The Sandbox Daily (10.3.2022)

Market performance, SPX P/E multiple, ISM manufacturing, BNPL, information technology

Welcome, Sandbox friends.

Today’s Daily discusses the market performance following the end of the third quarter, the P/E multiple reset, ISM manufacturing activity weakens, Buy Now Pay Later (BNPL) attracting regulatory attention, and a closer look at the Information Technology sector.

Let’s dig in.

Markets in review

EQUITIES: Dow +2.66% | Russell 2000 +2.65% | S&P 500 +2.59% | Nasdaq 100 +2.36%

FIXED INCOME: Barclays Agg Bond +0.81% | High Yield +1.31% | 2yr UST 4.115% | 10yr UST 3.641%

COMMODITIES: Brent Crude +4.08% to $88.61/barrel. Gold +2.14% to $1,707.8/oz.

BITCOIN: +1.79% to $19,591

US DOLLAR INDEX: -0.40% to 111.672

CBOE EQUITY PUT/CALL RATIO: 0.77

VIX: -4.81% to 30.10

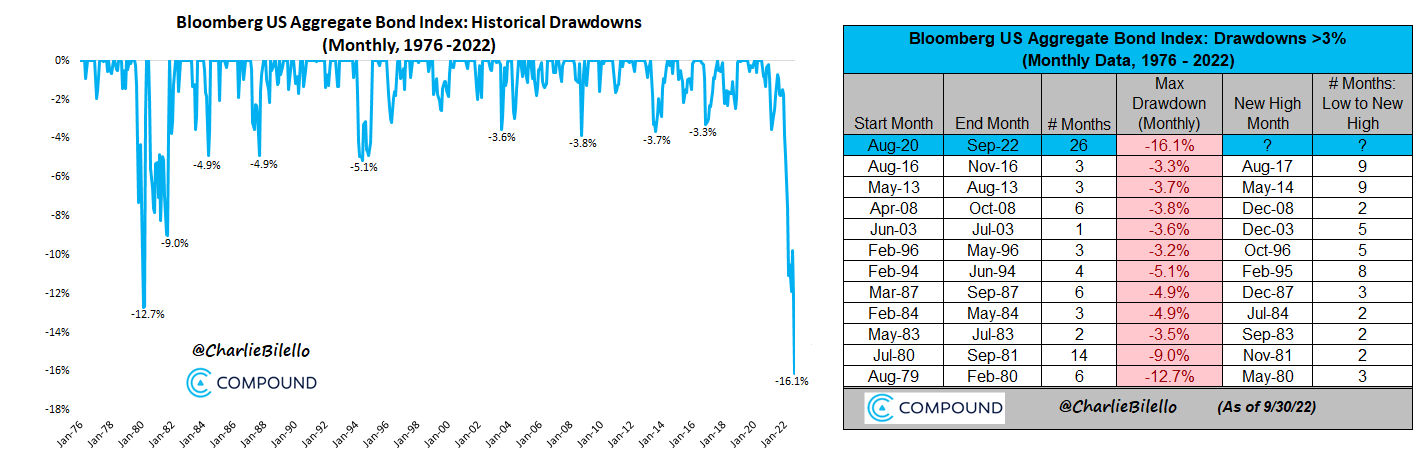

3rd quarter in the books

As we reflect on market performance with the closing of both the month and quarter, where does 2022 rank for the standard 60-40 asset allocation model? Well, the worst on record since 1931…

At 8 months, the current bear market in the S&P 500 is now the longest we’ve experienced since the 2007-2009 bear market. The average length of a bear market since 1929 is 14 months, with a great deal of macro catalysts and variation around each bear – however one of the most important considerations today will depend on whether we are in a recession (average 16 months) or not (average 12 months).

Meanwhile, bonds are having its worst drawdown (-16.1%) since the inception of the widely-regarded index, the Bloomberg US Aggregate Bond, which dates back to 1976. Stocks and bonds have not sold off together to this degree, only inflicting greater pain on the average investor.

Investing is hard. There are no certainties in markets. 2022 has been especially difficult: war, inflation, currency crises, energy shocks, hawkish central banks, inflamed geopolitical tensions, and a global economy on the brink of recession, to name a few. And then there’s the human element to consider – emotions and biases. BUT, the market has always had to confront these issues, climbing the wall of worry from one market cycle to the next. One day (hopefully sooner than later) this too shall pass, and the forward-looking returns will be more attractive on the heels of this uncomfortable reset we’ve all experienced together in 2022.

Source: Charlie Bilello

P/E multiple reset

Equity markets have seen their multiples compress meaningfully in 2022, as the sky high prices of 2021 have come crashing back to earth as higher interest rates are incorporated into asset valuations. Entering 2022, the S&P 500 had a forward P/E of multiple of 21.18x – now that same multiple is 15.15x, which is below the 25-year historical average of 16.84x and approaching 1 standard deviation below the average. When deconstructing the -24.8% percent change in the S&P 500 index, multiple growth is down -29.9%, while earnings are up +5.1%.

Source: JPMorgan Guide to the Markets

ISM manufacturing activity weakens

The ISM Manufacturing Purchasing Managers Index (PMI) fell 1.9 points in September to 50.9, its lowest level since May 2020, and below the consensus of 52.0. It is consistent with continued but notably weaker growth in both manufacturing activity and the broader economy. The ISM estimates that this level of the PMI corresponds to just +0.8% annualized growth in real GDP. Only half of the 18 ISM industries expanded last month, the smallest share also since May 2020, and consistent with slowing growth momentum.

The latest PMI decline was led by a 5.5 point drop in the employment index to 48.7, in contraction territory in four of the past five months. Excluding the pandemic, this was its biggest monthly drop since November 2012. The report noted that companies have resorted to hiring freezes and attrition to control labor costs, but are not yet planning large-scale layoffs. It likely signals more confidence in future demand conditions, despite a contraction in new orders last month. Indeed, new orders sank 4.2 points to 47.1, the lowest level since May 2020.

Source: Ned Davis Research

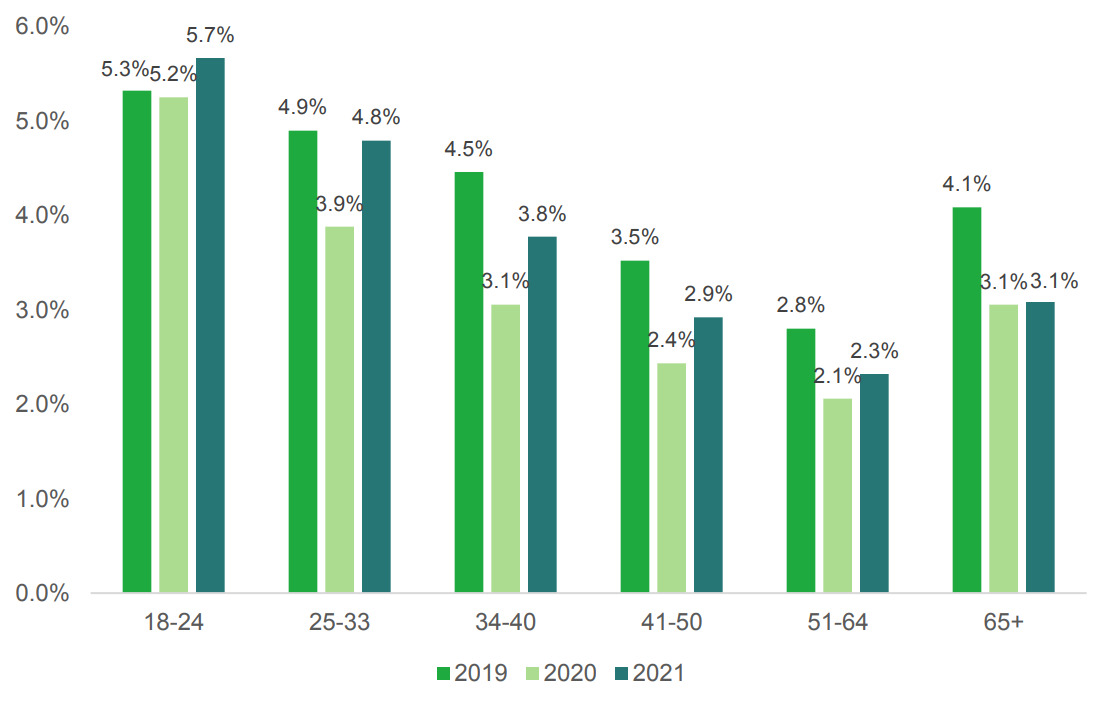

BNPL attracting regulatory attention

The Consumer Financial Protection Bureau (CFPB) recently released a study on "Buy Now, Pay Later" (BNPL) lenders highlighting uneven protections for borrowers, and plans to regulate the industry in a manner similar to credit card providers.

BNPL became increasingly popular during the pandemic, as households could order essentials and consumer discretionary items from home, while traditional payment methods were less flexible and available due to lockdowns and other pandemic restrictions. While early stages of BNPL focused on purchases of durable goods and more expensive items, consumers are increasingly using it to purchase everyday necessities. In 2021, the five major lenders (Affirm, Afterpay, Klarna, PayPal, and Zip) originated 180 million BNPL loans totaling $24.2 billion, for an average loan size of $135. Both loan and dollar originations are growing at over 200% since 2019.

According to the CFPB, overreliance on BNPL has led many borrowers – particularly younger and less creditworthy individuals – to take on more debt. The option of taking out numerous loans simultaneously, often with no interest payments, has left many consumers with high levels of debt that accumulate with each transaction. For this reason, regulators have considered subjecting the industry to the same degree of oversight as credit card companies. Here is the share of unique BNPL borrowers by age cohort with 1+ default(s) or charge-offs.

Source: Consumer Financial Protection Bureau

Information Technology undone

The S&P 500 re-entered bear market territory during the 3rd quarter, with the index being dragged down by its largest component, Information Technology, which made up 29% of the index and is the 2nd worst performing sector year-to-date at -31%. This follows the sector returning over +40% in calendar years 2019 and 2020, then another +30% in 2021.

Each group within the sector is suffering from rising rates, as many of these companies are characterized as growth stocks in which much of their value is derived from unlocking value and cash flows years down the road.

Here are the 10 companies within the sector, ranked across a selected variety of growth metrics.

Source: Goldman Sachs Investment Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.