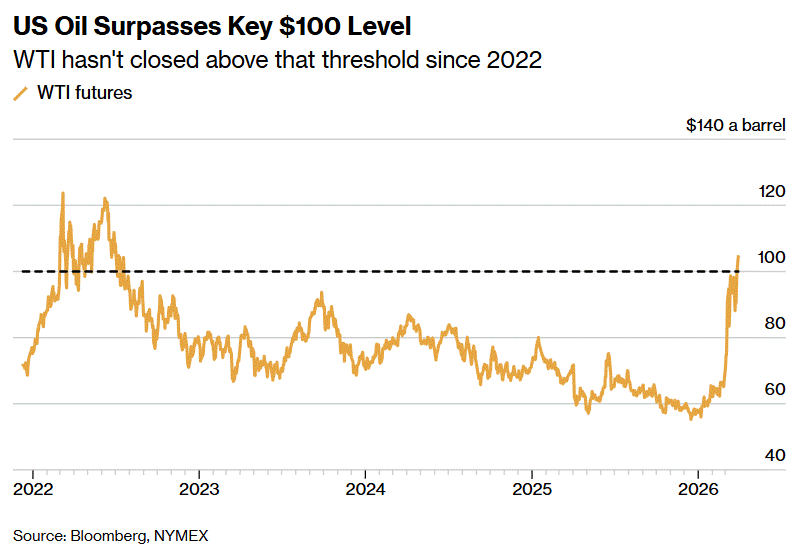

US oil settles above $100 a barrel for first time since 2022

The Sandbox Daily (3.30.2026)

Welcome, Sandbox friends.

Today’s Daily discusses:

$100 oil

Let’s dig in.

Blake

Markets in review

EQUITIES: Dow +0.11% | S&P 500 -0.39% | Nasdaq 100 -0.78% | Russell 2000 -1.46%

FIXED INCOME: Barclays Agg Bond +0.51% | High Yield +0.11% | 2yr UST 3.838% | 10yr UST 4.351%

COMMODITIES: Brent Crude +0.19% to $112.78/barrel. Gold +0.36% to $4,540.4/oz.

BITCOIN: +0.43% to $66,864

US DOLLAR INDEX: +0.33% to 100.48

CBOE TOTAL PUT/CALL RATIO: 0.96

VIX: -1.42% to 30.61

Quote of the day

$100 oil

U.S. oil prices are now trading above $100 a barrel for the first time since the United States and Israel launched a war against Iran.

The world remains beholden to the re-opening of the critical Strait of Hormuz, which Iran has effectively closed to oil tankers during the conflict.

Some 20-25% of the world’s oil supply and 20% of its liquefied natural gas passes through this critical shipping lane, and the ease with which it was shut down may permanently change how countries approach their own sovereign energy policies.

This conflict will require a new playbook going forward. Despite all the many conflicts in the Middle East over the years, not one has caused a total shutdown of the Strait of Hormuz.

Having parsed through many sell-side and independent research reports over the last few weeks, this post-war global economy will likely change in three key ways:

The world needs reserves away from the Middle East.

Most of the world’s excess oil sits on the wrong side of the Strait, making it largely inaccessible in the case of a shutdown. This will force countries to rethink the value of that spare capacity. Put another way, countries may look to re-categorize the excess supply that sits in this region, counting only a portion of it as actually accessible.

Greater emphasis on strategic stockpiles.

Once this conflict is over, countries will look to build domestic reserves to even higher levels than before. The U.S. never managed to refill its Strategic Petroleum Reserve to pre-2022 levels. Coming out of this, there will likely to be increased effort to do so, especially in Europe and Asia, which are really feeling the carnage from this oil disruption.

Higher prices for longer.

We likely see a premium on oil supplies that do not pass through the Strait. And, since energy is a global commodity, premiums on oil from one place will drive up prices overall, even if Strait supply lines trade at a discount.

The winners in all of this, of course, are companies in the energy sector. Several shops estimate 2026 earnings will be double its prior expectations.

The losers? Basically everyone else. Higher oil prices erode consumer spending power and raise a key input cost for companies, which must then absorb or pass along through higher prices. Even with a resolution to the war, corporate margins could be pressured, or prices passed through, resulting in a rebound in inflation, neither of which is good for stocks or the hope for lower interest rates.

While oil prices may stay higher in the short- to intermediate-term, stocks should rally on a resolution to the war, whenever that happens.

The Volatility Index (VIX) has now closed above 30. History shows that’s not necessarily a bad thing for forward returns.

Since 1990, when the VIX has closed between ~28 and ~33, the S&P 500’s forward 6-month return has averaged +9.5%. Compare that to the calm periods below 15, where forward 6-mo returns cluster around 5%.

In other words, elevated fear has created opportunity for patient investors that can stomach the volatility.

Sources: Bloomberg, Exhibit A

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures (click here)

Please see our SEC Registered firm brochure (click here)

Please see our SEC Registered Form CRS (click here)