Wall Street strategists upping their SPX targets, plus companies hoarding cash, positioning, and the labor market

The Sandbox Daily (2.23.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

Wall Street strategists up their price targets

cash held by corporations is at an all-time high

equity and cash positioning dynamics

labor market remains healthy 4 years after the pandemic

Let’s dig in.

Markets in review

EQUITIES: Dow +0.16% | Russell 2000 +0.14% | S&P 500 +0.03% | Nasdaq 100 -0.37%

FIXED INCOME: Barclays Agg Bond +0.37% | High Yield +0.06% | 2yr UST 4.694% | 10yr UST 4.251%

COMMODITIES: Brent Crude -2.37% to $81.69/barrel. Gold +0.74% to $2,045.8/oz.

BITCOIN: -0.97% to $50,995

US DOLLAR INDEX: +0.01% to 103.966

CBOE EQUITY PUT/CALL RATIO: 0.66

VIX: -5.43% to 13.75

Quote of the day

“Make living your life with absolute integrity and kindness your first priority.”

- Richard Carlson, Actor

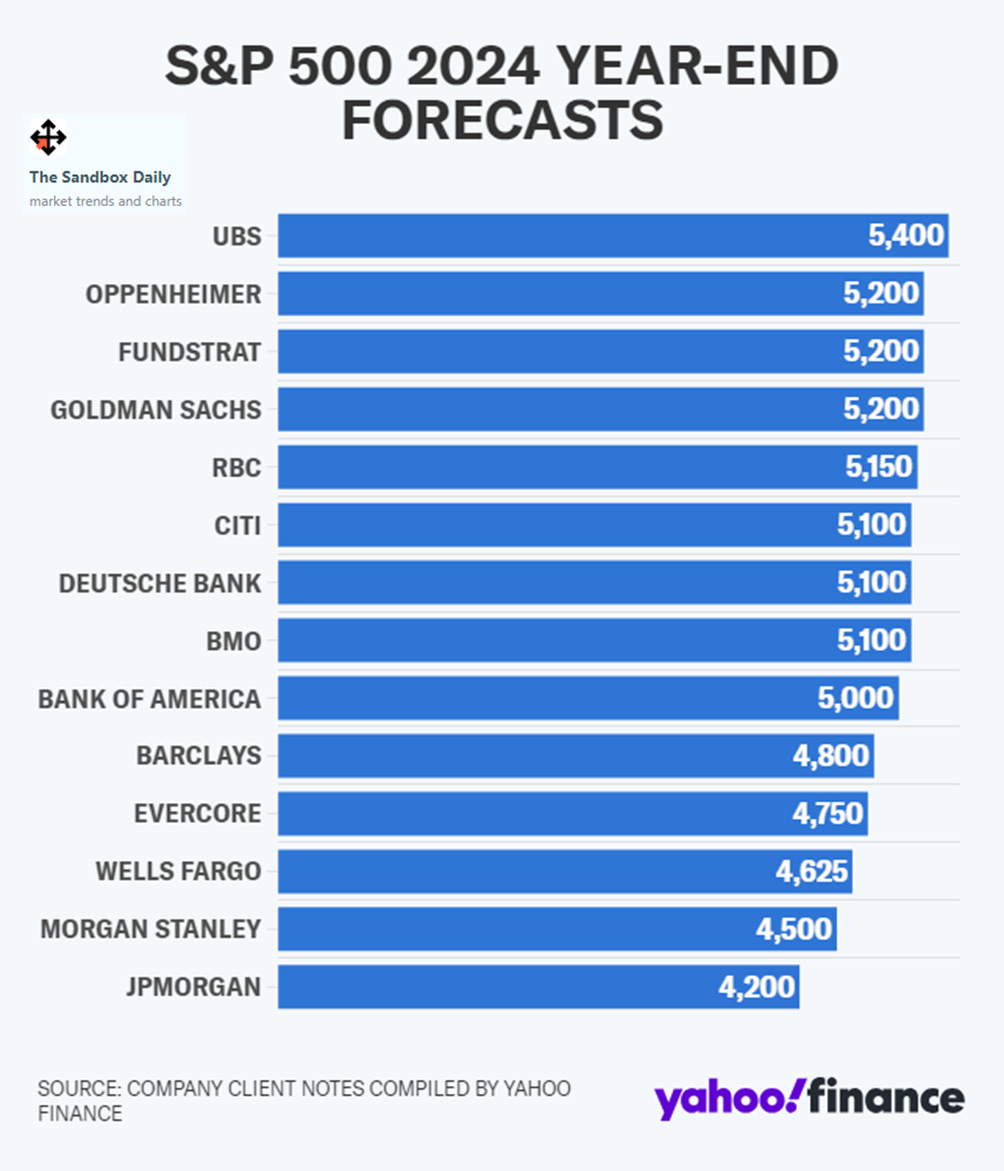

Wall Street strategists up their PTs

Just 8 short weeks into 2024, what’s changed this year?

Price.

So, here comes the street with their upgrades !

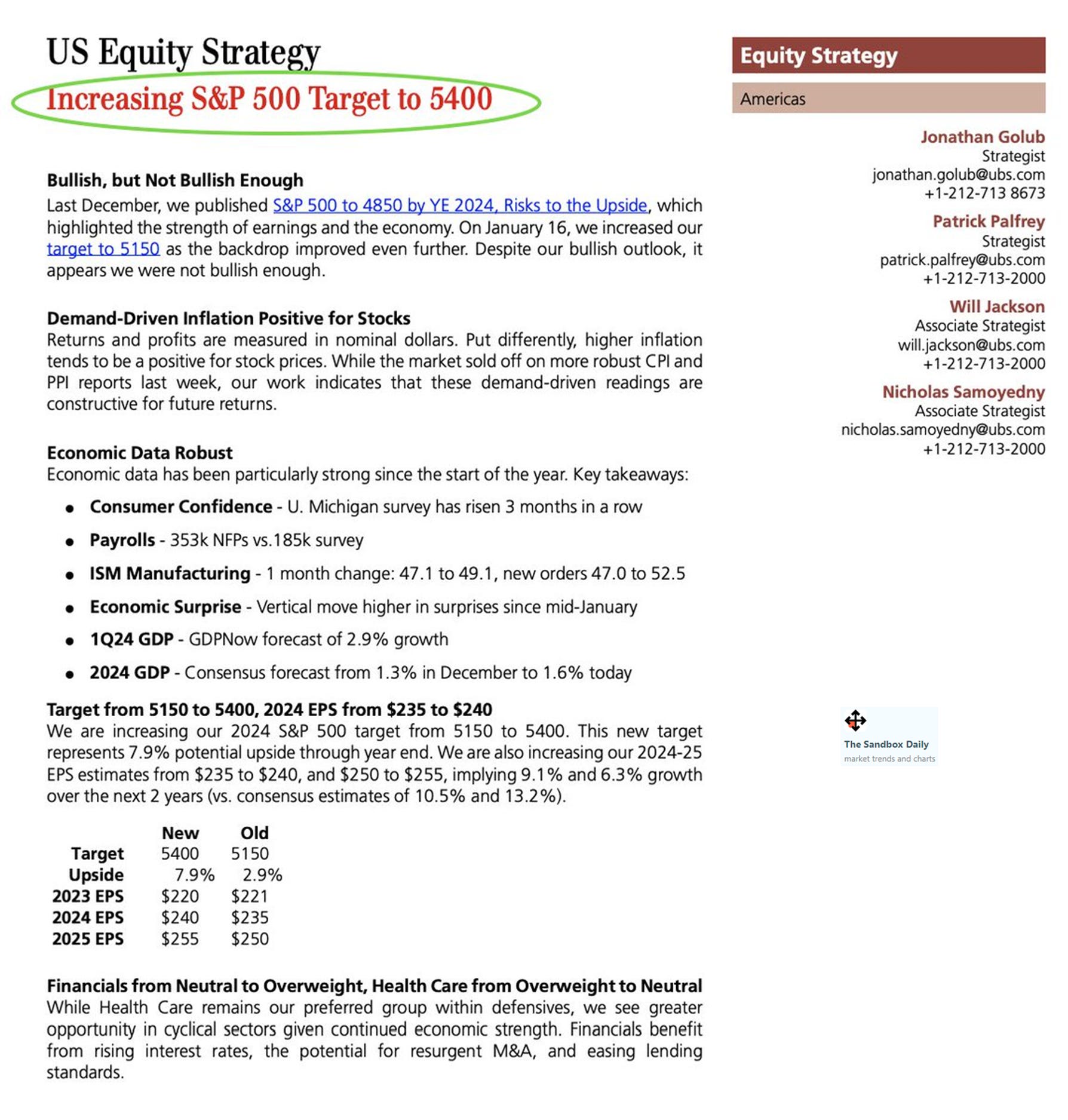

UBS strategists raised their 2024 Price Target for the S&P 500 again, saying their last hike – only 4 short weeks ago – was not bullish enough. Earlier this week, UBS lifted their year-end guide for the S&P 500 to 5400, implying roughly 6% upside from current levels.

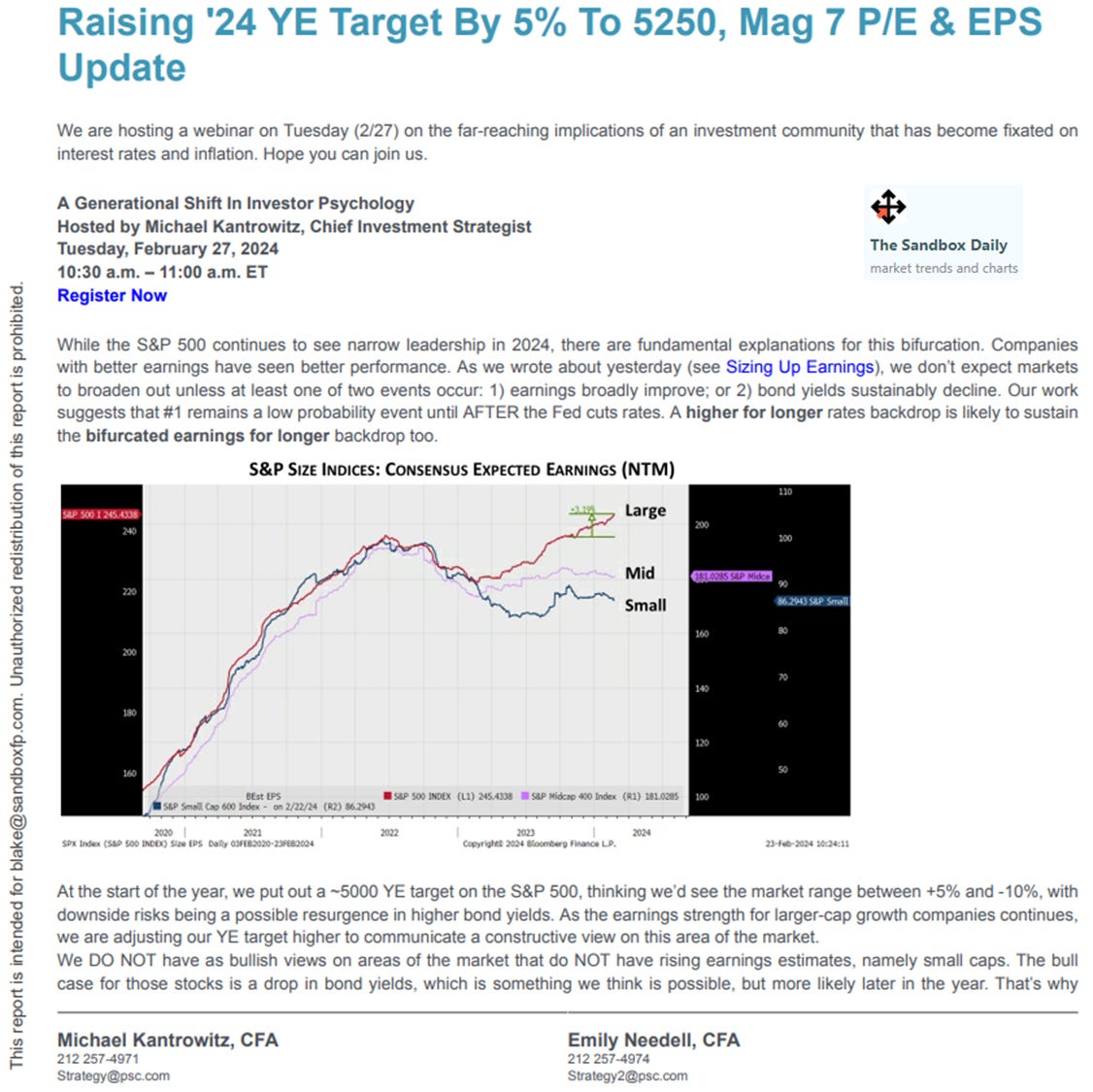

Over at Piper Sandler, Kantro and crew are taking their year-end target up from 5000 to 5250, which represents a 3% move higher from here.

Below are the year-end forecasts from the major firms, with an average target of 4950 (-2.8%) and median target of 5100 (+0.2%).

Our friends at Morgan Stanley (4500) and J.P. Morgan (4200) are likely feeling the pressure to catch up to where the puck is going.

On balance, these price targets still feel conservative.

Perhaps the uncertainty are the economy and its near-term future has filtered into strategists thinking, given the wide dispersion in outcomes that people are expecting:

Source: Josh Schafer (Yahoo Finance), Piper Sandler, Seth Golden, Mike Zaccardi

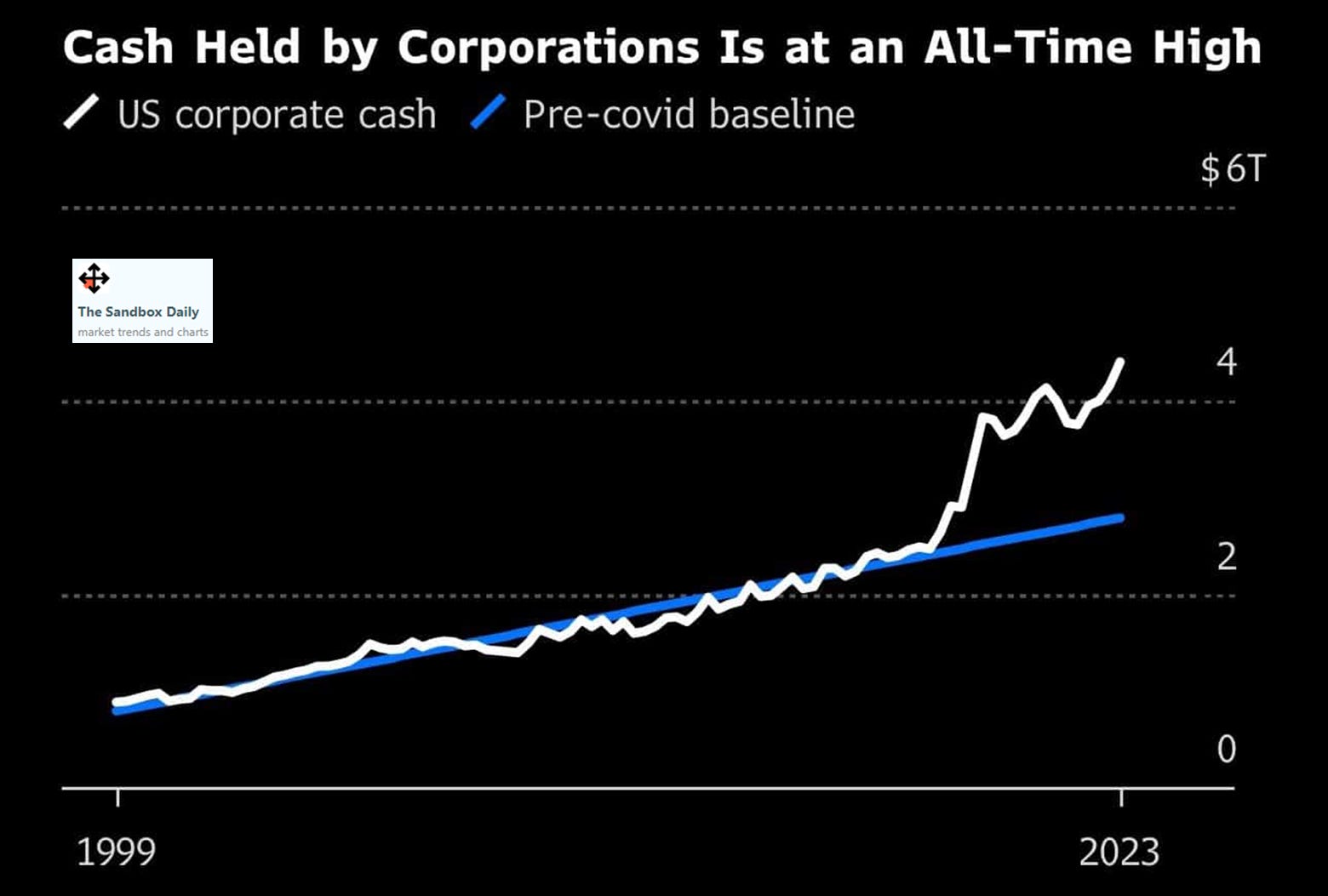

Cash held by corporations is at an all-time high

Companies are hoarding cash.

In fact, the amount of cash that companies hold on their balance sheets is at an all-time high and double the pre-pandemic trend.

Large amounts of cash are a good thing for shareholders in today's high interest-rate environment. Here’s two good reasons why:

Asset side: C-suites with excess cash on their balance sheet are investing at money market rates that are often higher than their borrowing costs. For shareholders, not only does the situation help/flow through to the income statement, but the cash allows some companies to buy back their shares and provide an additional tailwind to their stock price.

Liability side: In the 5 years preceding the pandemic, corporate debt securities outstanding rose on average by 3.5% per year. In 2020, corporate debt shot higher by 11% as corporations took advantage of historically low-interest rates to fortify their balance sheets. This means that corporate debt issuance lately has been below average, sparing some companies the need to borrow at higher interest rates.

Source: Bloomberg

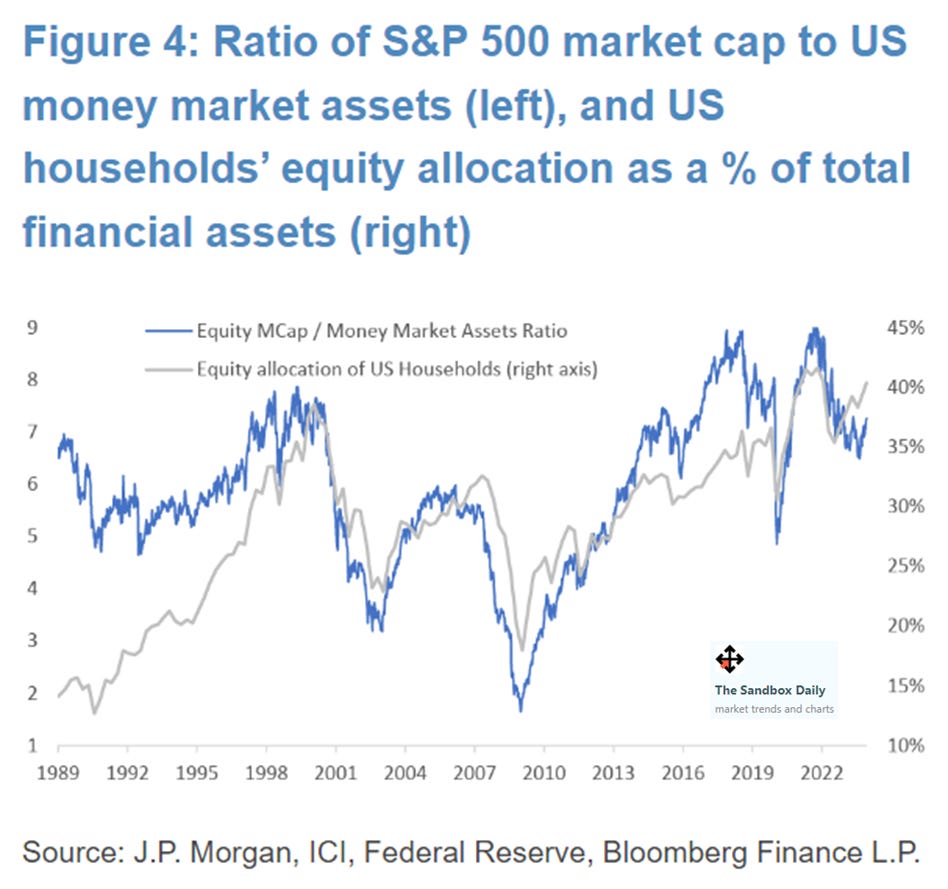

Equity and cash positioning dynamics

Investor positioning has increased significantly over the past few months, which may present an increasing headwind for the market.

Systematic strategies are running elevated equity leverage, with risk control portfolios’ (i.e. Volatility Targeting, Risk Parity) exposure near post-COVID highs (90th percentile) due to the low market volatility, and momentum strategies broadly long equities (outside of China) given the strong price trends. Meanwhile, Hedge Funds have also re-levered with both gross and net exposures currently registering at the 99% percentile over the trailing 12-months.

One common refrain from equity bulls is that there is a lot of dry powder that can continue to propel equity markets higher, for example pointing to the large pool of assets sitting in money market funds that could flow into the equity market.

However, as J.P Morgan notes, the asset base of money market funds is historically low relative to the size of the equity market (equity market cap / money market assets ratio is 80th percentile relative to the past 35 years of history), implied investor cash allocations are below average, and US households’ equity allocations are near record highs.

Source: J.P. Morgan Markets

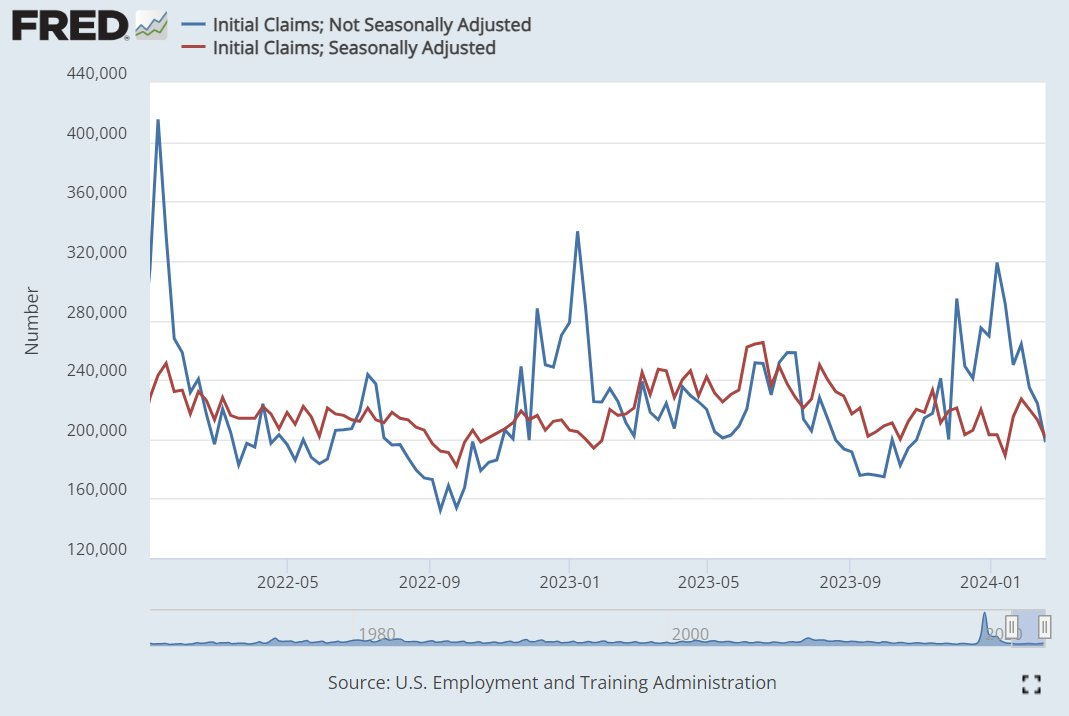

Labor market remains healthy 4 years after the pandemic

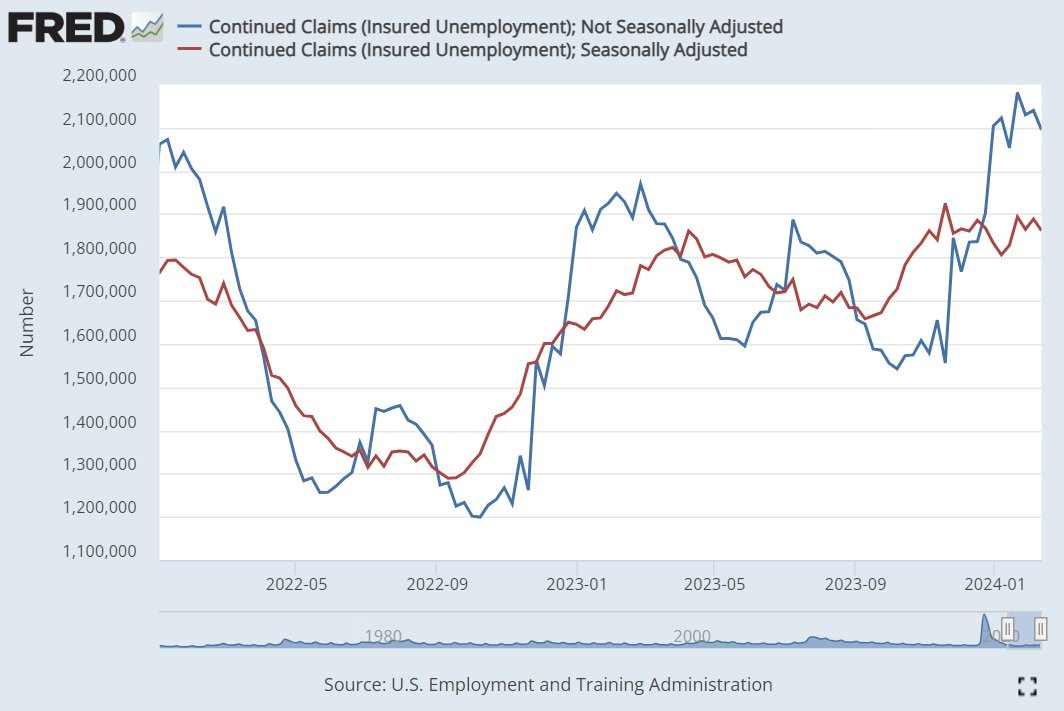

The U.S. labor market remains secularly tight – and to the shock of most market participants – quite healthy in the face of everything levied its way over the past 4 years.

Initial jobless claims are back to the low end of its range from the past two years.

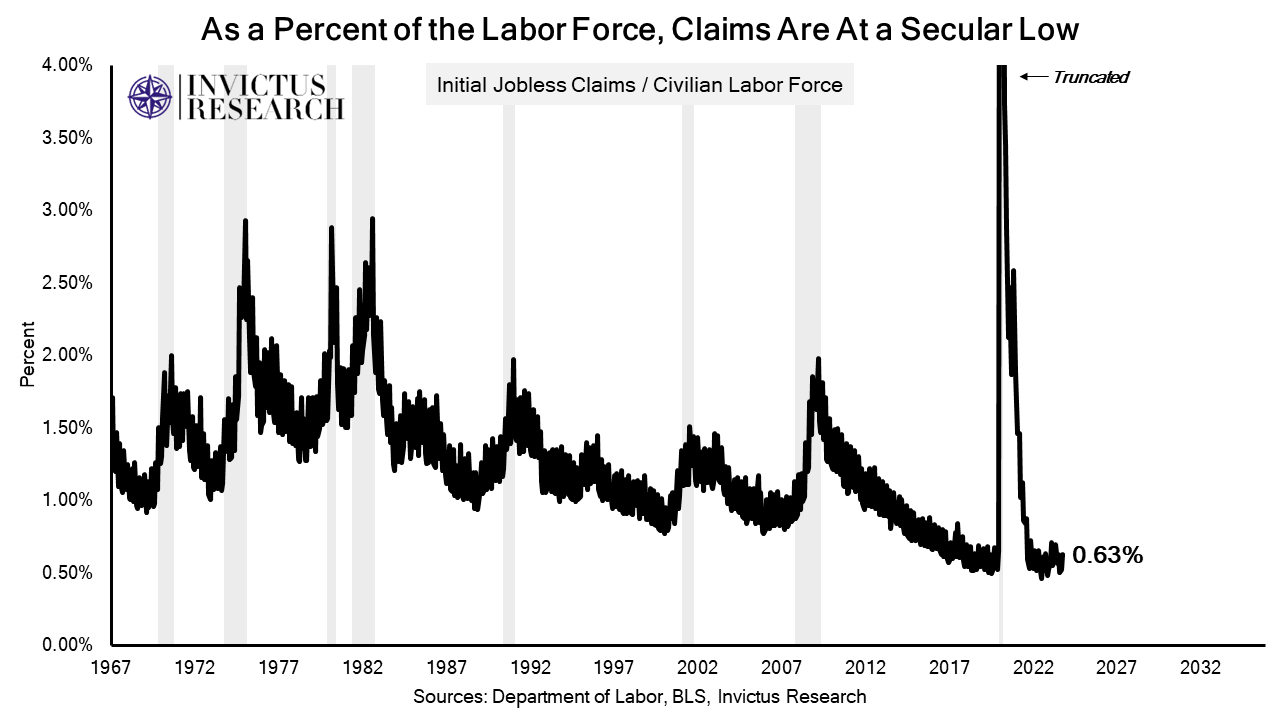

Even adjusting initial claims by the size of the labor force over multiple decades confirms as much:

And, as Bob Elliott (of Bridgewater fame) notes, continuing claims sub 2M “are in line with an unemployment rate that is below 4%”, showing “no signs of deterioration.”

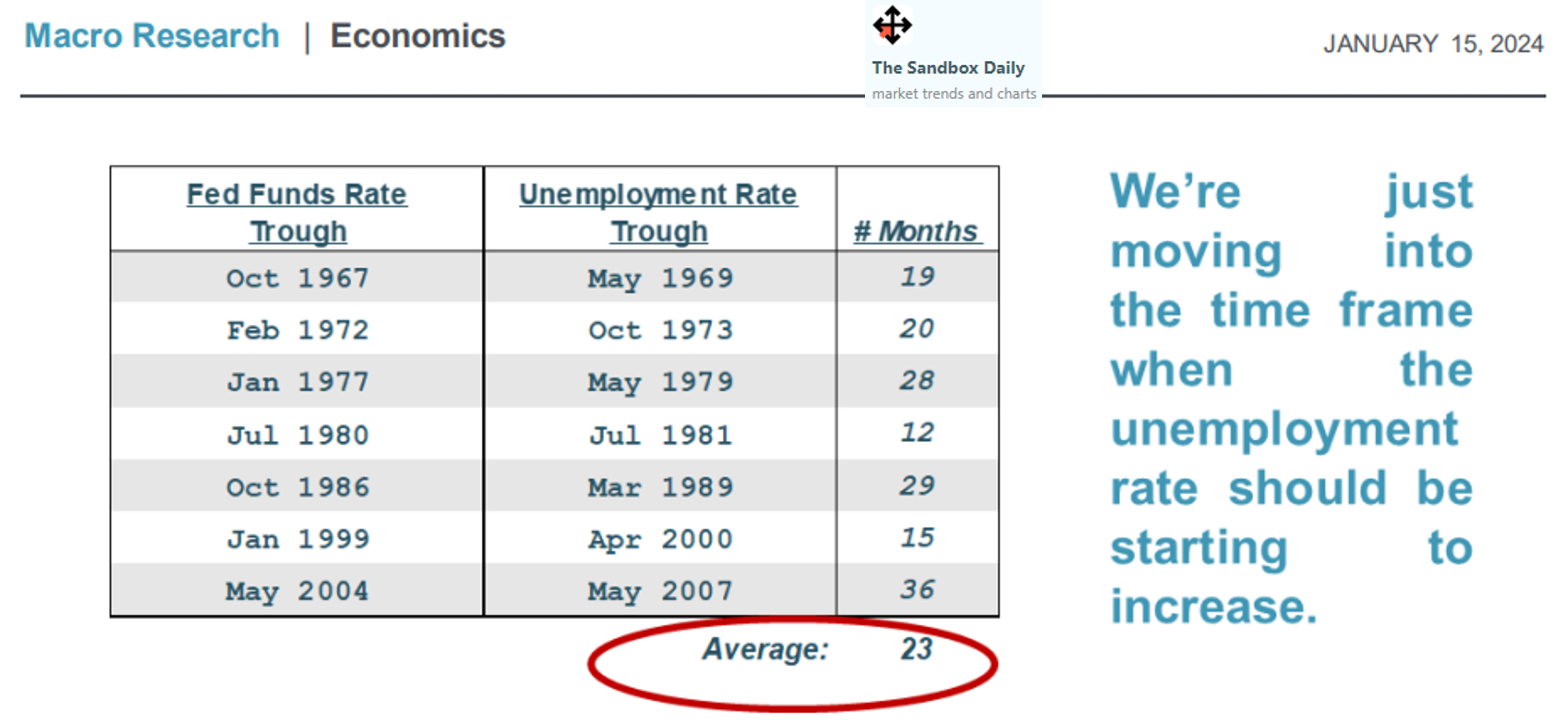

Many continue to ask, “When will we finally see a rise in the unemployment rate?”

Well, Piper Sandler would remind us that the transmission mechanism from Fed tightening to a lift in the unemployment rate, as measured by the troughs in each data series, takes 23 months on average – so the current delay is perfectly normal.

In fact, February 2024 will mark the beginning of the time frame when joblessness “should” start climbing – 23 months after the lows in the Fed Funds Rate in March 2022.

Source: Bob Elliott, Invictus Macro, Ned Davis Research, Piper Sandler

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.