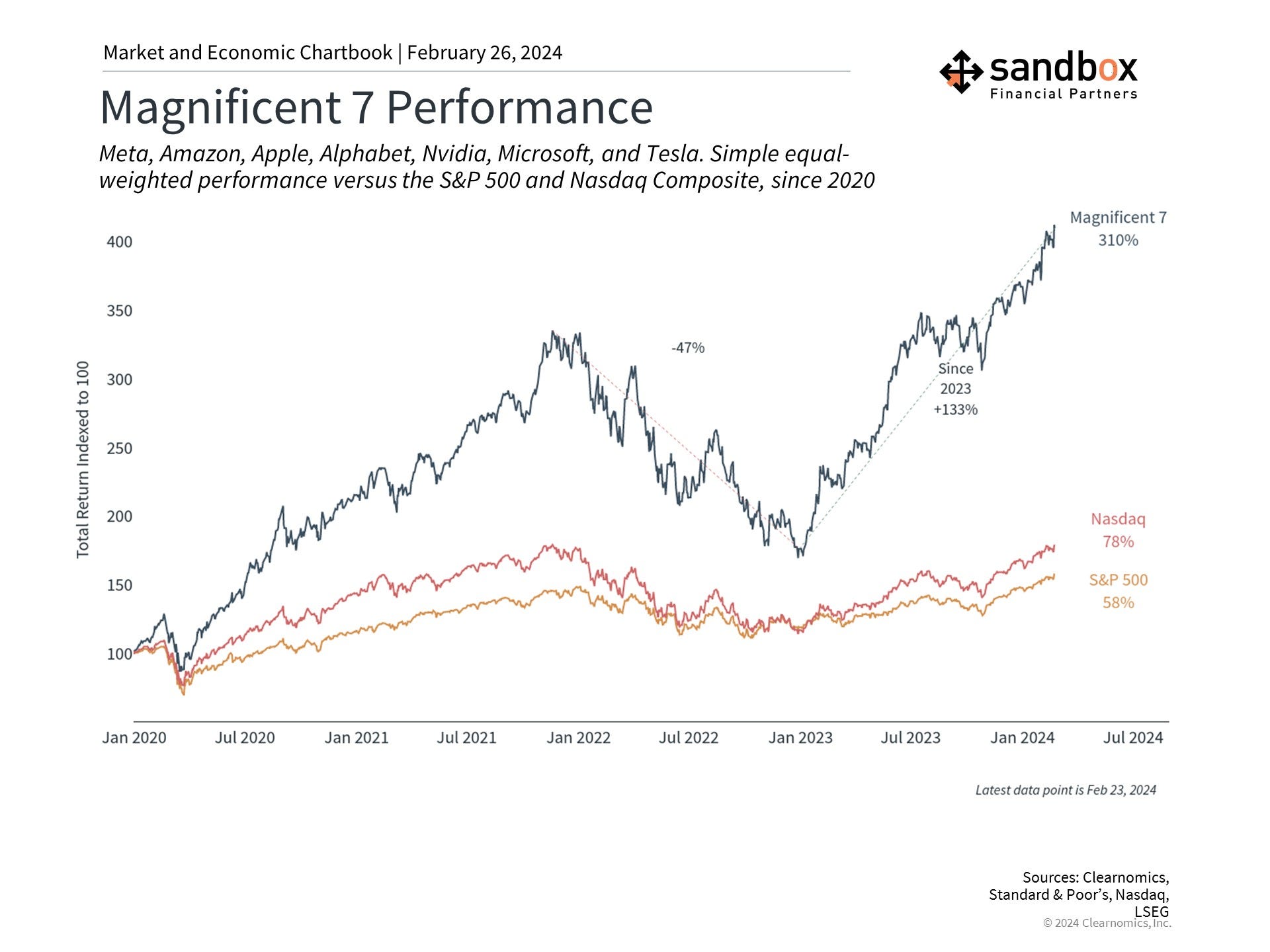

The stock market continues to reach new heights, driven by a stronger-than-expected economy and the largest technology stocks – in particular, Nvidia, the maker of graphics chips used in artificial intelligence applications that helped to push markets higher after it beat Wall Street earnings expectations last week.

This has added to the gains made by the group known as the Magnificent 7 which consists of fast-growing technology companies, many of which have market capitalizations of a trillion dollars or more. In this environment, some investors may be nervous that the market has risen too far, too fast. At the same time, other investors may have a growing fear that they are missing out.

So, how can long-term investors stay level-headed when markets have climbed so quickly?

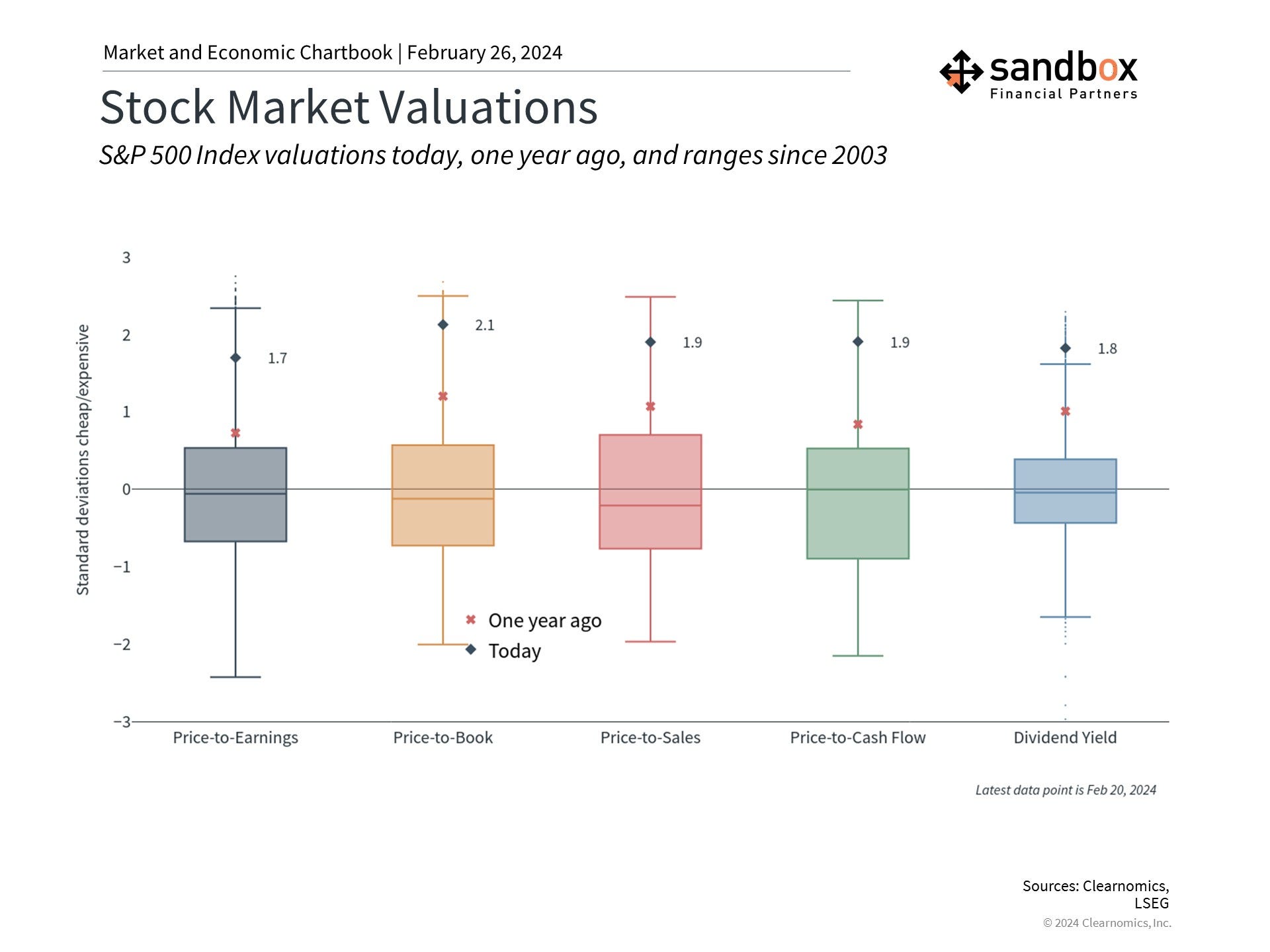

Perhaps the most important consequence of the bull market rally of the past year is that valuation levels are no longer cheap. The S&P 500 has gained roughly 28% during this time, while the Nasdaq and Dow Jones Industrial Average have risen 40% and 19%, respectively. As a result, the price-to-earnings (P/E) ratio for the S&P 500 is now 20.4x, meaning that investors are willing to pay $20.40 for every dollar of expected earnings. While this is below both its peak before the 2022 bear market as well as the historic high during the dot-com bubble, it is still well above its long-run average of 16.5x.

Why are valuations important to long-term investors? Simply put, valuations are among the best tools that investors have to gauge the attractiveness of the stock market over years and decades. Unlike stock prices on their own, valuations don't just tell you how much something costs, but what you get for your money. Valuations are correlated with long-term portfolio returns for this reason – buying when the market is cheap can improve the chances of success and buying when the market is relatively expensive can be a headwind on future returns.

However, valuations are neither market timing tools nor do they explain all nuances of the market’s movements. Instead, they are simply guideposts that can help investors determine appropriate asset allocations based on their financial goals.

As shown below, most common valuation measures are now well above their long run averages when looking at price-to-book (P/B), price-to-sales (P/S), dividend yield, etc. – as well as valuations versus just one year ago.

This is partly because the underlying fundamentals are still catching up with the market rally. As sales grow, earnings improve, and interest rates stabilize, valuations could begin to improve as well. Thus, higher valuations are not a reason to avoid stocks but are instead a reminder to focus on diversifying both within the stock market as well as across asset classes.

Source: Clearnomics

One potential headwind to corporate profit margins

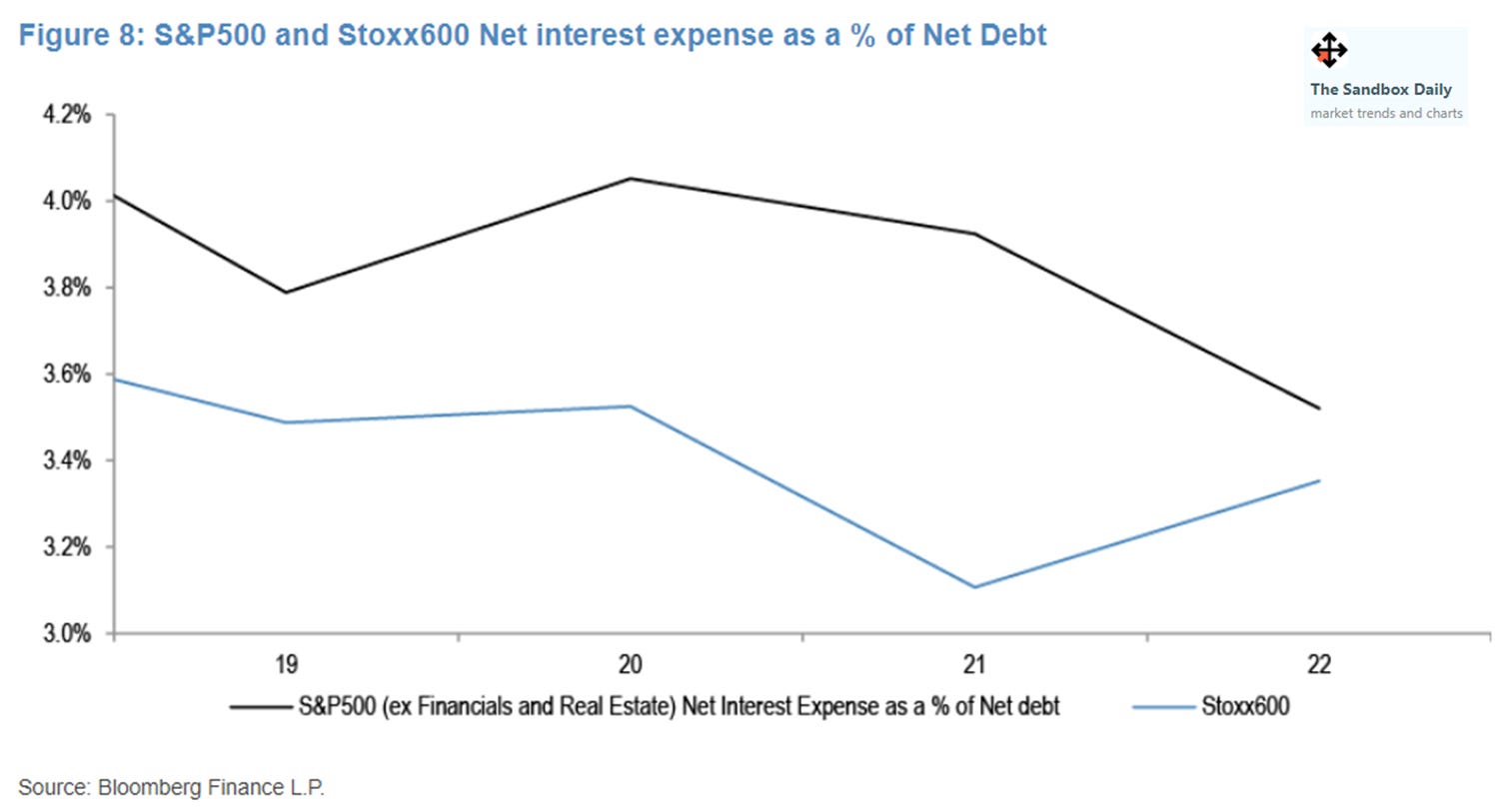

Bulls are to a good extent basing their constructive market call on the premise that corporate profits are set to accelerate in 2024 and 2025. However, one potential headwind to profit margins and earnings is net interest expense.

Many companies benefitted from the unique feature of this cycle: as interest rates increased, their net interest expense came down. That can be explained by corporates locking in low cost of financing through extending the maturity dates of their debt, while at the same time seeing a much-improved return on their cash balances. Of course, this will normalize as time passes when companies will have to roll their debt forward into higher costs of capital.

Almost 40% of S&P 500 index constituents have watched their net interest expense go down. See the chart below.

The net interest component was strongly accretive to a company’s bottom line over the past few years, with net interest expense collapsing, but this is likely as good as it gets.

In fact – almost defying logic – the effective interest rate (net interest expense / net debt) of the S&P 500 index has dropped versus the pre-pandemic levels despite rising interest rates.

Source: J.P. Morgan Markets

One simple chart

The FOMC’s most recent Summary of Economic Projections from mid-December 2023 showed the Federal Reserve was indicating 3 potential interest rate cuts for all of 2024.

By mid-January, the overzealous bond market had priced in nearly 7 rate cuts.

Now? We’re back to 3 cuts – just like the Fed told us.

As Ferris Bueller might say, “Life moves pretty fast.”

Source: Bloomberg

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.