The S&P 500 led by Utilities ??!?, plus U.S. homeowners, debt maturity schedule, and easing financial conditions

The Sandbox Daily (5.9.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

strength in Utilities

U.S. homeowners’ equity at record highs

debt schedule for the S&P 1500

financial conditions impulse remains positive

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 +0.90% | Dow +0.85% | S&P 500 +0.51% | Nasdaq 100 +0.16%

FIXED INCOME: Barclays Agg Bond +0.19% | High Yield +0.03% | 2yr UST 4.818% | 10yr UST 4.459%

COMMODITIES: Brent Crude +0.69% to $84.16/barrel. Gold +1.29% to $2,352.3/oz.

BITCOIN: +1.53% to $62,574

US DOLLAR INDEX: -0.31% to 105.223

CBOE EQUITY PUT/CALL RATIO: 0.69

VIX: -2.38% to 12.69

Quote of the day

“The most important adage regarding leverage reminds us to ‘never forget the six-foot-tall person who drowned crossing the stream that was five feet deep on average.’”

- Howard Marks, Oaktree in The Impact of Debt

Strength in utilities

The S&P 500 is roughly 1% away from new all-time highs and the (breadth) leader in this market is… Utilities ??!?

The Utilities sector has performed better since interest rates peaked last October. While the sector has been a slight underperformer in 2024, it has been gaining momentum as of late. Utilities are up +16.8% over the last three months, best among all sectors.

Strength within Utilities has been broad based. The sector currently has the highest percentage of issues trading above both their 50- and 200-day moving averages.

2023 was a tough year for Utilities. The combination of rapidly rising interest rates and stock prices meant that the sector’s negative correlation with bond yields and low beta were both drags on sector performance. While the S&P 500 gained 24.2% last year, Utilities fell 10.2%, trailing the index by its 2nd-widest margin in a calendar year since 1972.

It’s not all rose-colored lenses, though.

Risks for the sector include rising interest rates and elevated debt burdens.

The chart below shows the dividend yield for the Dow Jones Utilities Average is less than the yield on the 10-year Treasury, and the spread is near the widest since 2008. The historical data suggests that if rising yields make the sector’s divided increasingly less attractive, more weakness from the sector could be expected.

Source: Ned Davis Research

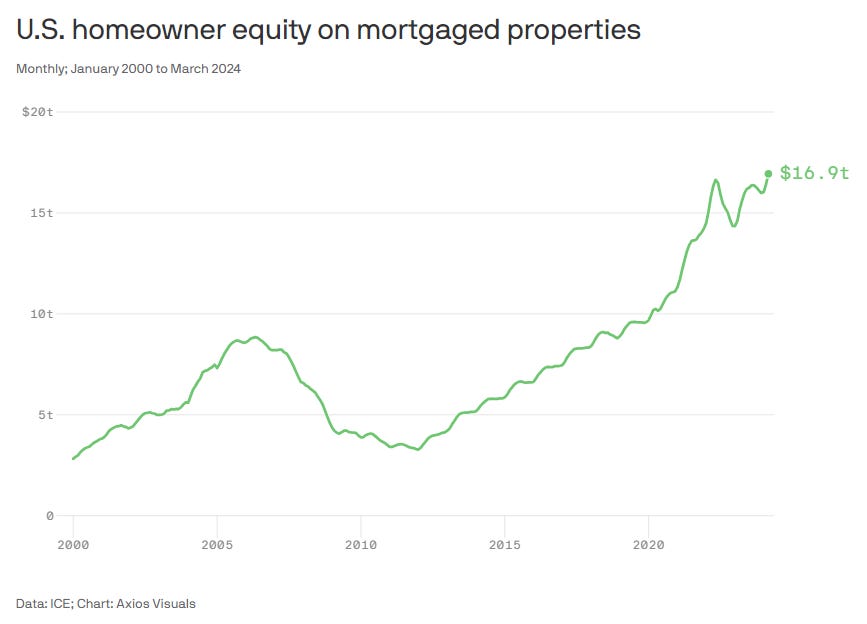

U.S. homeowners’ equity at record highs

Homeowners with mortgages hold just under $17 trillion in equity – a record high – per a report out this week from Intercontinental Exchange (ICE).

U.S. homeowners represent 65.6% of the population, so these paper wealth gains are broad-based.

Source: Axios, St. Louis Fed

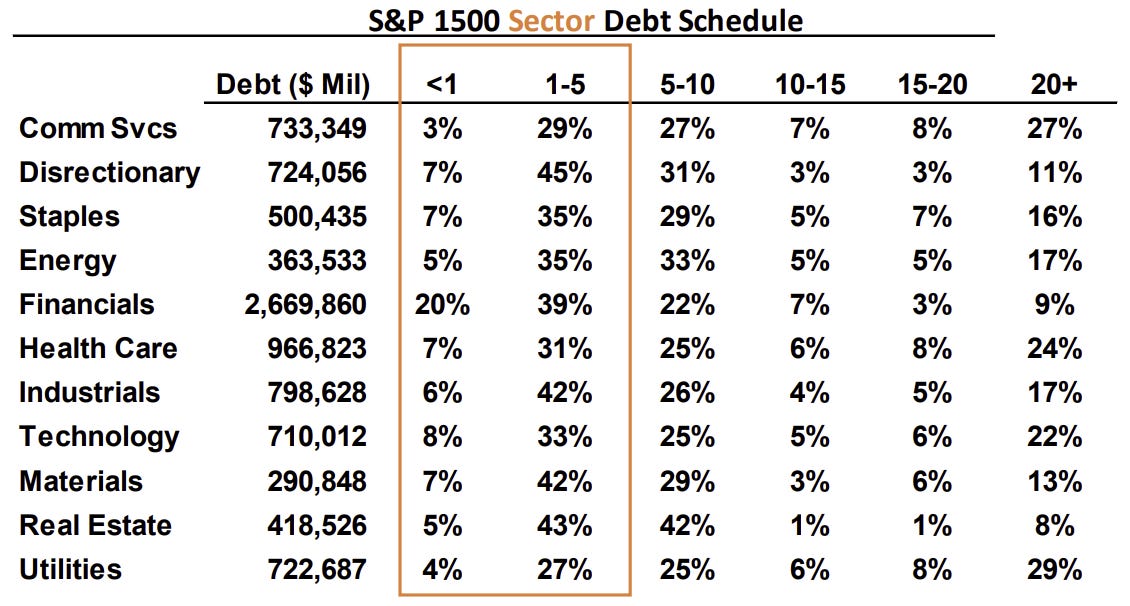

Debt schedule for the S&P 1500

Market rates remain at elevated levels amidst uncertainty on the timing and pace of the upcoming Fed easing cycle. At this point, the level of interest rates is the common thread amongst top investor concerns.

The chart below identifies the debt maturity wall for companies across the S&P 1500 – a composite of the S&P 500 (large-caps), S&P 400 (mid-caps), and S&P 600 (small-caps) – which covers 90% of the market capitalization of U.S. stocks, so it represents a broad swath of the domestic market’s exposure to the path of interest rates ahead.

Nearly a third of all debt is coming due in every sector within the next five years.

The longer rates remain elevated, the bigger the impact that the debt refinance wall will have on earnings and growth.

Source: Piper Sandler

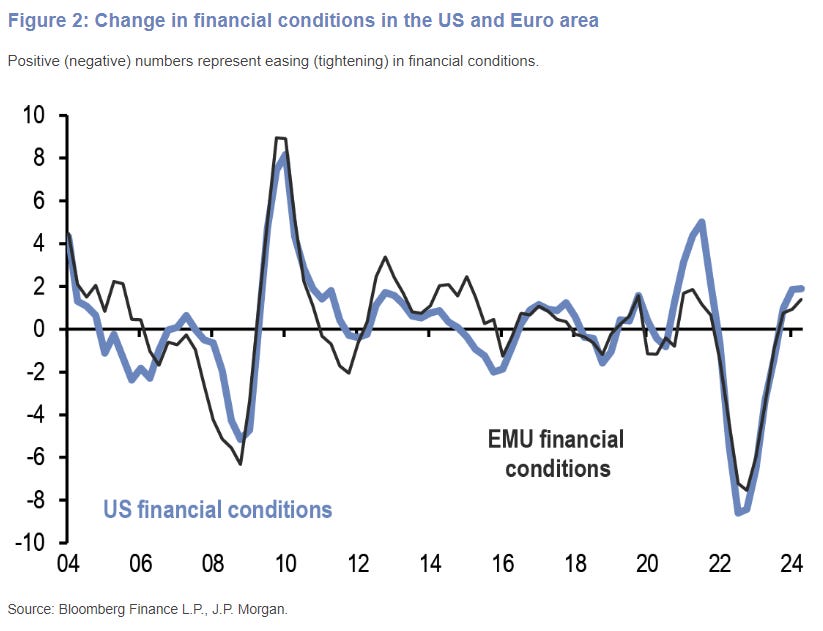

Financial conditions impulse remains positive

Much has been made about financial conditions steadily improving from their peak tightening in 2H22 to a net loosening by 4Q23.

Moreover, this has been a broad-based improvement as the effect of past yield rises has faded, equity returns turned from a headwind to a tailwind and lending surveys have eased back significantly from their previous peaks.

While easing financial conditions covers many inputs, one market in which this has manifested itself is the credit markets.

A major source of credit creation in 2024 is through net issuance of debt securities. The chart below shows the monthly net issuance of U.S. Investment Grade bonds for 2024 YTD, as well as for 2023 and the average for the previous 5 years.

The significant strength of net issuance in January and February saw 1Q24 net issuance reach around $310bn, the 2nd strongest quarter since 2000 after 2Q20, though there appears to have been some front-loading of issuance as the pattern for the 1st 4 months is surprisingly similar to 2023 with a drop-off in the pace in March and April.

Bottom line, the financial conditions impulse remains positive, posing some upside fuel for growth and inflation.

Source: J.P. Morgan Markets

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.