The wheels on the bus screaming rates, rates, rates

The Sandbox Daily (1.8.2025)

Welcome, Sandbox friends.

Today’s Daily discusses:

a huge level of interest for rates come into focus

Let’s dig in.

Blake

Markets in review

EQUITIES: Dow +0.25% | S&P 500 +0.16% | Nasdaq 100 +0.04% | Russell 2000 -0.48%

FIXED INCOME: Barclays Agg Bond +0.11% | High Yield +0.13% | 2yr UST 4.283% | 10yr UST 4.685%

COMMODITIES: Brent Crude -1.14% to $76.17/barrel. Gold +0.57% to $2,680.6/oz.

BITCOIN: -2.69% to $94,365

US DOLLAR INDEX: +0.45% to 109.029

CBOE TOTAL PUT/CALL RATIO: 0.78

VIX: -0.67% to 17.70

Quote of the day

“Luck is what happens when preparation meets opportunity.”

- Seneca

A huge level of interest for rates come into focus

The deterioration across many corners of the market over the last few weeks has the attention of many.

While index prices have proved resilient, the churning under the hood should not be dismissed. Lackluster market breadth (exhibit below) and traditional momentum gauges like MACD have rolled over – leading to some early concern if equities are headed for a long winter.

One culprit for the messy tape are U.S. Treasury yields, whose short-term breakout since December 18 remains a meaningfully bearish headwind for stocks.

Just yesterday, President-elect and hyper market-focused Donald Trump quipped that “interest rates are far too high.”

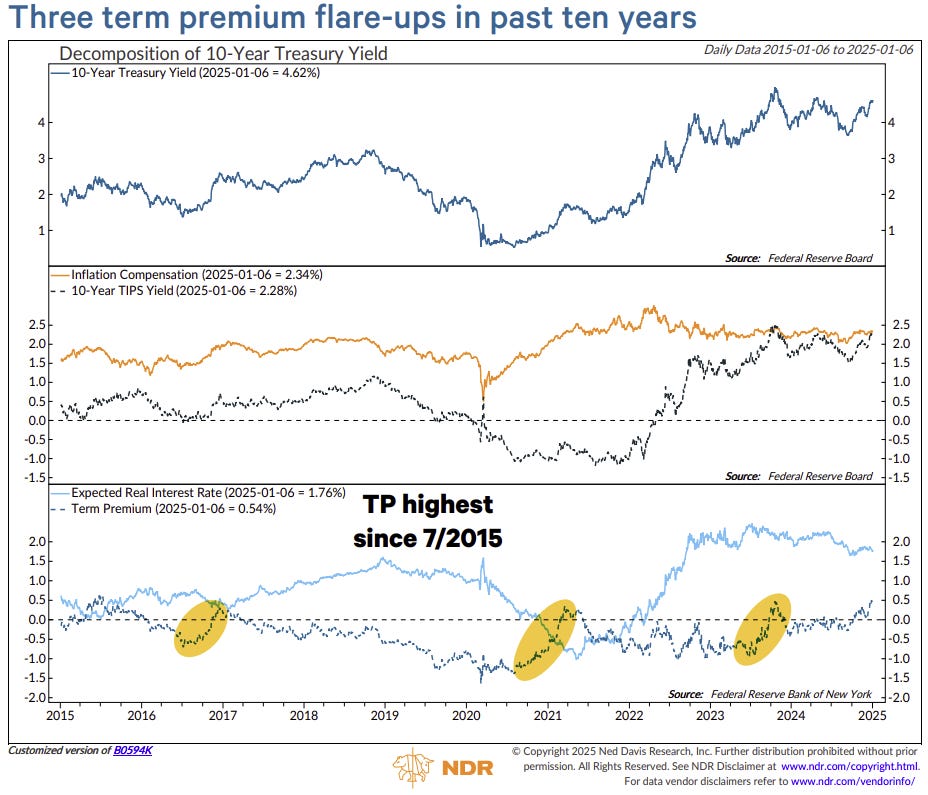

Treasury yields have been on the move for various reasons, including but not limited to a rising term premium (similar to the first Trump election – see below), higher expected economic growth under a Trump 47 Presidency, and a modest increase in inflation expectations.

The 10-year yield spent much of the last year oscillating back and forth between 3.8% and 4.6%.

Since the September 18 FOMC meeting – when the first interest rate cut was announced by Fed Chair Jerome Powell – the 10-year Treasury has marched higher from 3.65% to 4.68% in nearly a straight line.

So, while the key policy Fed Funds Rate has been slashed by 1%, the much-followed 10-year market rate has increased by that same amount.

The current level is an important spot which should become a fiery battleground in the days and weeks to come. At ~4.7%, this coincides with the April 2024 peak in yields and must be considered a significant yield-based area of resistance.

If/when this level successfully holds and results in a turn back lower for yields, such a move would likely be greeted positively by risk assets and should result in a much-anticipated January bounce.

On the flip side, if 4.7% is exceeded on the 10-year UST, one could reasonably expect the S&P 500 undercutting ~5830-5860, which is critical support for U.S. equities and of similar importance to the market. In this scenario, bears would be rejoicing around the winter campfire.

Source: StockCharts.com, Ned Davis Research

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures at the Sandbox Financial Partners website: