Treasury yields stall out, plus the pending maturity wall, stock/bond correlations, and mortgage payments

The Sandbox Daily (8.7.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

Treasury yields stalling out

the corporate debt maturity wall

stock and bond correlations rise to highest levels in over 25 years

mortgage payments up nearly 20% from one year ago

Let’s dig in.

Markets in review

EQUITIES: Dow +1.16% | S&P 500 +0.90% | Nasdaq 100 +0.87% | Russell 2000 +0.08%

FIXED INCOME: Barclays Agg Bond +0.02% | High Yield +0.19% | 2yr UST 4.774% | 10yr UST 4.095%

COMMODITIES: Brent Crude -0.46% to $85.84/barrel. Gold -0.25% to $1,971.2/oz.

BITCOIN: +0.24% to $29,171

US DOLLAR INDEX: +0.06% to 102.079

CBOE EQUITY PUT/CALL RATIO: 0.66

VIX: -7.78% to 15.77

Quote of the day

“Large price changes tend to be followed by more large changes, positive or negative. Small changes tend to be followed by more small changes. Volatility clusters.”

- Benoit Mandelbrot, The Misbehavior of Markets

Treasury yields stalling out

Friday’s sharp reversal in U.S. Treasuries is notable given that yields have been backing up since mid-May.

This cloud of 4.3%-4.4% on the 5-year U.S. Treasury, a shelf of former highs this cycle, is a major area of importance that has acted as strong resistance for the last year.

The recent surge in yields should likely prove short-lived. Yields for this cycle peaked October of 2022 which is considered strong resistance; Friday’s about-face left the weekly candle firmly off peak levels. Additionally, sentiment seems quite one-sided with most expecting yields to rise further. And seasonality studies show August to be the strongest month of the year out of the last 20 on average.

Some minor backing and filling could be expected after the strong lift in yields for the past few weeks saw the 5-year move higher by roughly 40 bps. But, as long as yields remain below this key cloud level, risk assets should continue to find bids.

Source: FS Insight

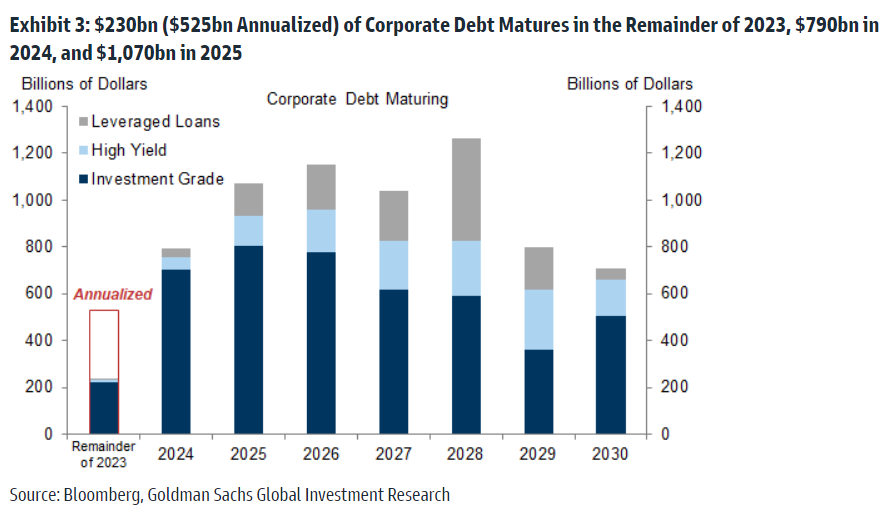

The corporate debt maturity wall

The Fed’s tightening cycle has pushed marginal funding costs for businesses sharply higher over the past couple of years. If interest rates remain high, companies will need to devote a greater share of their revenue to cover higher interest expenses as they refinance their debt at higher rates.

The path for interest expense depends on future refinancing needs and interest rates. Refinancing needs will remain historically low over the next two years – about 16% of corporate debt will mature over the next 2 years, the low end of its 15-year range.

While near-term refinancing needs appear limited, the pace of corporate debt maturing picks up sharply from 2024 onward.

One upshot? The hit to corporate America from higher interest expenses could be less than anticipated by the market due to high cash balances that help buffer the hit.

Source: Goldman Sachs Global Investment Research

Stock and bond correlation has reached the highest levels in over 25 years

Bonds haven’t worked as a traditional hedge in what feels like years.

The recent move back above 4% for intermediate and longer duration bonds has served as a negative catalyst for equities, with stocks quickly coming under pressure as yields moved above this important threshold. In fact, the 1-month correlation between stocks and bonds skyrocketed back to levels haven’t seen since 1996.

Historically, U.S. Treasuries tend to rally when stocks are selling off and vice versa – meaning they are negatively correlated – and this relationship leads to a reduction in portfolio volatility, one of the fundamental reasons why people diversify their portfolios. The recent correlation reading between stocks and bonds is 0.82; the average from 2000 to 2022 was -0.3.

So, in order for stock indexes to find their footing, it’s going to important for this recent advance higher in rates to stall out and consolidate, if not outright reverse course. Moreover, investors of traditional asset allocation models of stocks and bonds would like to see this correlation relationship return to more historical measures.

A peak in yields might seem unusual given last week’s Fitch downgrade of the U.S. sovereign credit rating, massive Treasury supply issuance, and the recent Bank of Japan decision to adjust their yield curve control policy.

Source: Bloomberg

Mortgage payments up nearly 20% from one year ago

Mortgage payments are significantly more expensive than the prior year, thanks to homebuyers facing a tight supply amidst surging mortgage rates and home prices.

Here’s Redfin on the monthly payment affordability crisis plaguing so many:

The typical U.S. homebuyer’s monthly mortgage payment was $2,605 during the four weeks ending July 30, up 19% from a year earlier and down just $32 from early July’s all-time high [$2,637].

Back in June, Edward Seiler of Mortgage Bankers Association had this to say about the current affordability, or lack thereof, impacting the housing market: “For new home buyers, this is the worst situation since the end of the Great Recession." Seiler continued, "Current homeowners that were lucky enough to get a 2.75% interest rate in 2022 are in a great position, but for new home buyers looking to buy a first home, or those looking to move to another home, it's a very daunting proposition."

Source: Redfin, Yahoo Finance

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.