The Sandbox Daily (7.26.2022)

Welcome, Sandbox friends.

Today’s Daily discusses the IMF’s lowered 2022 global growth forecast, crypto’s bounce off the June lows, bottlenecks in the shipping industry, the decline in new homes sales, ARKK stuck under overhead supply, Walmart’s cut in profit guidance, and the slowing issuance in junk bond debt.

Howard Marks, the co-chairman of Oaktree Capital Management, released his latest memo this morning, I Beg to Differ. Howard argues that investors seeking superior performance must have the courage to depart from the pack, even though doing so means accepting the risk of being wrong. Thinking differently and better than others is key to outperformance, he explains, because in investing, it’s not enough to be right. You have to be more right than most. This means being able to tell when the investment crowd is focused on all the wrong things.

Let’s dig in.

EQUITIES: Russell 2000 -0.69% | Dow -0.71% | S&P 500 -1.15% | Nasdaq 100 -1.96%

FIXED INCOME: Barclays Agg Bond -0.01% | High Yield -0.70% | 2yr UST 3.071% | 10yr UST 2.814%

COMMODITIES: Crude Oil +0.35% to $104.90/barrel. Gold -0.03% to $1,735.2/ounce.

BITCOIN: +1.11% to $21,208

VIX: +5.69% to 24.69

CBOE EQUITY PUT/CALL RATIO: 0.76

US DOLLAR INDEX: +0.61% to 107.026

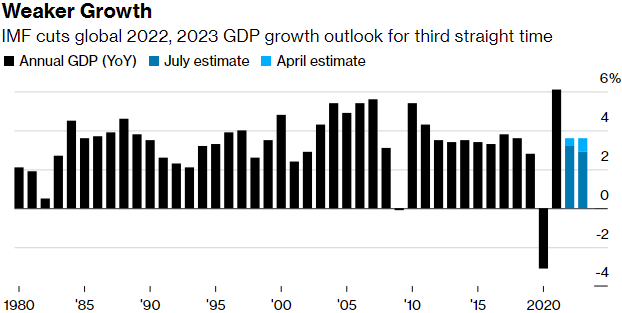

IMF sees “gloomy” outlook for global growth

The International Monetary Fund (IMF) slashed its global forecast again, citing a “gloomy” outlook with lower growth rates and higher inflation rates over a sustained period of time. The new IMF forecast shows the global economy growing 3.2% this year – down from the 3.6% it forecast in April (which itself was a downgrade from 4.4%).

The Washington-based institute said the revised outlook indicated that the downside risks outlined in its earlier report were now materializing. The IMF cited 3 main drivers of their lower growth guidance: 1) negative spillover from Russia’s invasion of Ukraine weighing on energy and grain markets, 2) a more pronounced economic slowing in China in large part from their zero-Covid mandate, and 3) tighter financial conditions in the United States. Last year global growth was a breakneck pace of 6.1% on the heels of the great reopening of the world’s economy.

Source: IMF World Economic Outlook update

Bounces from the low

While digital assets often face the brunt of macro selling pressure, the segment often bounces stronger than traditional equities after the lows are reached. Most risk-assets bottomed on June 16th (for many US equity indices) or June 18th (for many digital assets). This bottom in risk assets has been supported by several factors such as lower inflation expectations and better sentiment in relation to Fed rate hikes and the magnitude of financial tightening. Even with the news of many funds and brokerages unwinding leverage and risky bets, bitcoin and ether have still outperformed equities since their lows.

Source: Eaglebrook Advisors

Bottlenecks in the Shipping Industry

In the past seven years, the number of active shipyards has declined by 45%, and some of the remaining shipyards have also diminished in size, leading to significant port congestion, delays, and increases in shipping costs. At the same time, merchant fleet tonnage has been consistently increasing, as has the size of the vessels (making it more difficult for them to navigate existing channels), exacerbating the issue.

Source: Horizon Kinetics

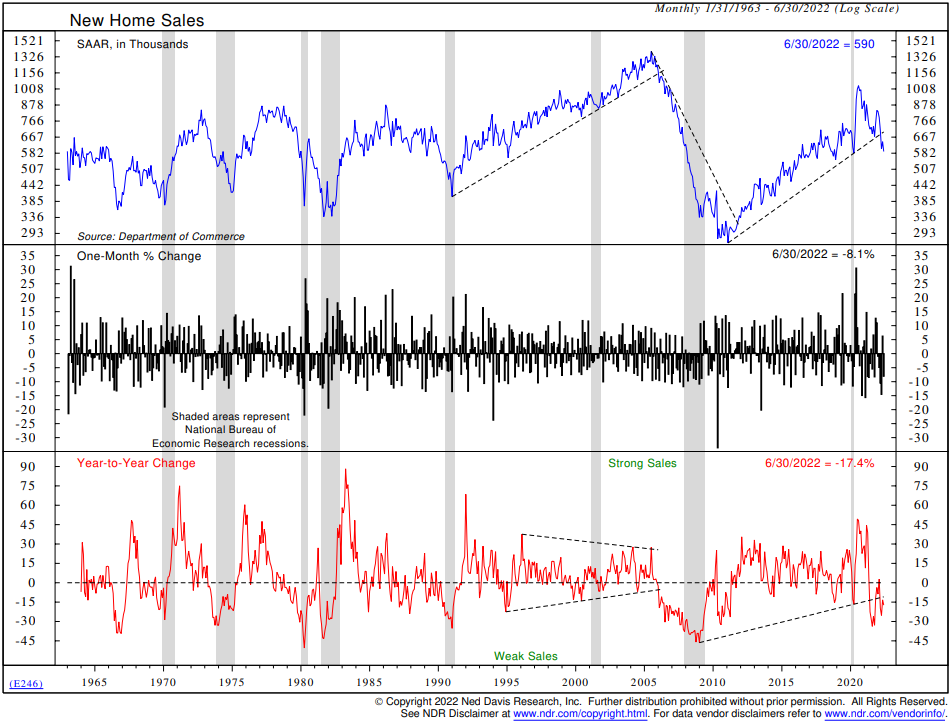

New home sales decline more than expected

New home sales fell 8.1% in June to a 590,000 unit annual rate, the lowest level in two years, and below the consensus of a 664,000 unit rate. It was the fifth decline in the past six months, as housing demand has softened this year amid rising mortgage rates. On a y/y basis, new home sales were off 17.4%.

Source: Ned Davis Research

ARKK still under overhead supply

This chart shows the performance of Cathie Wood’s ARK Innovation ETF (ARKK) over the last six months, where top holdings $TSLA, $ZM, $ROKU, $TDOC, and $CRSP have been correcting going back to 1H21. $ARKK is rolling over again after bouncing nearly 34% off its June lows – back below its recent breakout level around $45. This fund represents the market’s broader appetite for risk-on trades, and until we see a meaningful breakout from this one-and-a-half year downdraft, the bears remain in control.

Source: StockCharts.com

Walmart warning sends stock price plunging

The world’s largest retailer slashed its second quarter and full-year profit outlooks after Monday’s market close, owing to rampant inflation and a consumer retrenchment.

As recently as February, Walmart expecting earnings for the year to rise by 5-6%; comparable figures now are for earnings to decline 10-12%. Walmart CEO Doug McMillon said, “The increasing levels of food and fuel inflation are affecting how customers spend, and while we’ve made good progress clearing hardline categories, apparel in Walmart U.S. is requiring more markdown dollars.” Why does this matter? Walmart is a bellwether of American consumption — a key driver of economic growth. This news from $WMT shows how higher prices are affecting consumer spending and behavior on discretionary categories.

Source: CNBC, Sandbox Financial Partners

Borrowing among junk-rated firms slows to a trickle

Companies with speculative-grade credit ratings have slowed their pace of borrowing, illustrating how rising interest rates have upended the pandemic-driven boom. Junk-rated companies have raised roughly $74 billion so far this year, just a quarter of the nearly $300 billion from the same period last year, according to Refinitiv. That has led to an $80 billion drop in the net supply of high-yield bonds, a figure that is expected to grow to $130 billion by the end of the year. Such a fall would mark the biggest annual decline on record. The extra yield investors demand to hold junk bonds over U.S. Treasurys has risen to 5 percentage points from 3.1 points in January. That is well below the recent high of 11 points in March 2020. High-yield bonds trading in the secondary market still total a lofty $1.4 trillion, fueled by the nearly $900 billion in new junk bonds that came to the market in 2020 and 2021. Back then, easy monetary conditions during the Covid-19 pandemic allowed companies to raise cash cheaply and reduce their overall debt.

Source: Wall Street Journal, Goldman Sachs

That’s all for today.

Blake

Welcome to The Sandbox Daily, a community of market participants for market participants to encourage thought leadership and embrace intellectual enlightenment.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.