The Sandbox Daily (9.14.2022)

Future Proof, S&P 500 technical setup, quad witching, Produce Price Index August report

Welcome, Sandbox friends.

Today’s Daily discusses the technical setup on equities following yesterday’s market response to the August Consumer Price Index (CPI) report, quad witching to come on Friday, and the Producer Price Index (PPI) shows some moderation in prices. But first, a few last pictures to share from our time at the Future Proof wealth management festival.

Let’s dig in.

Editor’s note: Future Proof

Brian and I wrapped up our time at the Future Proof wealth management festival in Huntington Beach, California. This event brought together some of the world’s most prominent figures and emerging minds from all walks of life at the intersecting spheres of finance, investing, technology, business, pop culture, creative arts, and social impact. Here is an article from the Los Angeles Times with their reporting of Future Proof. Enjoy the final installment of photos from the fourth and final day!

Presentation by HALO Technologies

Art exhibition

The Compound and Friends live podcast stream on the current state of the RIA industry, featuring Michael Batnick, Shirl Penney, and Josh Brown (L to R)

Sandbox Financial Partners

Isaiah Thomas (NBA) and Dexter Fowler (MLB)

Big Boi and Sleepy Brown (of Outkast)

Fitz and The Tantrums

Markets in review

EQUITIES: Nasdaq 100 +0.84% | Russell 2000 +0.38% | S&P 500 +0.34% | Dow +0.10%

FIXED INCOME: Barclays Agg Bond +0.12% | High Yield +0.15% | 2yr UST 3.788% | 10yr UST 3.404%

COMMODITIES: Brent Crude +1.63% to $94.69/barrel. Gold -1.06% to $1,709.1/oz.

BITCOIN: +0.23% to $20,190

US DOLLAR INDEX: -0.18% to 109.615

CBOE EQUITY PUT/CALL RATIO: 0.73

VIX: -4.07% to 26.16

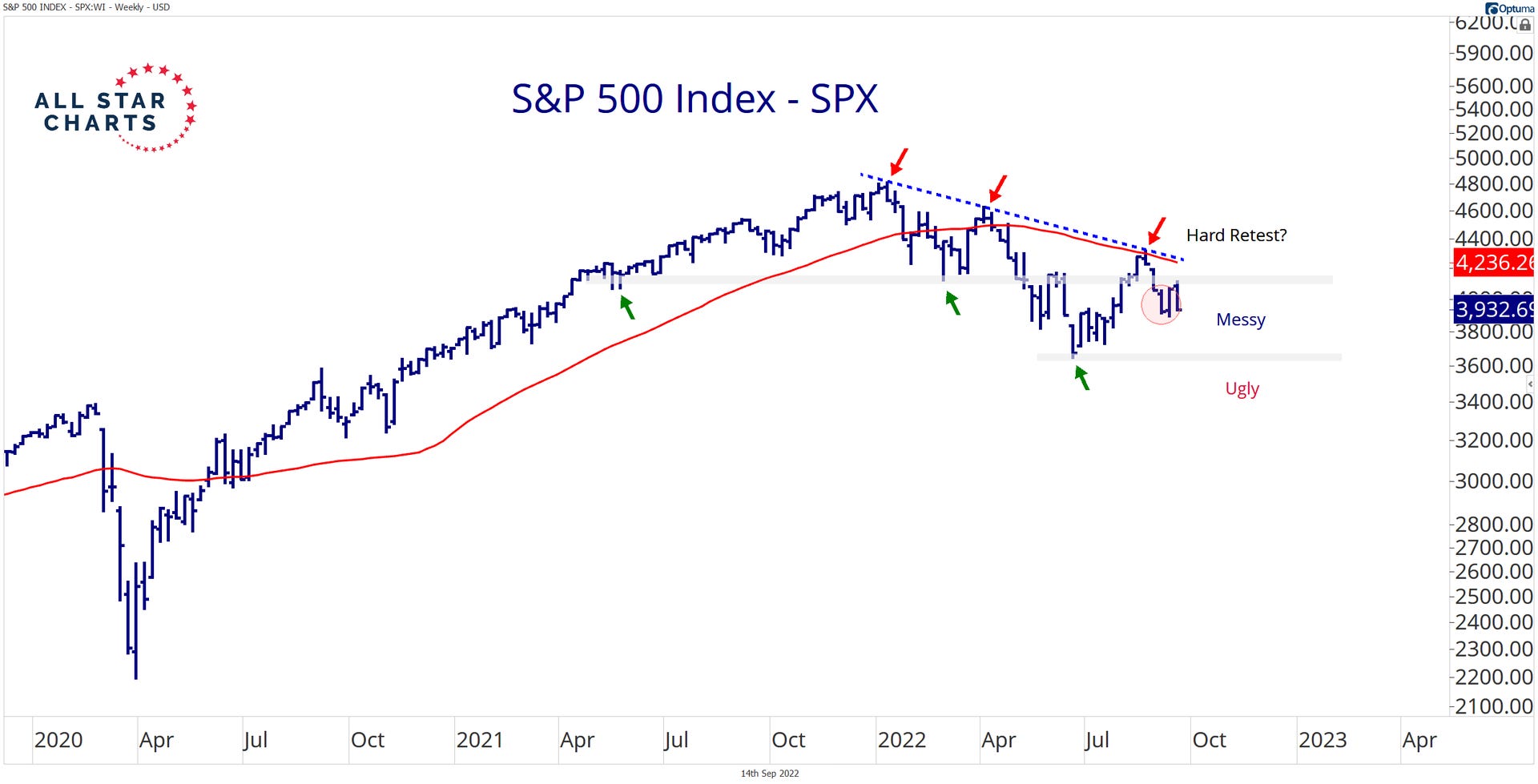

The bears take over

After a strong four day rally, the bears let us know they’re still here after yesterday’s ugly reception to inflation. Trends in the equity market can be described as neutral with a bearish bias – the three major averages trade below their 50 and 200-day moving averages but above their respective June lows. Rangebound.

There are signs that downside momentum is waning, but we need to see the index hold above the moving averages while volatility subsides to make a stronger case for a lasting rally. This next chart shows the S&P 500 (SPX) trading below a downward-sloping 200-day moving average and under a major horizontal resistance zone at 4,200.

As long as prices remain above the June pivot lows, we could see further basing action. From a tactical standpoint, this level could be the line in the sand for the S&P 500. If we undercut those June lows, expect further selling pressure and a fresh leg to the downside for stocks.

Source: Potomac Fund Management, All Star Charts

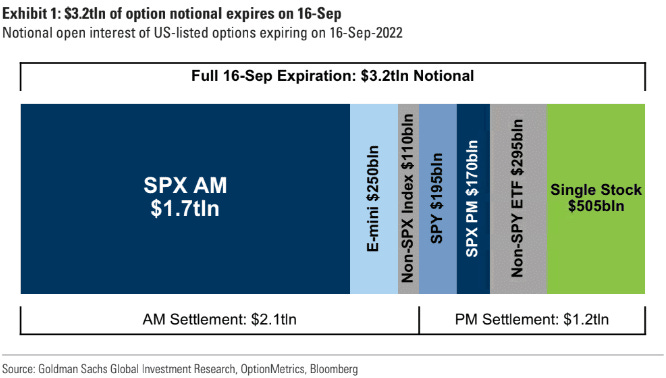

Buckle up for quad witching on Friday

This Friday's quad witching options expirations can generate a lot of market volatility. At the end of each quarter, the options markets' align – the options for futures, stock futures, indexes, and individual stocks all expire on the same day. During quad witching options expiration, trading volumes are heavy, and volatility often spikes as options traders simultaneously cover or roll their options.

Friday's option expiration of equity options is unusually large. A report from Goldman Sachs suggests ~$3.2 trillion notional of options are expiring. As such, market moves may be exaggerated due to options expiration.

Source: Goldman Sachs, Lance Roberts

Producer Price Index inflation moderates

The Producer Price Index (PPI) for final demand slipped -0.1% in August, its second consecutive decline and in line with expectations. It was largely attributed to a 6.0% drop in energy prices, led by gasoline – similar to what we saw in yesterday’s Consumer Price Index (CPI) report. Food prices were flat. PPI ex-food and energy increased 0.4%.

On a year-over-year basis, PPI for final demand came down to +8.7% from +9.8% in the previous month and a peak of 11.7% back in March. It was the lowest inflation rate in a year, although still much higher than pre-pandemic. PPI ex-food and energy posted a +7.3% YoY gain, also below its cycle peak, and the slowest pace since October 2021. Price pressures eased across most stages of production, which suggests that producer prices will continue to moderate.

Bottom line, both PPI and CPI inflation continue to run at elevated rates, which implies that the Fed will remain on its aggressive tightening path for now.

Source: Ned Davis Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.