The Sandbox Daily (8.29.2022)

Monetary Policy, the European energy crisis, U.S. equities testing the 50-DMA, and long COVID

Welcome, Sandbox friends.

Today’s Daily discusses the impact of the Jackson Hole Economic Symposium on the next FOMC announcement coming September 21st, the energy crisis roiling Europe, U.S. equity indices test a critical level of technical support, and quantifying long COVID’s economic impact.

Let’s dig in.

EQUITIES: Dow -0.57% | S&P 500 -0.67% | Russell 2000 -0.89% | Nasdaq 100 -0.96%

FIXED INCOME: Barclays Agg Bond -0.46% | High Yield -0.38% | 2yr UST 3.409% | 10yr UST 3.089%

COMMODITIES: Brent Crude +3.88% to $104.91/barrel. Gold -0.02% to $1,749.5/oz.

BITCOIN: +2.64% to $20,148

US DOLLAR INDEX: -0.03% to 108.771

CBOE EQUITY PUT/CALL RATIO: 0.76

VIX: +2.54% to 26.21

All eyes on the Fed

In 22 days, the Federal Reserve will convene at their next Federal Open Markets Committee (FOMC) meeting to discuss monetary policy and announce the future path of their two critical (albeit blunt) tools: 1) interest rate policy via the Fed Funds window and 2) balance sheet reduction via Quantitative Tightening (QT). As recently as last week, the market’s expectations on the next interest rate hike were divided roughly equal between a 50 bps hike and a 75 bps hike.

Last Friday at the Jackson Hole Economic Symposium, central bankers and policymakers from around the world gathered to discuss the necessary policy measures to combat decades-high inflation.

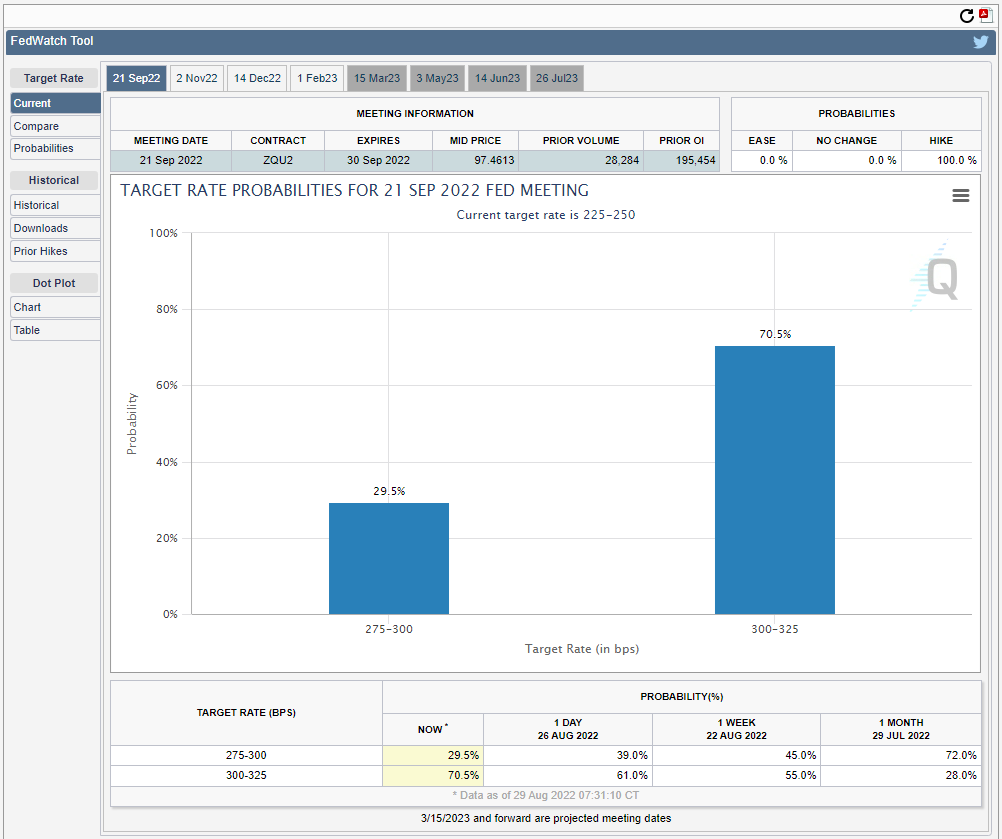

Specific to the United States, Federal Reserve Chairman Jerome Powell delivered a stern message: higher interest rates, slower growth, and a softening of the labor market will “bring some pain to households and businesses,” but the Federal Reserve is laser-focused on tamping down decades-high inflation. In fact, President of the Federal Reserve Bank of Minneapolis, Neel Kashkari, was “happy” with Friday’s price action and had this to say in response to the massive market sell-off following Jerome Powell’s speech: “people now understand the seriousness of our commitment to getting inflation back down to 2%.” Today, the market has firmly repriced the expectation for a 75 bps hike (70.5% probability) versus a 50 bps hike (29.5%).

Source: CME FedWatch Tool, Bloomberg

European energy crisis

The impact of Russia's war in Ukraine – and the combination of sanctions and embargoes drastically curbing Russian gas supplies – is beginning to have real effects on the West's standard (and cost) of living. In late July, the European Union's 27 member states agreed to voluntarily cut gas consumption by 15% between August 2022 and March 2023. Now a range of government-imposed restrictions, akin to the kind of restraints during wartime, are now rolling out. Here is a sample:

Germany: Public buildings, museums, and other landmarks — such as the Brandenburg Gate in Berlin — will no longer be illuminated overnight. In the city of Hanover, hot water was cut off at public buildings.

Spain: Congress agreed to temperature limitations — air conditioning no cooler than 27 degrees Celsius, or nearly 81 degrees Fahrenheit.

Italy: Air conditioning in schools and public buildings has already been limited in what the government labeled "Operation Thermostat."

France: Shopkeepers will now be fined for keeping doors open and air conditioning running. Illuminated signs will be banned between 1 a.m. and 6 a.m.

Since Russia launched the “special military operation” on February 24th (local Moscow time), Natural Gas prices have soared around the world. As Europe is heavily reliant on Russian Natural Gas, here is what the cost of electricity looks like across Europe where prices are more than 10 times their average for this time of year:

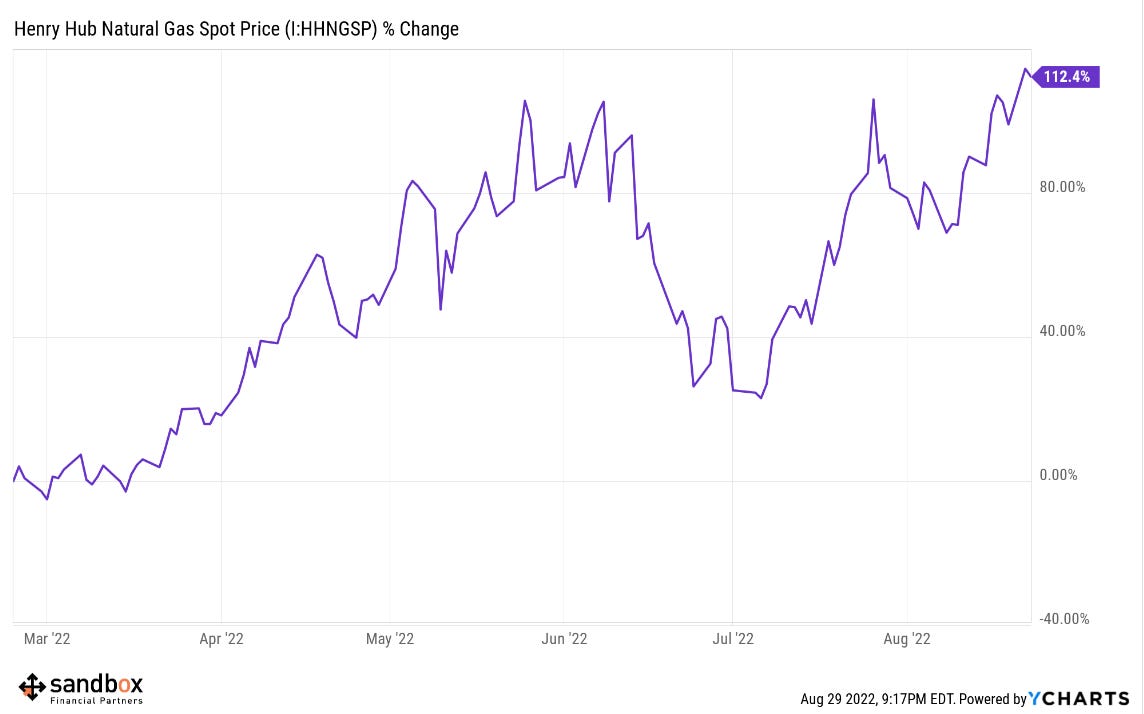

Meanwhile, Nat Gas prices in the United States are up +112.4% in roughly six months, as measured by the Henry Hub Natural Gas futures contracts.

Up next, the European Union is preparing to step into its energy market and intervene in the short term with urgent measures to dampen soaring power costs, per Commission President Ursula von der Leyen. “We’re seeing now with these exorbitantly high gas prices that we must decouple.”

Source: Axios, YCharts, Natural Gas Intelligence

Testing the 50-Day Moving Average

The summer rally off the mid-June lows stalled out two weeks ago when the major U.S. equity indices approached the 200-Day Moving Average (DMA) (as well as the key 61.8% level of Fibonacci retracement of the 2022 bear market). This was a perfectly logical place to see a rejection of this recent strength – with equities pressing against key overhead supply zones, the U.S. dollar beginning to reassert strength, and those stubborn Treasury yields backing up once again.

Well, after Federal Reserve Chairman Jerome Powell threw a wet towel on the summer rally in a brief 8-minute speech on Friday from the Jackson Hole Economic Symposium, the major U.S. indices are now headed lower to a key area of support: testing the 50-DMA, which is where equities broke above in mid-July. For those who follow technicals, this is a critical level where bulls want to see support and bears want to see price break definitively below. On the bright side, most major indices are holding up, at least for now.

Investors should closely watch how the major U.S. indices trade around their respective 50-DMAs. A bounce off these critical technical levels will favor the bulls, while undercutting the 50-DMAs would present a technical breakdown and a possible retest of the June lows.

Source: Bespoke Investment Group

Quantifying long COVID’s economic impact

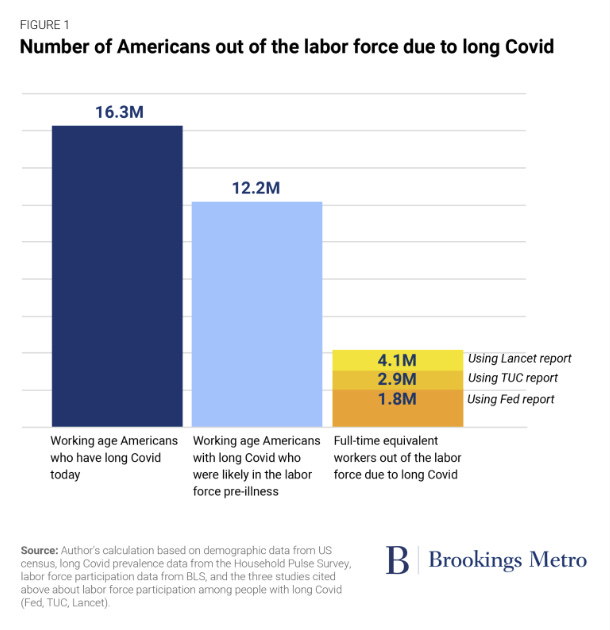

America’s ongoing labor shortage begs an important question: where have all the workers gone? There are 10.7 million unfilled jobs in the United States, according to the latest report from the U.S. Bureau of Labor Statistics. Some economists point to the high numbers of workers quitting amid the Great Resignation. New research highlights another troubling factor that may bear part of the blame: long COVID.

A Brookings Institution report published last week says an estimated 16 million working-age Americans (between ages 18 to 65) are experiencing COVID symptoms long after infection. The condition, dubbed long COVID, can include brain fog, fatigue, breathing problems, muscle pain, headache, chest pain and even anxiety or depression — all symptoms that can make it challenging for people to work. The Brookings report estimates that between 2 million and 4 million of those people are currently out of work due to long COVID.

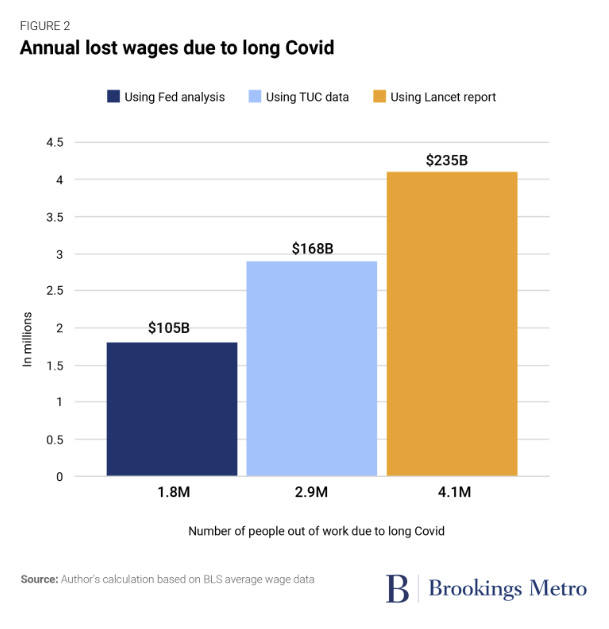

What’s more, if one uses the average U.S. wage of $1,106 per week, the United Kingdom’s Trades Union Congress (TUC) estimate of 3 million people out of work due to long COVID translates to $168 billion a year in lost earnings. This is nearly 1% of the total U.S. Gross Domestic Products (GDP). Using The Lancet study estimate of 4 million out of work, the number grows to $230 billion. And this number does not include downstream impacts such as lower productivity of people working while ill or health care costs incurred.

Long COVID is producing a meaningful drag on U.S. economic performance and household financial health.

Source: Brookings Institution, Barron’s, Centers for Disease Control and Prevention

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.