U.S. household debt by the numbers, plus tight credit conditions, housing (un)affordability, and higher-for-longer

The Sandbox Daily (11.7.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

total U.S. debt rises to $17.29 trillion dollars

tighter credit, lending conditions build case for Fed policy hold in December

housing affordability crisis

downstream impacts of higher-for-longer on housing

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +0.93% | S&P 500 +0.28% | Dow +0.17% | Russell 2000 -0.28%

FIXED INCOME: Barclays Agg Bond +0.53% | High Yield +0.01% | 2yr UST 4.913% | 10yr UST 4.569%

COMMODITIES: Brent Crude -4.06% to $81.72/barrel. Gold -0.68% to $1,975.1/oz.

BITCOIN: +1.87% to $35,589

US DOLLAR INDEX: +0.31% to 105.544

CBOE EQUITY PUT/CALL RATIO: 0.77

VIX: -0.54% to 14.81

Quote of the day

-Howard Marks, Howard Capital Management in I Beg to Differ

Total U.S. debt rises to $17.29 trillion dollars

Aggregate household debt balances increased by $228 billion (+1.3%) in the 3rd quarter of 2023 to reach a total of $17.29 trillion.

The household debt load has increased $3.1 trillion since the onset of the pandemic – despite record government stimulus and moratorium on various debt obligations and household expenses.

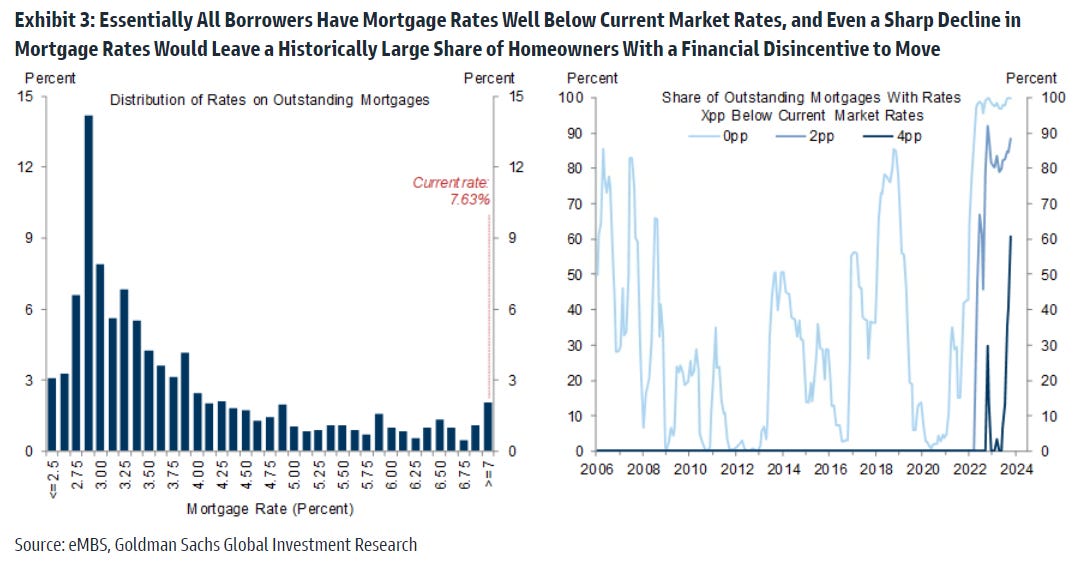

Mortgage balances were largely unchanged and stood at $12.14 trillion at the end of September – this makes sense given declining mortgage originations and higher interest rates capping transactions. Mortgages make up the overwhelming slice of the pie (orange bars below).

One reason for the tightening delay in the monetary policy transmission mechanism layered across the United States economy is mortgages, underpinning why the consumer continues to hold up so well in this environment.

As noted above, mortgages are the biggest consumer debt balance at $12.14 trillion. As noted below, over 80% of Americans are locked into 30-year fixed-rate mortgages under 5% – so increasing interest rates and tightening lending standards are not having the desired impact as past cycles.

BUT, the headliner in today’s Quarterly Report on Household Debt and Credit report from the New York Fed?

Credit card debt, of course, which stands at $1.08 trillion – having risen $48 billion, or +4.7%.

Three quick thoughts on credit cards and the popular consumer-is-in-big-trouble narrative:

Credit card balances at $1.08 trillion (navy blue bars below) are just a fraction of the limits available (light blue bars) around ~$4.5 trillion, so credit in aggregate is not stretched.

As Callie Cox of eToro points out below, the credit card debt load (liabilities) as a percentage of total deposits (assets) is near its lowest levels in 20 years: 6.1% of household deposits, up marginally from 5.8% last quarter.

The percentage of loans in serious delinquency, 90+ days, is virtually flat across all categories save credit cards, which yes have ticked higher but remain well below the pre-pandemic highs and miles away from the levels seen during the Global Financial Crisis.

For now, the consumer is mostly on fine footing, especially with the labor market holding up so well.

However, the sunset of government stimulus and relief programs, as well as diminishing savings and rising rates, should result in higher delinquency rates and charge-offs in the coming quarters.

Source: Federal Reserve Bank of New York, Quarterly Report on Household Debt and Credit, Callie Cox

Tighter credit, lending conditions build case for Fed policy hold in December

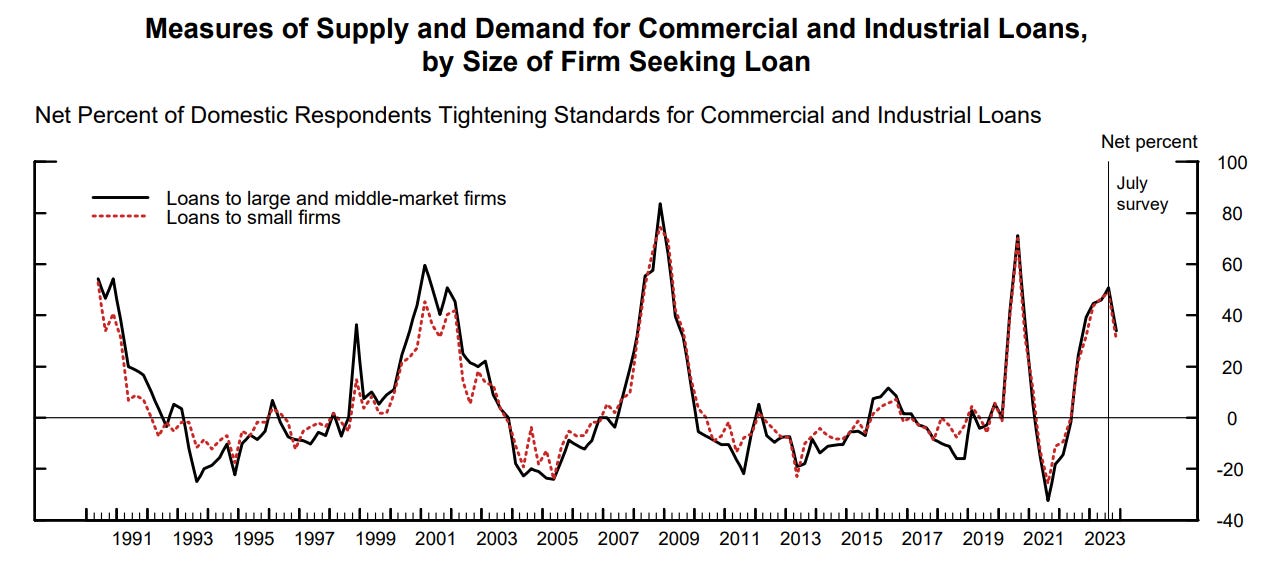

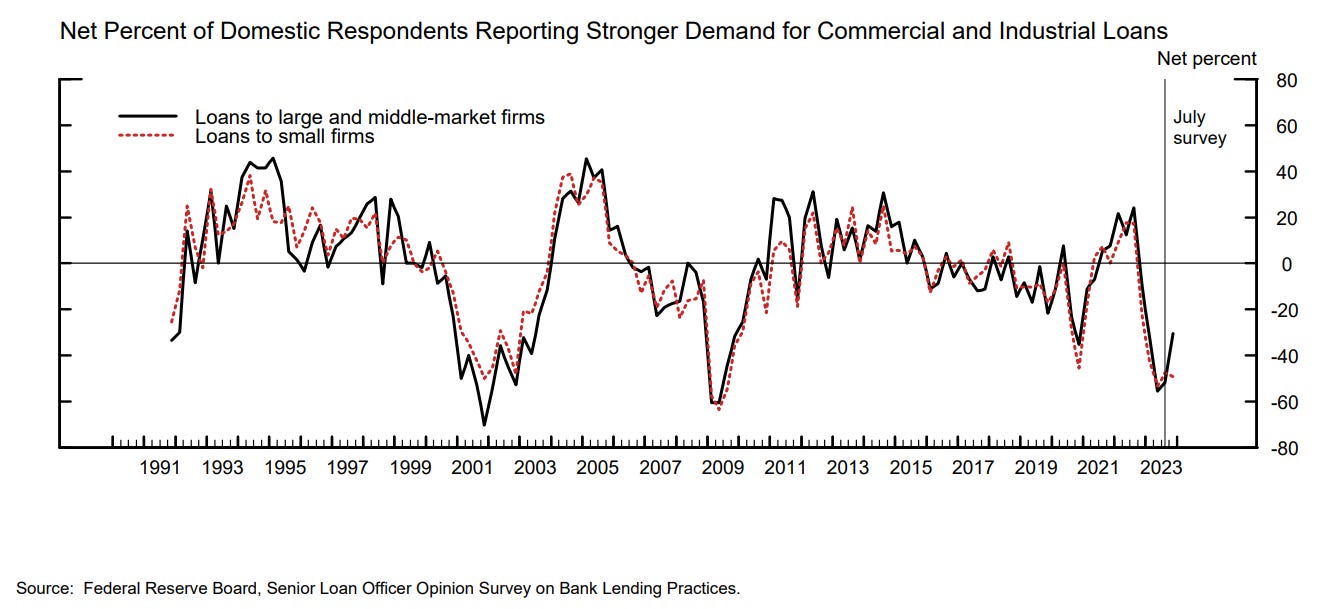

Credit conditions among banking institutions remain very tight.

In the latest Senior Loan Officer Opinion Survey (SLOOS) released yesterday, banks continued to tighten standards on commercial and industrial loans as well as commercial real estate loans but only a slightly slower pace.

Meanwhile, demand, which has shown early and tepid signs of a rebound, is still near the depths of the cycle – suggesting customers are being cautious about accumulating more debt amidst higher interest rates and an uncertain economic backdrop.

Overall, banks tightened access to credit due to a more uncertain economic outlook, reduced tolerance for risk, falling credit quality and collateral values, and higher funding costs.

For the banks themselves, a weaker economy is concerning but not necessarily catastrophic. In the years since the Global Financial Crisis, banks have been required to hold higher levels of capital to protect against credit losses and their ability to withstand economic and market shocks is evaluated annually during the Fed’s stress tests.

Source: Federal Reserve, Ned Davis Research

Housing affordability crisis

The annual income needed to afford a median-priced home in the U.S. has soared over the last three years.

The qualifying yearly income for a median-priced house in 2020 was $74,657. Redfin now says it $114,627, a 53% surge since the pandemic and the highest necessary annual income on record.

Housing affordability has dropped in half since the ultra-low interest rate environment of 2021.

Source: Redfin

Impact of higher-for-longer on housing

With interest rates higher across the curve and liquidity continuing to contract, an improvement in mortgage rates and housing activity would be welcome news to the Housing Food Chain.

Home sales remain well below trend, which puts stress on all aspects of this universe – both direct and indirect housing plays – that relies on constant churn of the housing market.

Think building supplies, business services such as Real Estate Brokerage/Mortgage Lending/Title/Legal Services, home improvement & specialty stores, home appliances, furniture, electricians, etc.

Source: J.P. Morgan Markets

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.