Why I remain constructive on markets here at all-time highs

The Sandbox Daily (3.6.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

10 ideas why markets can move higher from here

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 +0.70% | Nasdaq 100 +0.67% | S&P 500 +0.51% | Dow +0.20%

FIXED INCOME: Barclays Agg Bond +0.15% | High Yield +0.25% | 2yr UST 4.561% | 10yr UST 4.108%

COMMODITIES: Brent Crude +1.05 % to $82.90/barrel. Gold +0.59% to $2,154.6/oz.

BITCOIN: +6.27% to $66,774

US DOLLAR INDEX: -0.41% to 103.376

CBOE EQUITY PUT/CALL RATIO: 0.70

VIX: +0.28% to 14.50

Quote of the day

“It's important to have the ability to zoom out. This really is a superpower. You want to talk about the edge in this market – like, what's your edge? Our edge as market participants is that we can analyze markets along multiple time frames.”

- J.C. Parets, All Start Charts in Monthly Charts Strategy Session

Why I remain constructive on markets early in 2024

Several months ago, on October 16th, I joined Charles Payne on Fox Business to make a simple case: the year-end equity rally was beginning.

In the blink of an eye, the S&P 500 index was up almost 16% into year-end, while the Russell 2000 index had its 4th best 2-month period ever (h/t Ryan Detrick) as yields and the U.S. dollar simultaneously rolled over. Volatility collapsed. Whatever breadth or momentum metric you could think of, it was surging. The floodgates of risk were open wide.

If only we could have accumulated more shares when $SPX was trading at 4300… today it’s higher by 8 sticks at 5100.

Fast forward to late January when the tea leaves, coated in further market upside lacquer, remained ripe to pluck.

I shared some of those bullish sentiments in my Daily note Reasons to support the bull case, as well as the viewers on Charles Payne (again):

The U.S. economy is on stable footing.

Monetary policy is transitioning from aggressive jaw-boning tactics to one of accommodation.

4th quarter 2023 breadth and momentum thrusts cannot be ignored. This is a resilient market with strong undertones of buyers incrementally adding to risk.

Market structure is supportive.

Ok, ok – enough with the pictures !!

So, how am I feeling now after we just bagged 4 consecutive months of market gains?

Is there more juice to squeeze? Has the market run up too much too fast? Will the consumer hang in there? And what about this higher-for-longer narrative?

These are great questions – ones that I hope to address below.

But first…

Each month, I take a full day to step back from the day-to-day operations as the Director of Investments/Portfolio Manager at Sandbox, so I can acutely focus my attention and thoughts on market outlook in the broadest sense possible.

This monthly review process provides clarity for me. What is the highest probability outcome from here? Where are the risks? What do the upside scenarios look like? How are my portfolios positioned?

As J.C. notes in today’s Quote of the Day:

So, with that lengthy setup behind us, let’s discuss some of the reasons why I believe the higher probability outcome from here is higher, using a weight-of-the-evidence approach – even as U.S. stocks are making all-time highs, gold is at all-time highs, bitcoin, Japan, India, the EuroStoxx, etc. etc. And to be absolutely clear, the market can go down – and likely will at some point this spring or summer – because markets don’t move in a straight line.

Equity markets have delivered strong gains and continue to reach new all-time highs in 2024 – while shaking off uncertainty about the Fed’s future trajectory of interest rates. In just 6 weeks, the equity market has resolved higher while pricing out 3 rate cuts. This market isn’t solely reliant on lower yields.

At the heart of the market outlook for 2024 and beyond is whether the market will broaden and in which direction. The current cycle is still young in time and magnitude compared to past cycles, suggesting more room for stocks to dance (see below, top pane). More importantly, just 26% of stocks are beating the index and remains one of the narrowest in history (see below, bottom pane). Taken together, a bullish broadening remains highly plausible.

Market internals remain supportive, part I. When more stocks are advancing than declining, the market is likely to trend higher. After all, you need bulls in a bull market.

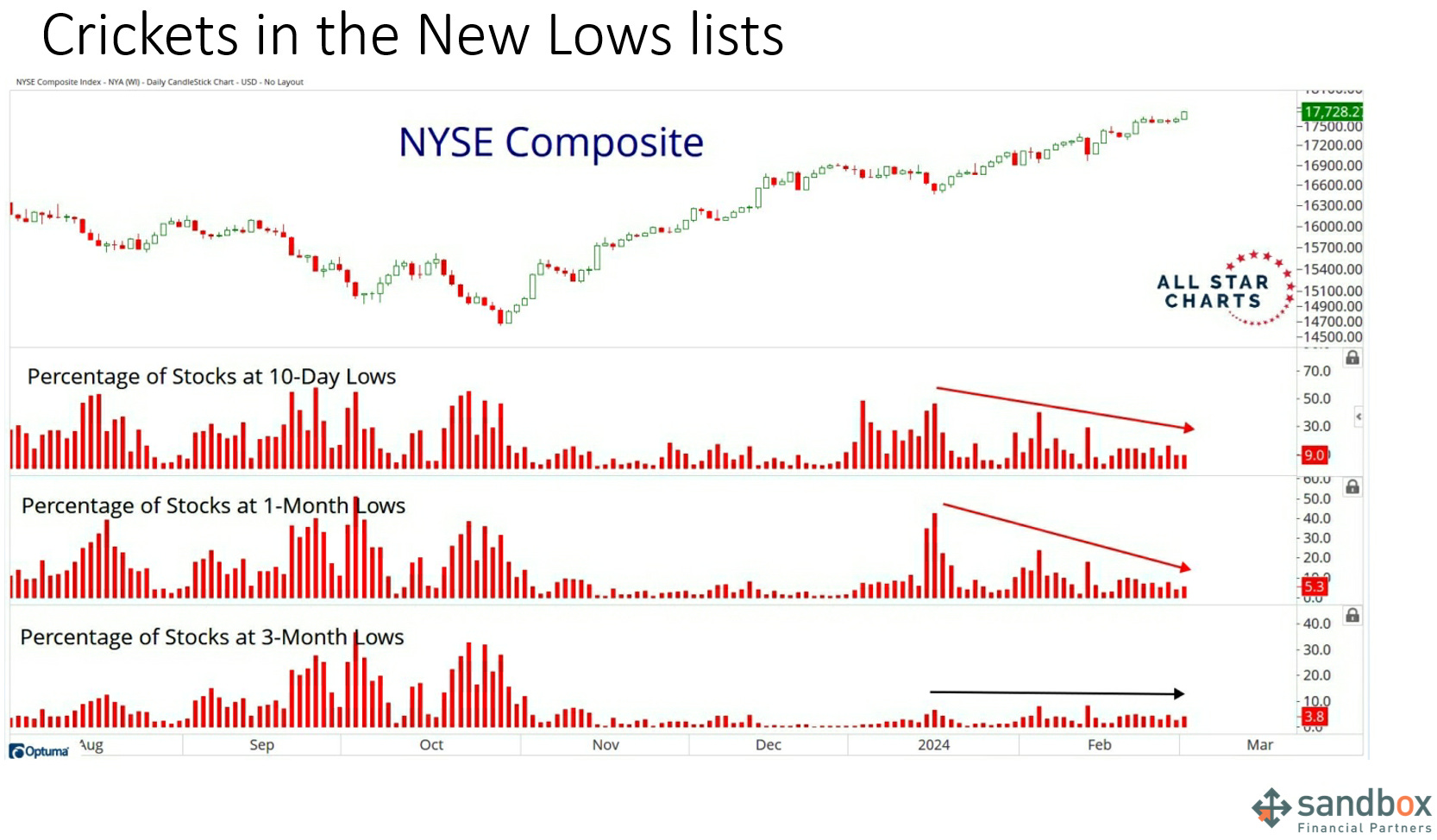

Market internals remain supportive, part II. The most bullish thing I see out there for the stock market is the lack of expansion in New Lows. It's mathematically impossible for the stock market to get worse, go into a correction, or even think about the possibility of a bear market, without seeing an expansion in New Lows first.

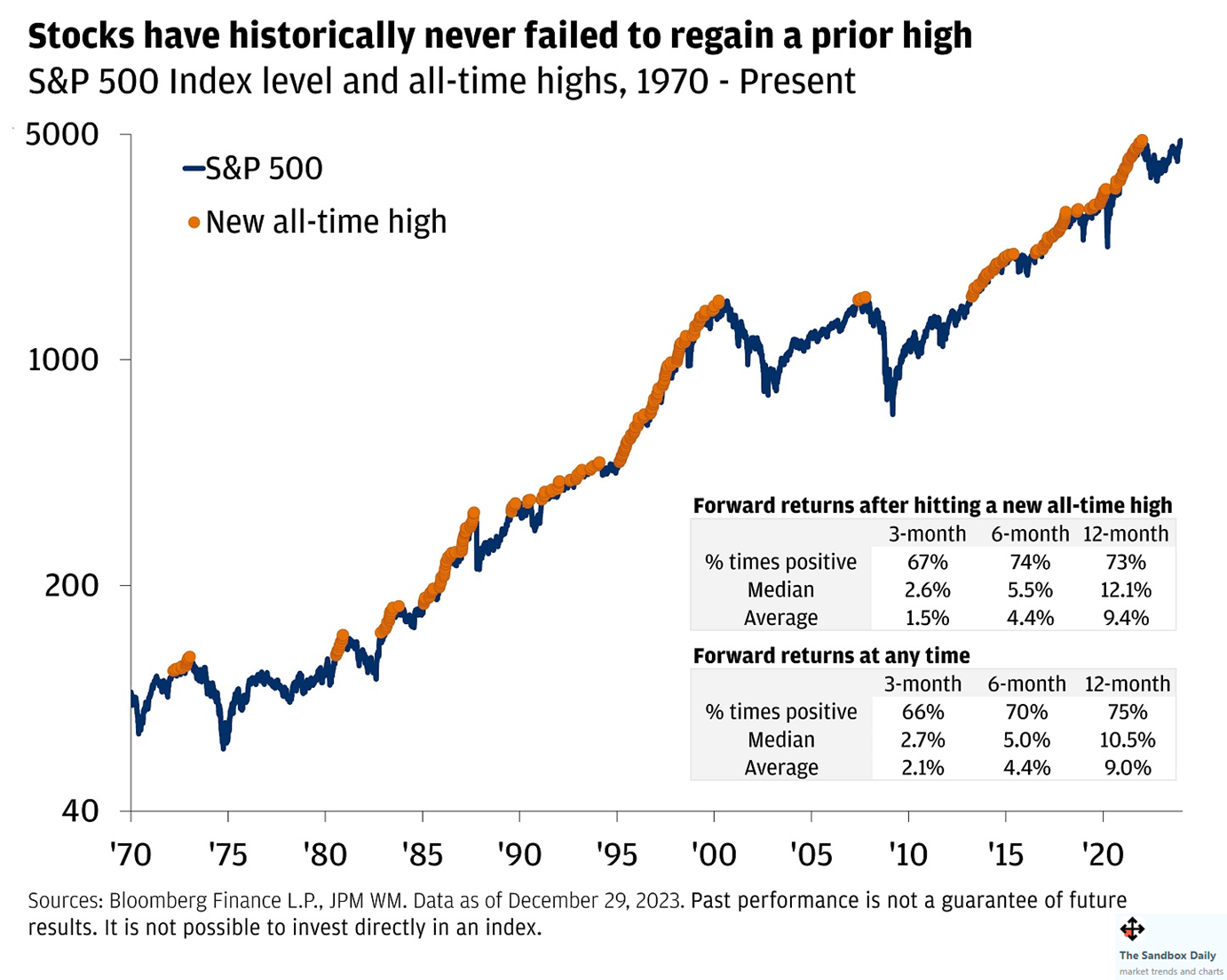

Many investors express a certain anxiety or discomfort holding their positions while the index resides at fresh new highs. What many fail to realize though – until they look at a long-term chart – is that the stock market is often trading at or near all-time highs with some regularity. Over the last 50+ years, had you invested in the S&P 500 at an all-time high, your investment would have been higher a year later 73% of the time with a median return of 12.1%. This is in line with historical market averages – whether we are at all-time highs or not. New highs are not scary.

Roughly 70% of the U.S. economy is personal consumption, so inflation-adjusted income growth matters – big time. With wage growth up and inflation pressures easing, real incomes are growing. As Sonu Varghese of Carson Group notes: “Over the last three months, real incomes excluding transfers (like social security) are running at an annualized pace of 4.2%. For perspective, it was running at 2.6% across 2018-2019.” Bottom line: wages are finally outgrowing inflation.

America's top executives are strikingly more confident about the economy, with expectations of stronger sales and capital investments — plans that indicate the economy should forge ahead in the months ahead. For the 1st time in two years, the Business Roundtable's quarterly gauge of CEO sentiment is above its historical average, signaling that business leaders' economic uneasiness may finally be fading. The C-Suite is finally embracing renewed growth.

The market is going higher without bellwether darling, Apple. This tells me the market has other levers of strength to pull for an advance higher, a bullish development given the size and momentum of passive investors/vehicles that keep piling into this stock.

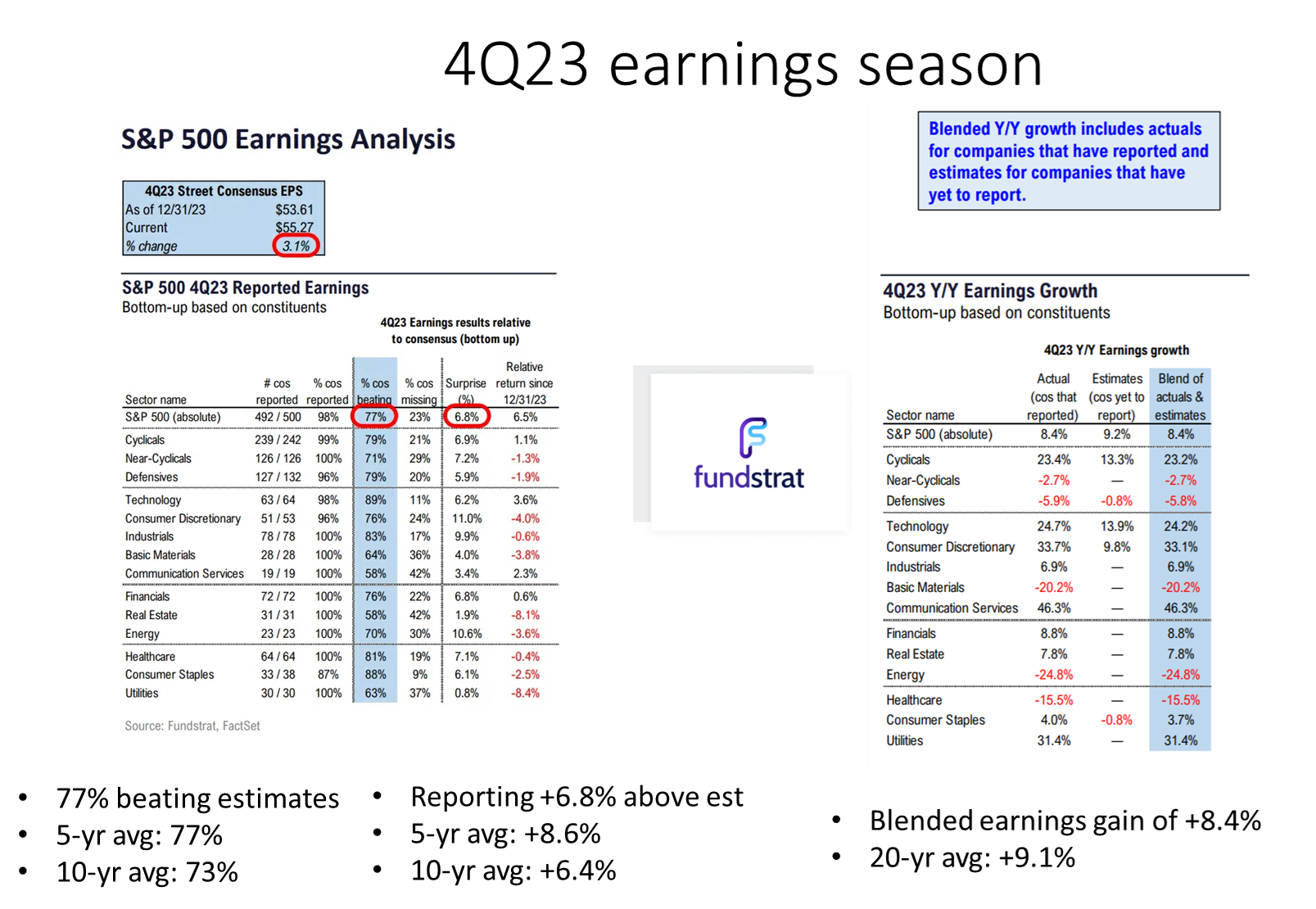

Earnings are at the forefront of the conversation now, following last year’s multiple expansion and a robust – albeit choppy – 4th quarter earnings season. Remember, we are at the stage of the cycle where price usually leads changes in the fundamentals. While valuations are getting stretched, operating margins and bottom-line earnings seem to be heading higher this year and next, which should remain supportive of valuation.

Has the market run up too much too fast? No, at least not according to history. Looking back the prior periods when the S&P 500 was up 20% or more over a 4-month timeframe, forward returns are very favorable – with the S&P 500 index higher 100% of the time over the following 12 months and posting a median gain of +18%.

Sources: Bianco Research, Jurrien Timmer, Larry Thompson (Hostile Charts), J.P Morgan, Carson Group, Axios, All Star Charts, Fundstrat, Dwyer Strategy

Let me know your thoughts and feedback in the comments section below – I’d love to hear what you agree with, and perhaps more importantly, what you don’t agree with.

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.