What corporate earnings reveal about tariffs

The Sandbox Daily (7.28.2025)

Welcome, Sandbox friends.

Time to buckle up.

It’s a jam-packed week ahead, with a host of influential companies set to report alongside a Federal Reserve meeting – and, if that wasn’t enough, there’s fresh data on inflation, jobs, and economic growth, too.

Today’s Daily discusses:

What corporate earnings reveal about tariffs

Let’s dig in.

Blake

Markets in review

EQUITIES: Nasdaq 100 +0.36% | S&P 500 +0.02% | Dow -0.14% | Russell 2000 -0.19%

FIXED INCOME: Barclays Agg Bond -0.13% | High Yield -0.05% | 2yr UST 3.931% | 10yr UST 4.414%

COMMODITIES: Brent Crude +2.54% to $70.18/barrel. Gold -0.65% to $3,314.1/oz.

BITCOIN: -0.74% to $118,186

US DOLLAR INDEX: +1.04% to 98.659

CBOE TOTAL PUT/CALL RATIO: 0.91

VIX: +0.67% to 15.03

Quote of the day

“The mind is like a parachute. It only works if it's open.”

- Frank Zappa, Musician

What corporate earnings reveal about tariffs

While investors always look to corporate earnings for clues about how businesses are performing, the current earnings season carries far greater weight than normal due to tariffs.

Although major stock market indices have reached new all-time highs as trade tensions have stabilized, there is still uncertainty as to how tariffs might affect business and consumer activity. Fortunately, new trade agreements are being announced, and corporations are reporting earnings that are beating expectations.

The latest figures show that consumer spending remains healthy and corporate earnings growth continues to exceed expectations.

According to the Yale Budget Lab, consumers face an overall average effective tariff rate of 20.2% as of July 23, the highest level since 1911. The fact that material issues have not appeared in the consumer spending data (yet) suggests that businesses and consumers alike are absorbing the cost of tariffs quite admirably.

Specifically, with just over a third of S&P 500 companies having reported earnings results for the 2nd quarter, 80% have delivered positive earnings-per-share surprises, and the blended earnings growth rate of 6.4% has exceeded expectations of 4.9%, according to FactSet.

While this growth rate is lower than recent quarters, it suggests that an “earnings recession” – ie a sharp drop in corporate profits, such as in 2020 or 2022 – is less likely than originally feared.

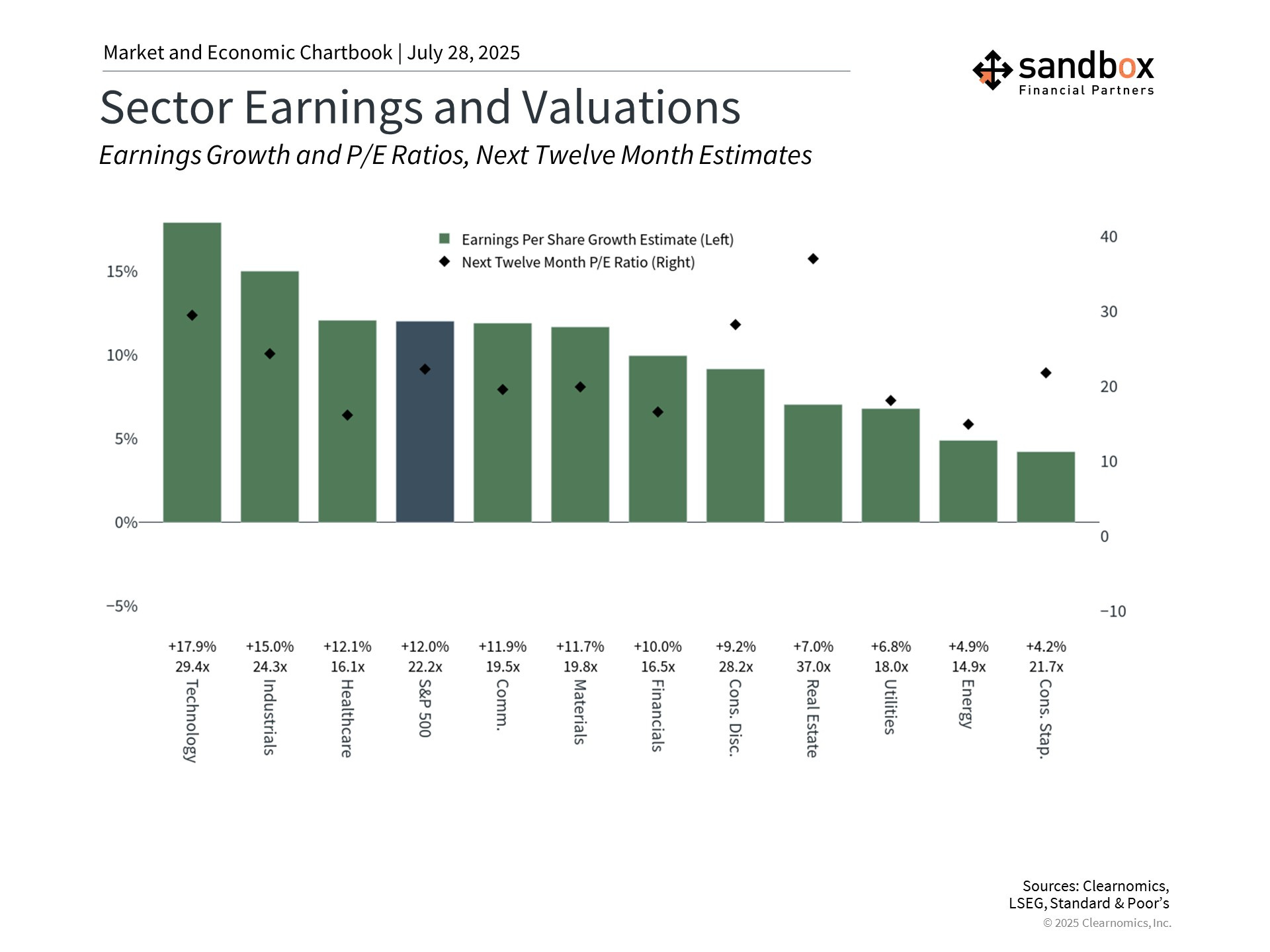

Corporate earnings are holding up so far

How are tariffs paid, and how might they show up in the numbers?

Although tariffs are collected as revenue by the government, the true costs are shouldered by 1) those businesses that export to the United States, 2) U.S. companies themselves, or 3) American consumers in the form of higher prices.

How much each group pays depends in part by how management decides to act but, of even greater importance, is the group’s respective “pricing power.”

For example, the U.S. relies on materials known as “rare earth metals” for electronic devices, nearly all of which are imported. Since there are few alternative sources, any tariffs would likely be passed directly to consumers. This is one reason the administration has sought an agreement that expands imports of rare earth metals with China, and why there is greater interest in domestic production.

In contrast, the automotive industry is highly competitive with both domestic manufacturers and many countries that seek to export their locally-produced vehicles to the U.S. If tariffs are imposed on cars from one country, those manufacturers may choose to absorb some of the costs to remain competitive with vehicles from other nations and domestic producers.

Therefore, the impact of tariffs on earnings, and the response from companies, varies greatly by industry.

For instance, General Motors reported that tariffs cost $1.1 billion in profits during the 2nd quarter, with profit margins falling from 9.0% to 6.1%. On the other hand, Cleveland-Cliffs, a flat-rolled steel maker in the United States, announced better than expected earnings having benefitted from tariffs that reduced steel imports.

The chart below highlights the fact that earnings expectations vary greatly across sectors, partly due to the impact of trade. It will likely take several quarters to understand the full effects of tariffs on companies, especially as trade agreements are announced and evolve.

Several countries have agreed to new arrangements, some with significantly lower tariffs than originally declared on April 2.

In just the last few days it was announced that the European Union and Japan will face 15% tariffs for goods exported to the U.S., while Indonesia and the Philippines will face 19% tariffs. Meanwhile, discussions with China are ongoing this week after earlier developments on a trade truce.

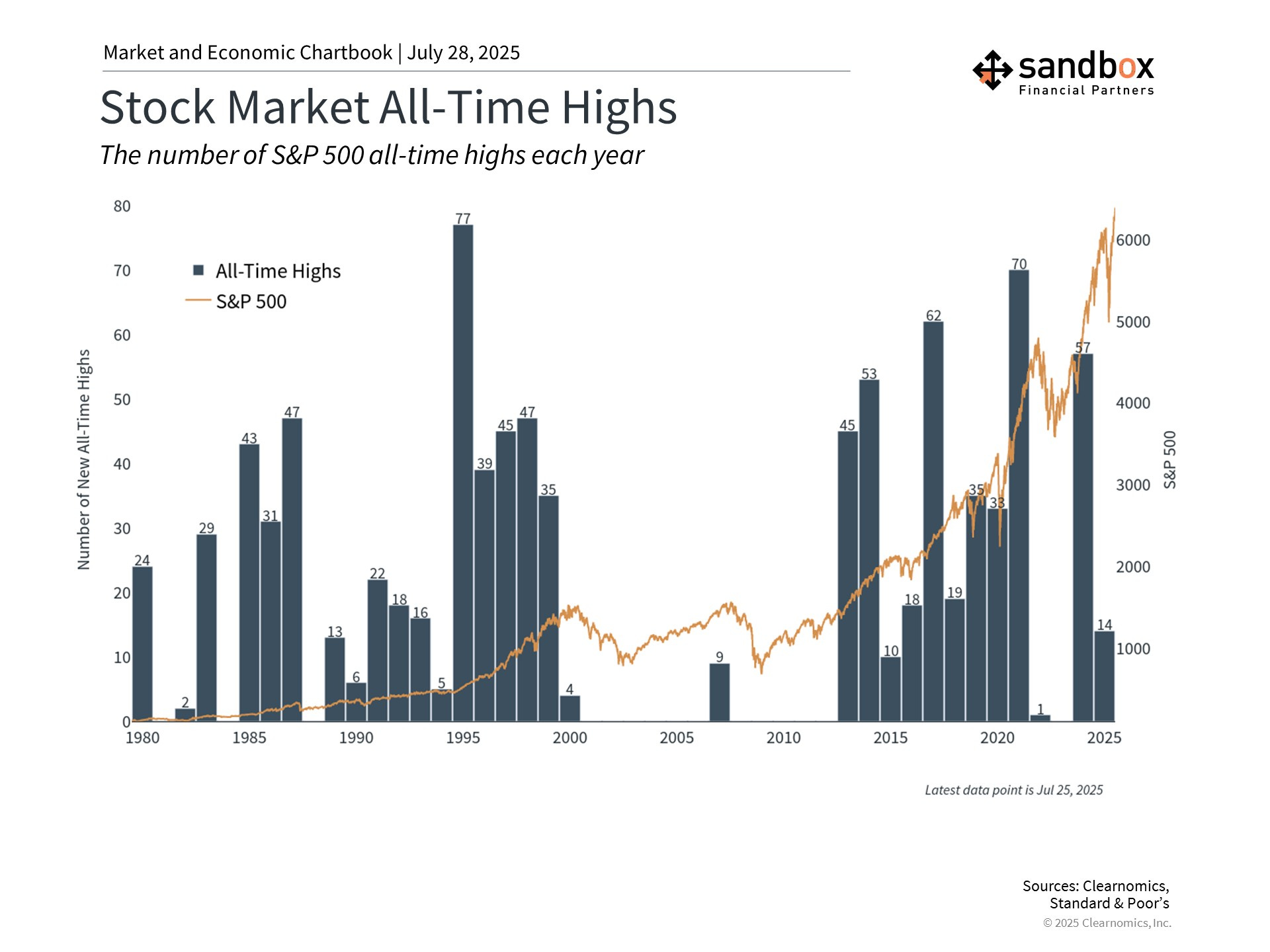

Markets continue to reach new all-time highs

Markets have continued to reach new all-time highs as earnings beats are reported and new trade deals are announced.

As of Friday’s close, the S&P 500 has reached 14 new record highs this year, most of which were achieved in the last month. The Nasdaq has also hit record levels, topping its historic peak from last December, and the Dow is near a new record as well.

Although all-time highs have a habit of making some investors nervous, the reality is that the major averages reach many new all-time highs each year during bull markets.

So, while markets are performing well, concerns about the impact of tariffs on the economy persist.

Some economic forecasts, including those by the Federal Reserve, suggest that inflation could be slightly hotter and growth somewhat slower. The impact on each industry will depend on their input costs, with those that import more facing lower profit margins.

However, these estimates must be weighed against the benefits of domestic investment and the potential for companies to adapt through innovation and greater efficiency.

While tariffs are historically high, what matters more is that they are predictable, since a stable business environment allows companies to adapt their operations and supply chains more effectively.

Looking further out, current Wall Street consensus estimates are for S&P 500 earnings to rise at a 9.6% annual growth rate.

These same forecasts expect an acceleration in growth over the next two years as global trade tensions stabilize and the AI trade is monetized, although much could change between now and then.

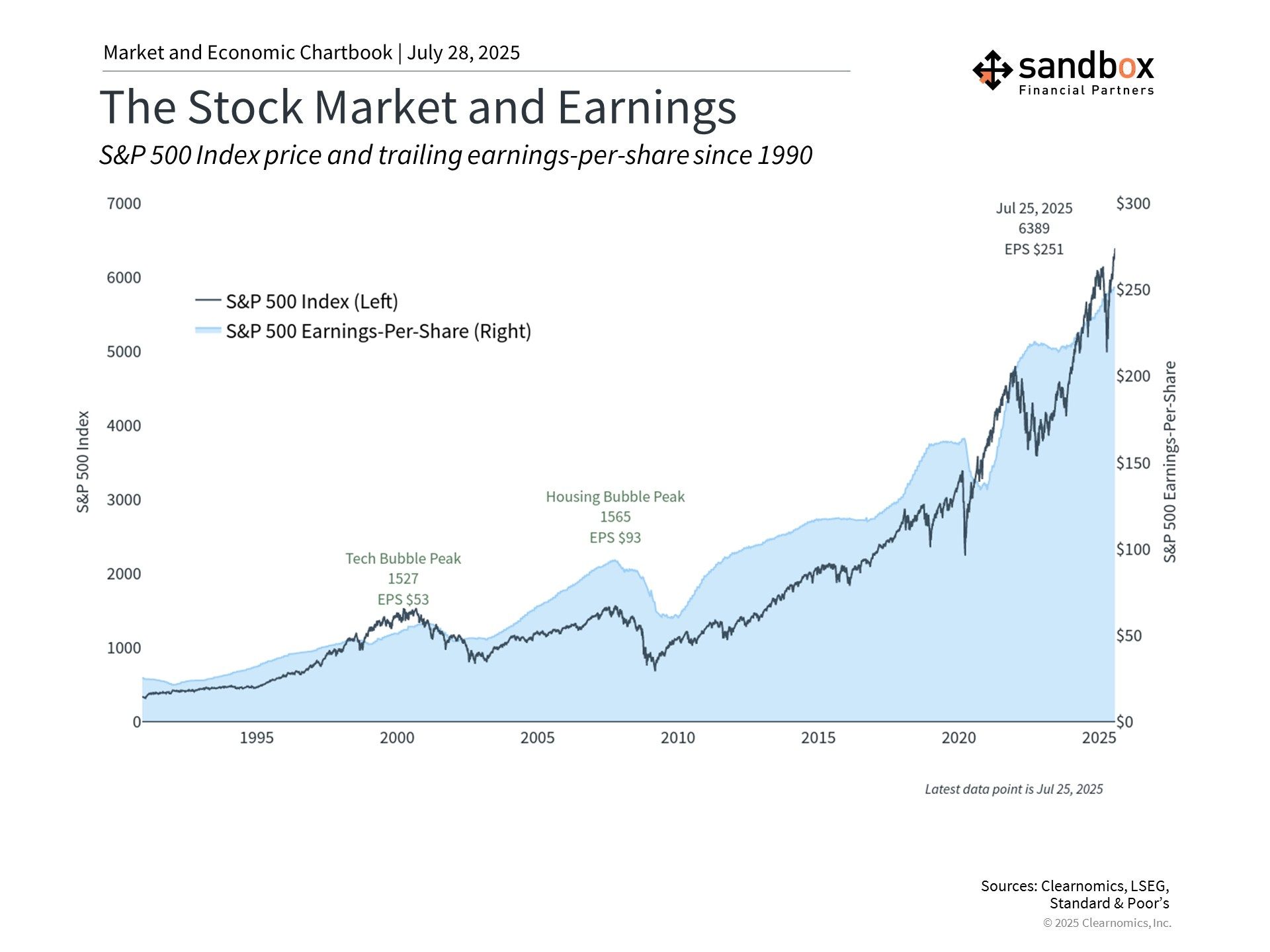

Earnings are an important long-term driver of returns

The stock market tends to follow the path of corporate earnings in the long run.

As shown in the chart below, while price and earnings of the S&P 500 do not line up perfectly, they follow the same broad trends.

This is because economic growth boosts earnings, which in turn pushes stock prices higher. So, while the economy and the stock market are not one and the same, the two are closely related through the performance of companies and their customers.

This is how the impact of tariffs on profits can affect investors.

Whether the stock market is "cheap" or "expensive" depends not just on stock prices but also on corporate performance.

The price-to-earnings ratio, for instance, is simply the price of a stock or index divided by some earnings measure, such as expected earnings over the next twelve months. What this means is that even if prices don't change, increasing earnings will make the market more attractive, and vice versa.

The current S&P 500 price-to-earnings ratio is 22x, well above the historical average of 16x, and is approaching the historic dot-com bubble peak of 24.5x.

Current earnings trends are positive, but whether the stock market continues to be attractive will depend on economic growth and earnings.

Bottom line?

The current earnings season will provide key insights into the effect of tariffs on consumers and businesses.

For investors, understanding these trends – while staying focused on long-term planning – are still the best ways to achieve their financial goals and stay on target.

Source: Josh Schafer, Yale Budget Lab, FactSet, Clearnomics

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures (click here)

Please see our SEC Registered firm brochure (click here)

Please see our SEC Registered Form CRS (click here)