The Sandbox Daily (8.8.2022)

Coinbase and BlackRock team up, negative EPS surprises, reviewing the path of the Fed Funds Rate, the greatest corporate acquisitions, and a survey on the rental market

Welcome, Sandbox friends.

Today’s Daily discusses the announcement of the crypto partnership between Coinbase and BlackRock, the stock performance of S&P 500 companies that have produced negative EPS surprises in 2Q22, a look at the Fed Funds Rate to determine if the market is fighting the Fed, a (fun) list of the 10 greatest acquisitions of all time, and an in-depth survey on the skyrocketing rental market.

Let’s dig in.

EQUITIES: Russell 2000 +1.01% | Dow +0.09% | S&P 500 -0.12% | Nasdaq 100 -0.37%

FIXED INCOME: Barclays Agg Bond +0.45% | High Yield +0.09% | 2yr UST 3.207% | 10yr UST 2.748%

COMMODITIES: Brent Crude +1.41% to $96.32/barrel. Gold +0.81% to $1,805.7/oz.

BITCOIN: +2.97% to $23,950

VIX: +0.66% to 21.29

CBOE EQUITY PUT/CALL RATIO: 0.58

US DOLLAR INDEX: -0.22% to 106.382

Coinbase and BlackRock partner to provide institutional clients direct access to Bitcoin

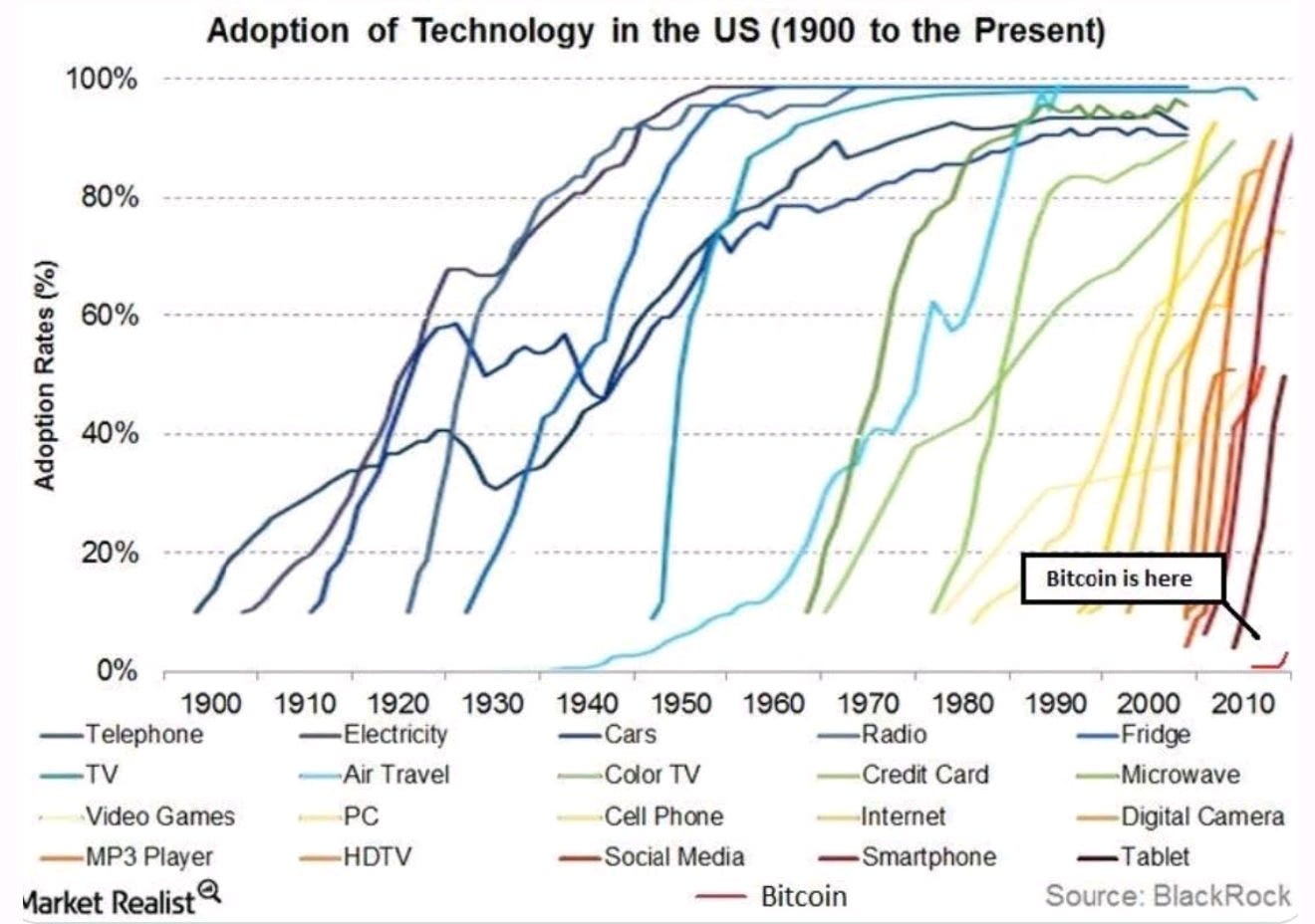

Last week, Coinbase announced a partnership with Blackrock to provide institutional clients with direct access to crypto, starting with bitcoin. At the core of the partnership will be an interconnection between Coinbase Prime and BlackRock’s Aladdin. Coinbase Prime is an institutional prime brokerage platform that offers its 13,000 clients custody and advanced trading solutions. Aladdin is BlackRock’s portfolio management software that supports nearly $22 trillion USD in assets managed by 55,000 investment professionals. Through this partnership, Aladdin’s user base will have access to Coinbase Prime’s prime broker, trading, reporting, and custody solutions. According to Max Branzburg, Vice President of Product at Coinbase, this deal could usher trillions of dollars into the crypto asset class in the coming years.

Source: Yassine Elmandjra, Ark Investment Management, Barron’s, Financial Times, Dan Tapiero

Market not punishing negative EPS surprises reported by S&P 500 companies for Q2

To date, 87% of the companies in the S&P 500 have reported earnings for the second quarter. Of these companies, 75% have reported actual EPS above the mean EPS estimate, which is below the five-year average of 77%. In aggregate, earnings have exceeded estimates by 3.4%, which is also below the five-year average of 8.8%. Given this underperformance relative to the five-year averages, how has the market responded to negative EPS surprises?

Well, the market has not punished S&P 500 companies that have reported negative EPS surprises on average. Companies that have reported negative earnings surprises for Q2 2022 have seen no price change (0.0%) on average two days before the earnings release through two days after the earnings release. This percentage is well above the five-year average price decrease of 2.4% during this same window for companies reporting negative earnings surprises. In fact, if this is the final percentage for the quarter, it will mark the first time the index has not seen a negative price reaction on average to negative EPS surprises reported by S&P 500 companies for a quarter since Q1 2009 (+0.3%).

Source: John Butters, FactSet

Why the market wants to fight

Martin Zweig's Winning on Wall Street, first published in 1970, is always on short lists of recommended reading for up-and-coming students of the markets. It was in this book that Zweig coined the famous phrase "don't fight the Fed," a concept that is one of the keys to keeping a portfolio on the right side of history. For most of the last few decades, "don't fight the Fed" meant risk-on mode. Investors were rewarded for keeping their foot on the gas pedal as central bank liquidity dampened volatility and drove outsized beta returns.

Today, inflation is at a 41-year high, and the Fed is in its most aggressive tightening cycle since 1994. Those two conditions differentiate this period from those leading up to the last few recessions. In this market, not fighting the Fed means accepting the idea of a longer hiking cycle and a higher terminal rate. But to date, the market isn’t ready to accept that.

The market is pricing in just about 75bps more in rate hikes, a peak in the Fed funds rate in 4Q 2022, and rate cuts starting a year from now. And yet, these expectations come as the Fed signals that it will tighten well into 2023, with the policy rate ending next year at least 50bps higher than what markets are pricing. This chart highlights the diverging expectations for the Fed’s policy rate:

The market seems to be pricing in something like the last cycle, using any plausible datapoint to believe in a quick return to easy money policies. The 1970s provide a useful, albeit imperfect, example of what is more likely to occur. That decade featured quicker bouts of inflation and shorter, more volatile economic cycles. Contrast that environment with the 2010s, when monetary stimulus dampened volatility and produced the longest expansion and bull market in history.

Source: Joe Zidle, Chief Investment Strategist at Blackstone Private Wealth Solutions

Mergers and Acquisitions

Growth is generally achieved one of two ways: build or buy. Bypassing the former and focusing on the latter, mergers and acquisitions are often how more mature businesses grow their user base, diversify their product offering, expand into new markets, and/or achieve greater top/bottom line growth. M&A can be a difficult, albeit profitable, exercise in long-term growth trajectories; future synergies can establish amazing enterprises and new products/services, or never materialize and the transaction becomes a burden on both the acquired and the acquiree. What’s more – C-Suite executives, sell side analysts, financial media, and the broader investing public often cannot come to consensus on what defines a successful merger – or stated differently – how to quantify and sort the results post-merger.

A recent list produced by 10kreader.com caught financial media by storm with their published list. Who do you have on your list?

Source: Sandbox Financial Partners, 10kreader.com

Skyrocketing rent, explained

In the past year, nearly every essential good or service – food, utilities, transportation – has escalated in price. But hikes in rent, typically the biggest monthly expense, have hit especially hard and effect the estimated 44 million renters in the United States. The Hustle recently ran a survey of 2.3k renters and 740 landlords to gain more insight into how much rent has gone up in the past year, and why landlords are boosting up their rates.

Among the survey’s findings:

71% of renters had rent hikes in 2021-2022

The average increase was 14.6% (or $275/mo)

In certain hot spots (Miami, San Diego, Austin), average rent went up 25%+

4 out of every 10 renters spend more than 30% of their gross income on rent

More than half of all landlords cite market demand as the reason for rent hikes

Source: The Hustle

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.