Why interest rates are defying expectations amid Fed cuts, the election, and more

The Sandbox Daily (11.4.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

interest rates are going up, not down?

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 +0.40% | S&P 500 -0.28% | Nasdaq 100 -0.35% | Dow -0.61%

FIXED INCOME: Barclays Agg Bond +0.42% | High Yield +0.28% | 2yr UST 4.164% | 10yr UST 4.291%

COMMODITIES: Brent Crude +2.71% to $75.08/barrel. Gold -0.07% to $2,744.2/oz.

BITCOIN: -1.08% to $67,936

US DOLLAR INDEX: -0.04% to 103.881

CBOE EQUITY PUT/CALL RATIO: 0.71

VIX: +0.46% to 21.98

Quote of the day

“The lesson you struggle with will repeat itself until you've learned from it.”

- Michael Yardney

Why interest rates are defying expectations

An important, yet counterintuitive, issue for investors is that interest rates have risen in recent weeks despite the Federal Reserve cutting its target interest rate by 0.50% on September 18th.

The 10-year U.S. Treasury yield, for instance, has jumped from a low of 3.63% on September 16 to as high as 4.37%.

This is primarily due to stronger economic data of late and inflation expectations around the election, both of which push longer-term rates higher. Another factor was the bond market front-running the Fed by pricing in too many cuts over the next year.

Unfortunately, a major move like this in the bond market is not an isolated event in recent memory. Over the last five years, rates have swung meaningfully in either direction – causing great anxiety across financial markets.

Looking ahead, one question I often hear is how might uncertainty around interest rates impact investors.

Interest rates affect many parts of our lives, both directly and indirectly.

Households are directly impacted when the cost of borrowing increases, which affects mortgages, credit cards, auto loans, and other consumer-facing loan categories. Many consumers experienced whiplash when borrowing costs jumped suddenly in 2022, after growing accustomed to ultra-low rates over the prior decade. On the flip side, rising interest rates can result in higher yields on bonds, savings accounts, certificates of deposit, money market funds, and more.

When it comes to the broader economy and financial markets, the effects can be more subtle and broad-based. Higher rates increase the “cost of capital” for businesses, which can slow hiring, impede expansion plans, and reduce profitability. For the stock market, rising rates can theoretically reduce the value of future cash flows, reducing stock prices today. Higher rates can also make existing bonds less valuable, since newly issued bonds will offer higher yields. Thus, for investors, interest rates can have wide-ranging effects on portfolios.

What’s driving rates today?

Unlike short-term rates which are influenced primarily by Federal Reserve policy, long-term interest rates are sensitive to economic trends. Fortunately, recent economic figures suggest the economy continues to grow at a steady pace. The latest GDP report showed that the economy grew 2.8% in the third quarter. While this was slightly below expectations, consumer spending remained exceptionally strong. Some economists worry this could reverse as consumers spend down their excess savings and debt levels rise.

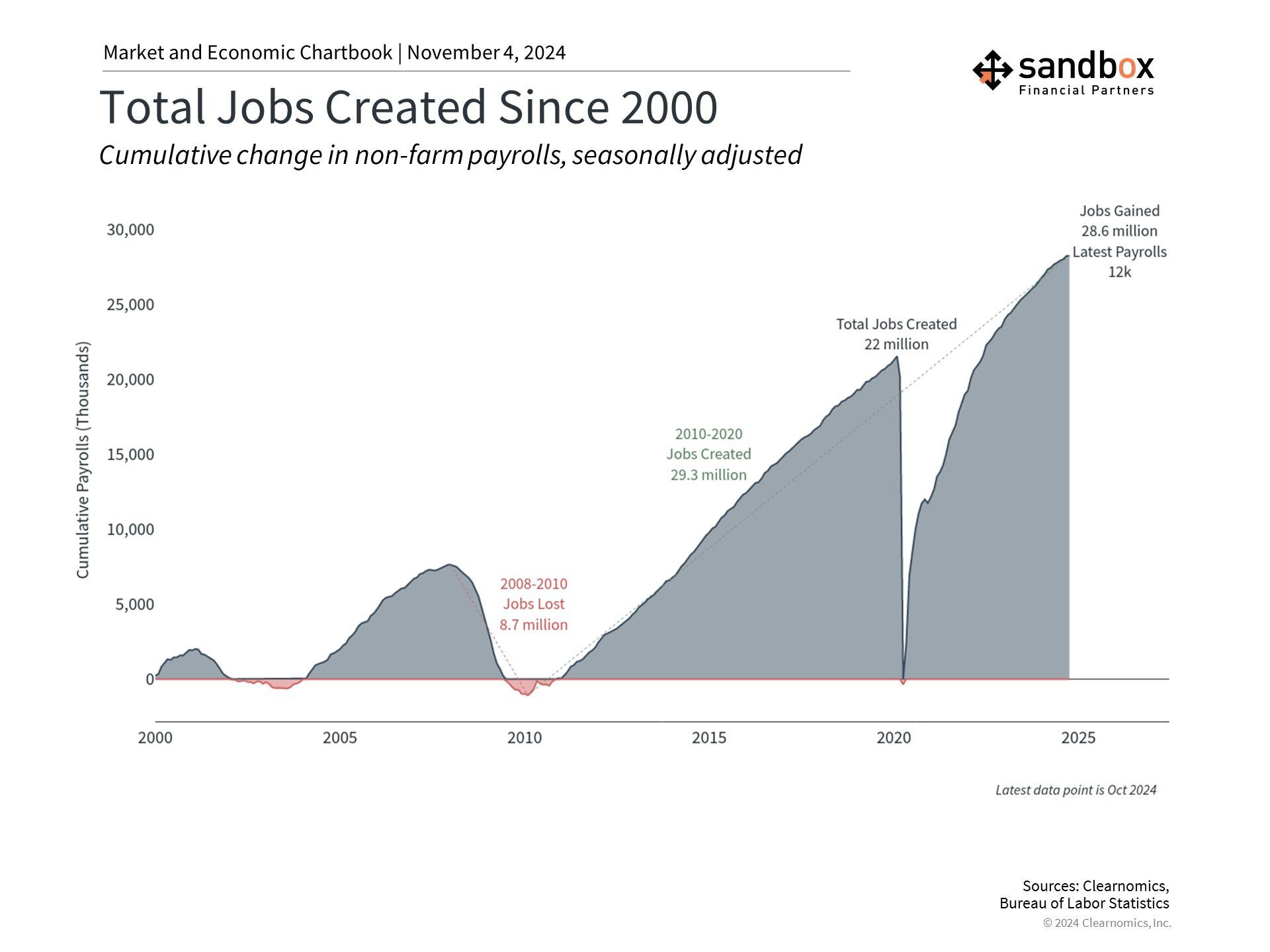

Another key metric investors are watching is the labor market, where recent jobs data has been more mixed.

The jobs report immediately following the Fed’s September rate cut showed that 254,000 jobs were created that month, a blowout figure. This is one reason rates began to rise since a strong job market means the Fed may not need to cut rates as quickly to support the economy. In other words, the Fed could be achieving a so-called “soft landing” even with higher rates.

However, the latest jobs numbers for October show that only 12,000 jobs were added last month – the lowest monthly figure since 2020. There were also significant downward revisions to prior months, lowering the September figure from 254,000 to 223,000. The Bureau of Labor Statistics cited strikes among manufacturing workers and the recent hurricanes in Florida as likely dampeners in the report, although the exact impact is difficult to determine from the survey data. For this reason, the market’s initial reaction was to look beyond this single data point.

The jobs numbers matter because they are of growing importance for Fed decision making. As inflation rates continue to fall back to more normal levels, hiring activity is what will affect households and everyday individuals.

Despite the recent poor data, the reality is that the job market has been exceptionally strong. Not only has the economy added 2.2 million new jobs over the past year, but the unemployment rate is only 4.1%. So, even if the economy does slow from here, it would be from an unusually healthy level.

Thus, rising long-term rates are not unusual if they are due to a stronger economy. In fact, it can be normal for short-term rates to fall as the Fed cuts rates even as long-term rates climb higher. In technical terms, this results in a "steepening yield curve," which typically occurs in the early stages of economic cycles. While it's unclear if this will continue this time, investors should not overreact to these patterns.

Interest rate uncertainty has affected bond prices with the Bloomberg U.S. Aggregate index gaining only 1.4% year-to-date. Returns across sectors this year range from 7.5% for High Yield junk bonds to only 0.8% for Munis. This is because the prices of existing bonds fall as yields rise since newly issued bonds with higher yields become more attractive to investors.

However, these swings have taken place multiple times this year as markets have adjusted to different economic trends. Additionally, many of these bond sectors are offering yields well above their long run averages. The yields on Treasury bonds are 4.3%, well above the 2.0% average since 2009, while Investment Grade corporate bonds are yielding 5.2%.

For all investors, bonds still play an important role in not only diversifying portfolios during periods of uncertainty, but in providing income. As you can see in the chart above, returns by different types of bonds can vary greatly from year to year. While it’s not clear exactly where rates may go next, investors should maintain a longer-term perspective. It’s important to diversify properly across a variety of fixed income sectors to help weather market volatility and avoid concentration in underperforming assets, in the same way equity investors diversify across size, style, and sectors.

Bottom line?

Recent economic data, including a disappointing jobs report, may influence the Fed’s rate cut decisions, but long-term investors should avoid overreacting to a single data point and should instead stay diversified and maintain a longer-term perspective.

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures at the Sandbox Financial Partners website: