Why invest abroad?

The Sandbox Daily (3.18.2026)

Welcome, Sandbox friends.

Today’s Daily discusses:

why invest abroad?

Let’s dig in.

Blake

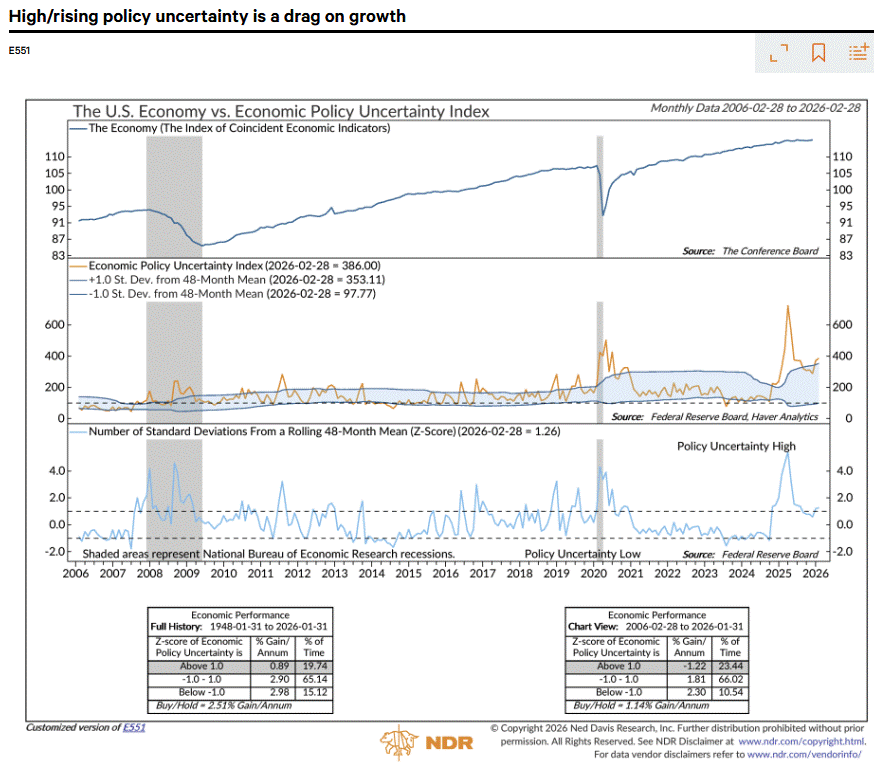

Markets in review

EQUITIES: S&P 500 -1.36% | Nasdaq 100 -1.43% | Dow -1.63% | Russell 2000 -1.64%

FIXED INCOME: Barclays Agg Bond -0.42% | High Yield -0.51% | 2yr UST 3.779% | 10yr UST 4.265%

COMMODITIES: Brent Crude +7.31% to $110.98/barrel. Gold -3.68% to $4,823.9/oz.

BITCOIN: -4.76% to $71,198

US DOLLAR INDEX: +0.62% to 100.192

CBOE TOTAL PUT/CALL RATIO: 1.00

VIX: +12.16% to 25.09

Quote of the day (**hat tip Ryan Detrick for this one)

“I never worry about the problem. I worry about the solution.”

- Shaquille O’Neal

Why invest abroad?

The S&P 500 index has been moving sideways for exactly six months, consolidating gains from recent years and chopping up traders in the meantime. This has led some investors to look abroad for other opportunities.

So, one must ask: what is the bull case for international markets?

A few things come to mind. But first, let’s back up.

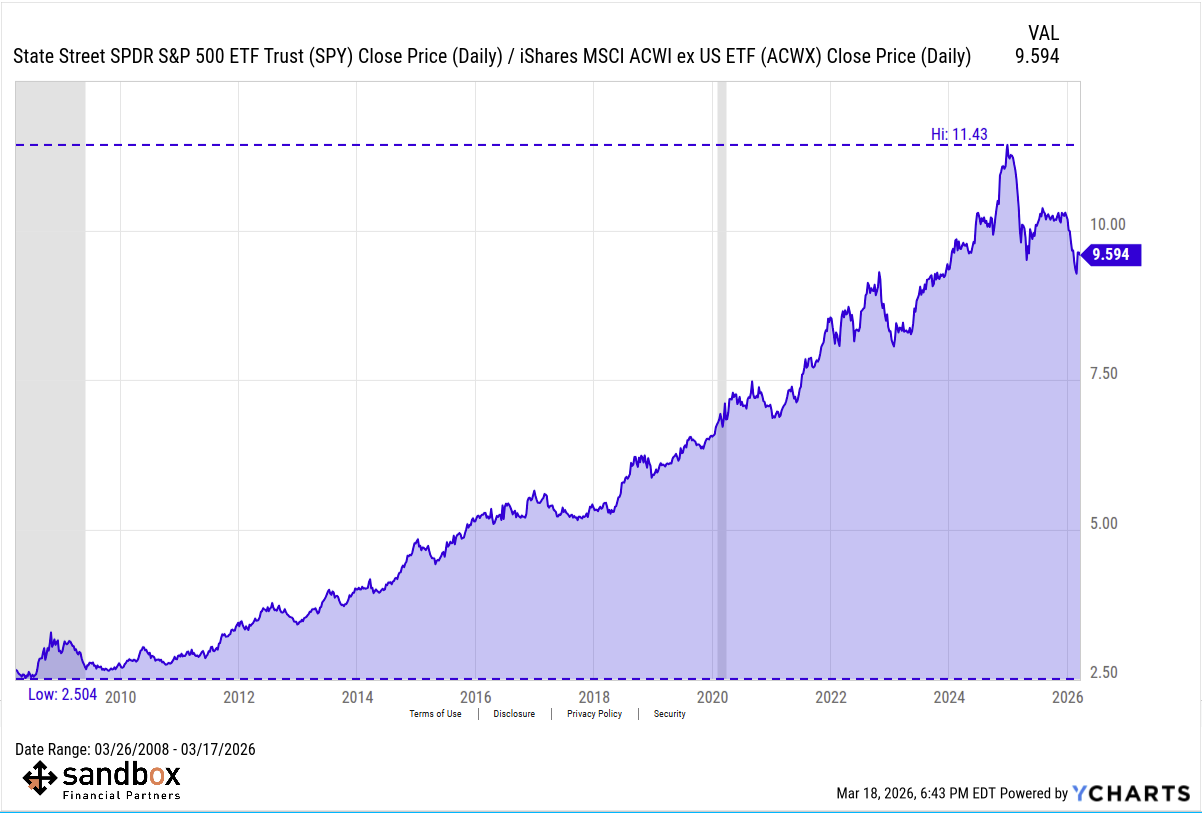

U.S. stocks have dominated international stocks over the past 20-ish years.

This trend reversed abruptly in 2025 (ACWI ex-U.S. +32% vs. S&P 500 +17%) and has continued into 2026, at least until the recent exogenous shock from the Iran conflict.

To believe this longstanding trend is in the midst of a durable trend change in favor of international markets, one likely trusts in some combination of these various tailwinds converging.

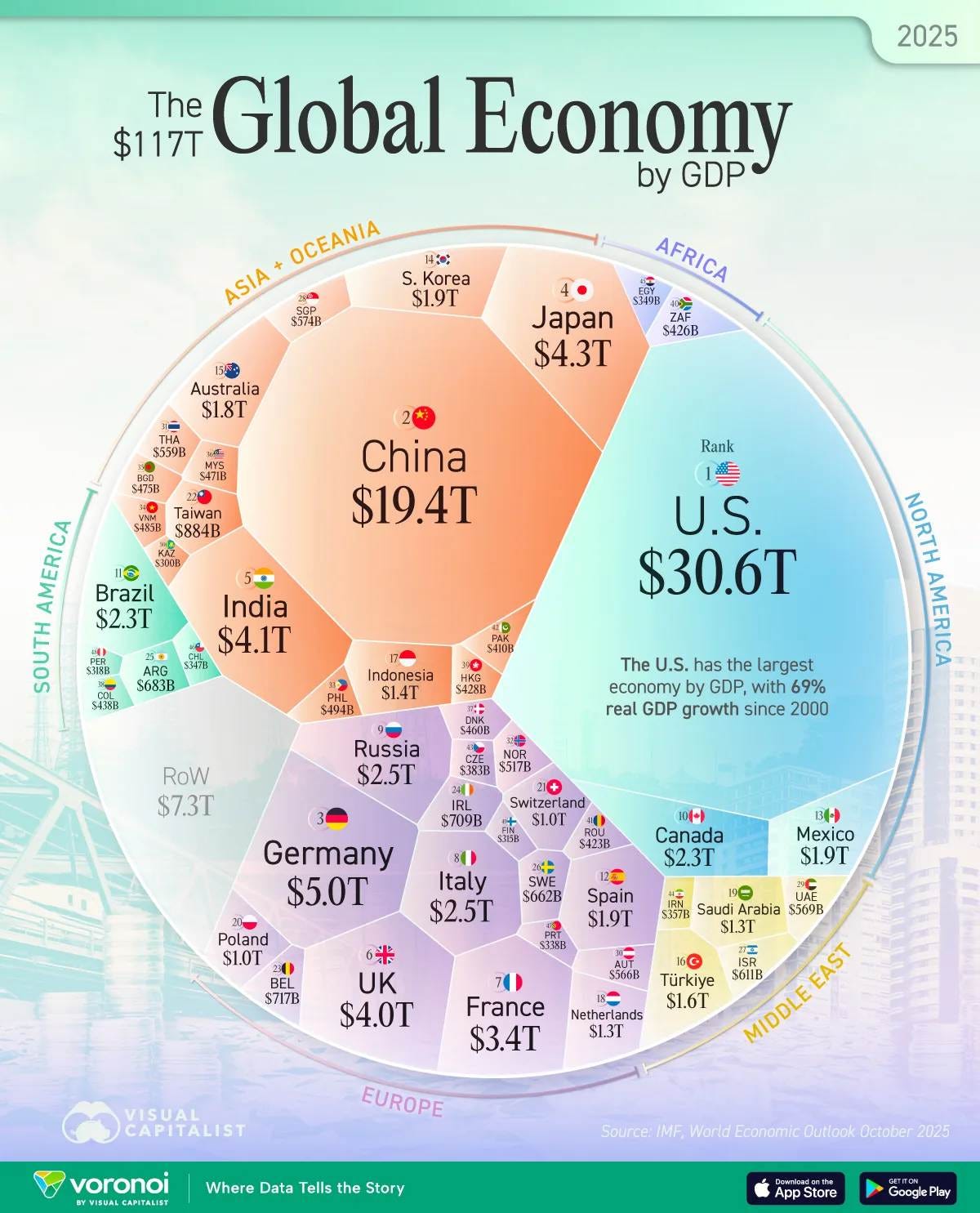

Global growth is broadening

The U.S. now accounts for only ~26% of global GDP, down from ~40% in 1960. In other words, roughly three-quarters of the world’s economic activity is now happening outside the borders of the United States.

EM’s footprint has surged – their share of world GDP jumped from ~25% in 1980 to ~40% today. China alone represents nearly 20% of global output, reflecting how growth engines have shifted towards Asia and other developing economies.

Today, global growth is more balanced. Rising investment and productivity across Europe, Japan, and Emerging Asia have contributed to a more broad-based global growth profile. The Covid-19 pandemic caused countries to focus on protecting domestic supply chains in the interest of national security.

In other words, the United States is no longer the sole growth engine for the global economy.

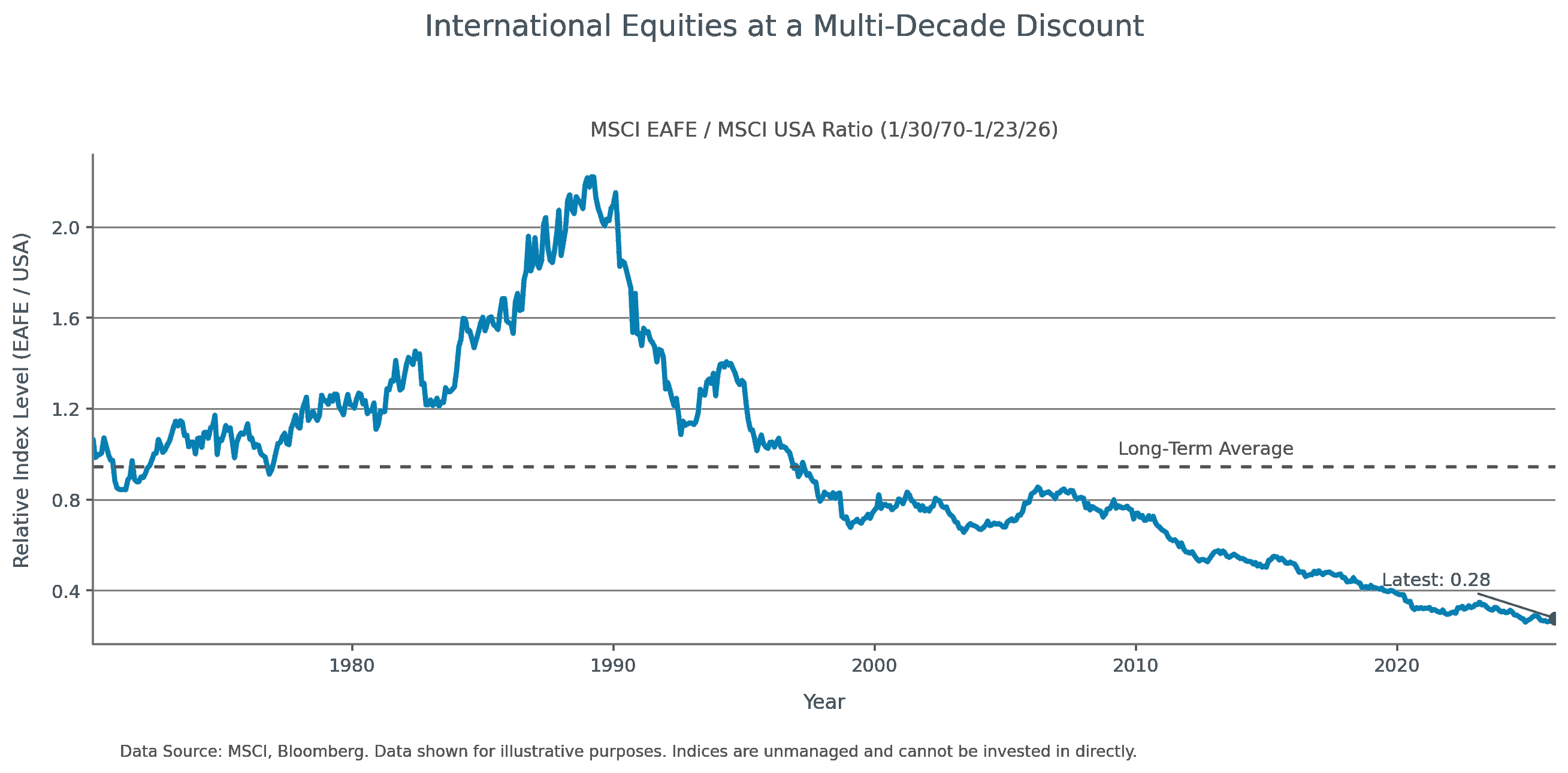

The gap in valuations remains

U.S. stocks are priced for perfection and trade at a hefty premium: international equities trade at a ~30-40% discount relative to U.S. markets, one of the widest gaps in decades.

History shows that after extended runs, leadership often flips – a pattern we may be seeing as valuation extremes and performance trends start to reverse.

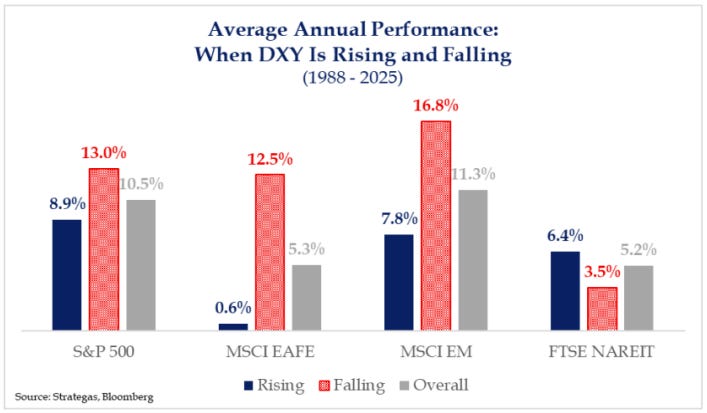

Dollar weakness is a return amplifier

The U.S. Dollar Index (DXY) fell 9.5% in 2025, touching a four-year low. This removed a key headwind for U.S.-based investors abroad as overseas gains now translate into larger USD returns.

Historically, nearly every major run of international outperformance has aligned with a weakening dollar.

This currency tailwind is again evident today, echoing past cycles when a soft dollar helped tilt leadership towards international markets.

Investors are shifting out of the dollar and into hard assets, such as gold, in meaningful ways. A mix of long-term trends and intermediate-term policies suggest prolonged dollar weakness:

excessive debt in the U.S. with no end in sight

U.S. declining share of global growth

a move away from globalization

trade policies, tariffs

further Fed rate cuts

Tariff policy is net dovish on a go-forward basis

The recent SCOTUS ruling striking down Trump’s IEEPA tariffs reduces baseline U.S. tariff levels, creating lower trade barriers for key export economies, particularly emerging markets.

Economies with high past tariffs and significant reliance on U.S. exports stand to benefit, while China and the EU may face more competitive pressures.

Whatever the final policy that is put into place, one thing is certain: reduced uncertainty will benefit stocks, home or abroad.

Is a rebalancing of your global equity exposure warranted in 2026?

Something to monitor closely in the weeks and months ahead.

Sources: YCharts, Visual Capitalist, Bloomberg, Strategas, Ned Davis Research

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures (click here)

Please see our SEC Registered firm brochure (click here)

Please see our SEC Registered Form CRS (click here)