The Sandbox Daily (10.6.2022)

U.S. housing market, recapturing the S&P 500 high water mark, and credit spreads

Welcome, Sandbox friends.

Today’s Daily discusses the affordability crisis brewing inside the U.S. housing market, what needs to happen for the S&P 500 to recapture its high water mark from earlier this year, and credit spreads show widening but not yet major market risk.

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 -0.58% | Nasdaq 100 -0.76% | S&P 500 -1.02% | Dow -1.15%

FIXED INCOME: Barclays Agg Bond -0.39% | High Yield -0.30% | 2yr UST 4.256% | 10yr UST 3.828%

COMMODITIES: Brent Crude +1.33% to $94.92/barrel. Gold -0.29% to $1,720.1/oz.

BITCOIN: -0.54% to $19,908

US DOLLAR INDEX: +1.04% to 112.228

CBOE EQUITY PUT/CALL RATIO: 0.72

VIX: +6.90% to 30.52

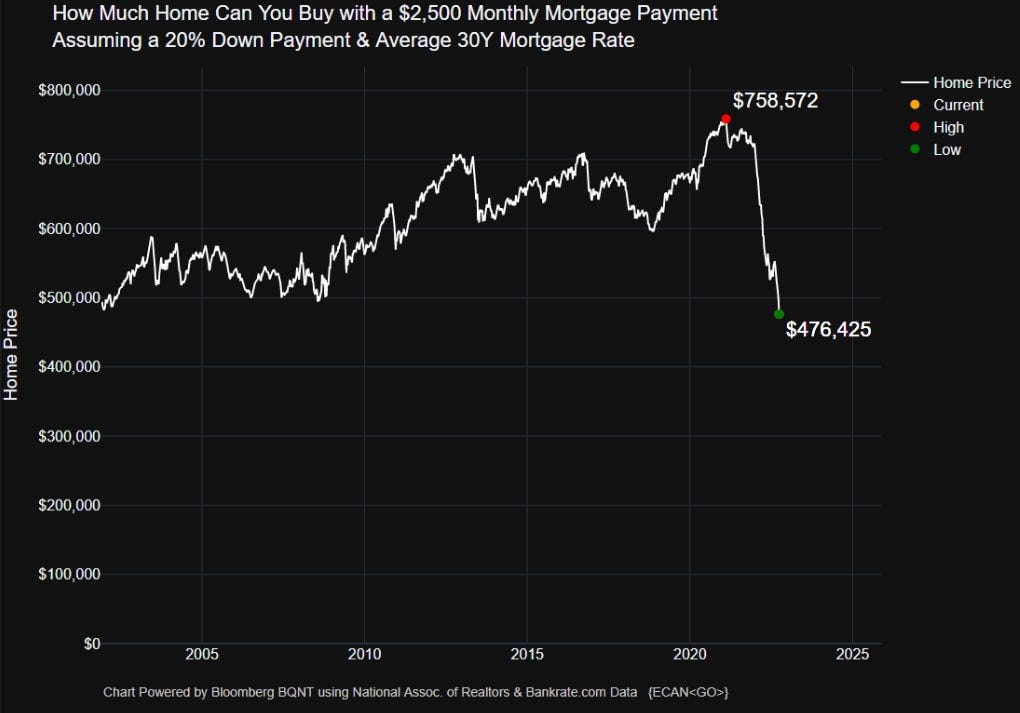

The housing market has an affordability problem

Housing affordability is becoming a real issue.

In 2021, a standard 30-year fixed rate mortgage in the United States could be locked in somewhere around 3%. Fast forward to 2022, that number is closer to 7%. What does that mean in terms of financing a home? Well, if one wanted to spend $2,500 a month on their mortgage payment, you could have bought a $758,572 house in early 2021. For that same monthly payment, you can now only buy a home for $476,425 in 2022. This simple exercise shows just how much interest rates can impact the financing of a home purchase.

And this hypothetical doesn’t even consider the appreciation in home prices that we all hear about from family and friends or see on the news. The Case-Shiller National Index shows the average home price has increased +15.8% year-over-year, as of July.

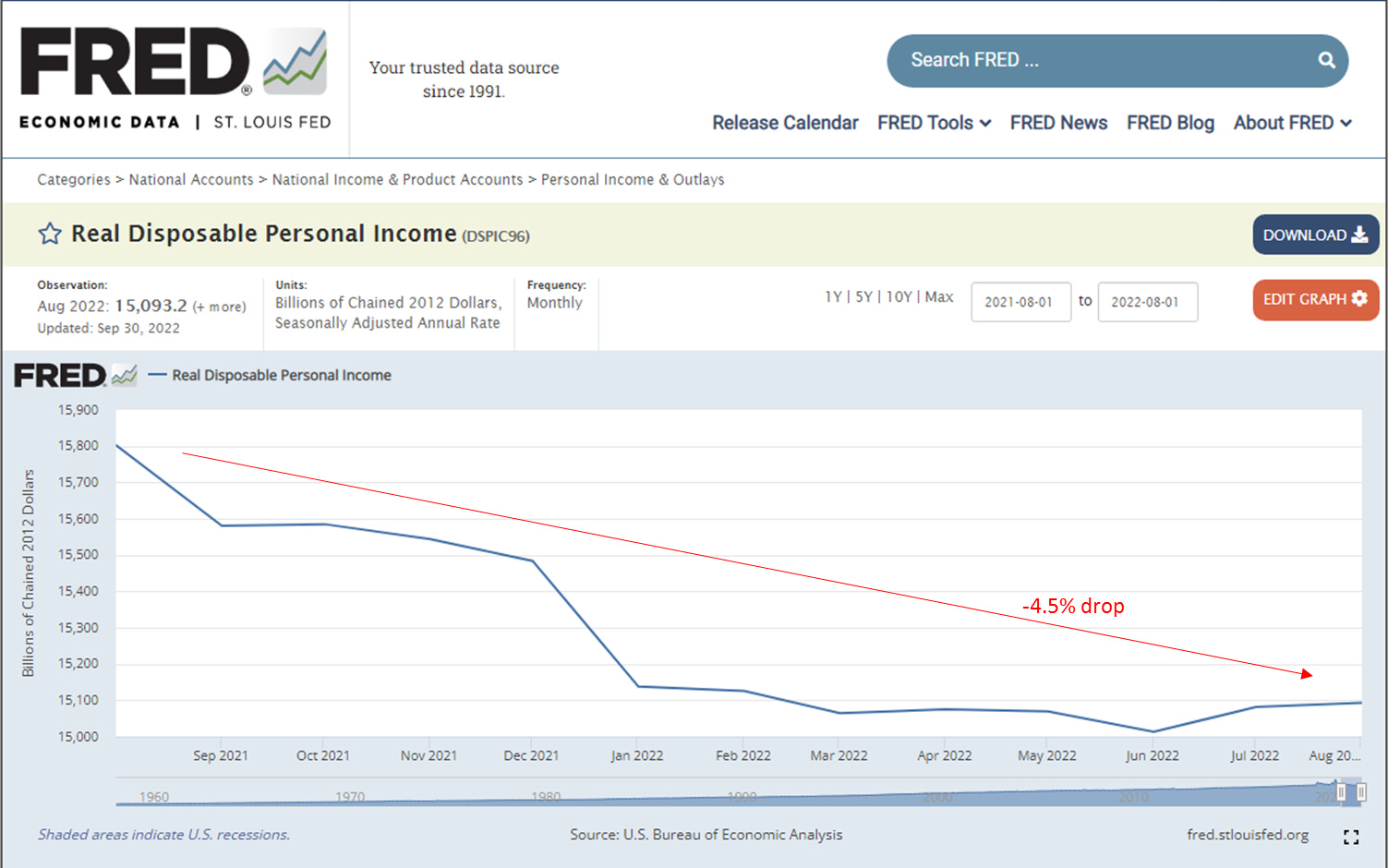

Nor does this exercise consider that the real disposable incomes are down -4.5% in the last year (hat tip inflation).

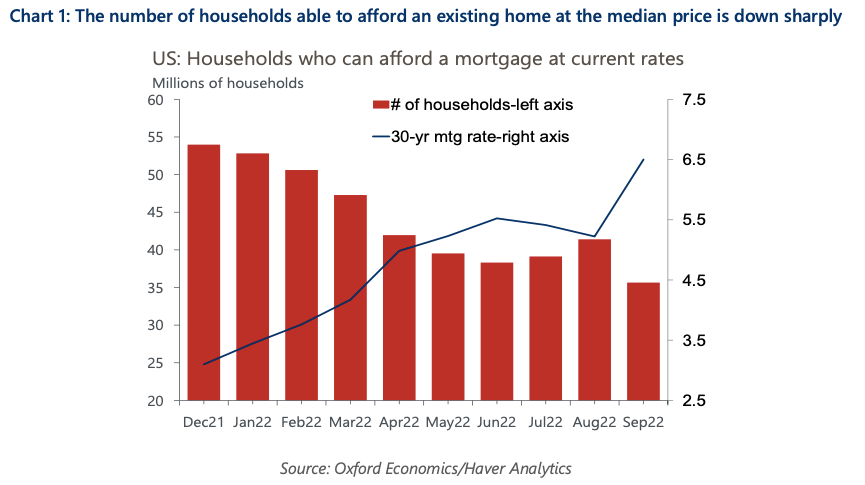

By some estimates, the housing affordability issue ripples out to effect millions of households. Oxford Economics had this to say: “with 30-year mortgage rates approaching 7.0%, we estimate that 18mm fewer households now qualify for a mortgage to buy a median-priced existing home compared to the end of 2021.” These households will need to adjust their expectations down, consider a smaller home, look at a different location, etc. Or one must wait, hoping prices drop and/or rates come in.

Higher interest rates? Check. More expensive homes? Yup. Income after inflation down? Sadly yes. The math no longer works for millions of American homebuyers.

Per a note from David Doyle, Macquarie’s head of economics, what we’re seeing right now is “the most severe deterioration in affordability on record.”

One silver lining of the 2022 rate shock is that because most American homeowners are on fixed-rate mortgages and likely refinanced in the last few years, the impact isn’t really felt by them. But for prospective homebuyers, the reset in rates is having a material effect on housing demand and mortgage applications.

Source: Bloomberg, Pragmatic Capitalism, Calculated Risk, FRED Economic Data of St. Louis Fed, Oxford Economics

Recapturing the S&P 500 high water mark

The markets have come down quite a bit this year. It has been an unpleasant ride for most investors. The S&P 500 index is down -21.44% year-to-date. Not terrible, but definitely not great.

So what needs to happen for the equity market to recapture their all-time highs from January 3, 2022? JP Morgan shows we will need to gain +35.7% over the next year to be made whole. Over 3 years, the S&P 500 would need to annualize +12.1%. Over 5 years, +7.9% compounded.

Investing is not easy.

Source: JP Morgan Guide to the Markets

Credit spreads are not indicating near-term major market risk

The pain for bond investors cannot be understated as the Federal Reserve and other central banks around the world hike their target interest rates in efforts to tighten financial conditions and stomp out inflation. This angst has sent the majority of sectors’ spreads much higher this year, some roughly double the spread from just last year. But even as the bond losses mount in 2022 and spreads likely hover at/near their peak for the current cycle, there’s still plenty of room for these spreads to widen out further – we are nowhere close to 2008 levels, if we are to gauge and measure market risk using the Global Financial Crisis analog.

Credit risk, for now, is perceived to be elevated but within the historical “norm” – given that many corporate and high yield borrowers refinanced rates over the last few years at historically low levels, consumer aggregate demand remains strong, the flow and access to credit shows vigilance, and the labor market continues to show strength.

Source: Eaton Vance

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.