Why markets will be fine after the United States lost its AAA credit rating

The Sandbox Daily (5.19.2025)

Welcome, Sandbox friends.

Today’s Daily discusses:

U.S. loses its final AAA credit rating from Moody’s

Let’s dig in.

Blake

Markets in review

EQUITIES: Dow +0.32% | Nasdaq 100 +0.09% | S&P 500 +0.09% | Russell 2000 -0.42%

FIXED INCOME: Barclays Agg Bond -0.03% | High Yield -0.05% | 2yr UST 3.968% | 10yr UST 4.451%

COMMODITIES: Brent Crude +1.49% to $65.49/barrel. Gold +1.51% to $3,235.4/oz.

BITCOIN: +1.64% to $105,559

US DOLLAR INDEX: -0.73% to 100.355

CBOE TOTAL PUT/CALL RATIO: 0.69

VIX: +5.22% to 18.14

Quote of the day

- Meg Bartelt, CFP, Flow Financial Planning

The U.S. lost its final AAA credit rating

The United States lost its last perfect credit rating on Friday, with Moody’s downgrading the U.S.’ sovereign credit rating one notch from Aaa to Aa1.

The decision – which comes over rising deficits, increased interest payment ratios, and sluggish growth – ends the country’s perfect Moody’s credit rating, in place since 1917.

There are three major credit agencies and Moody’s was the last to cut the United States from the most pristine credit rating available. The others, S&P Global and Fitch, downgraded the U.S. credit profile in 2011 and 2023, respectively.

One valid question to ask: what took Moody’s so long?

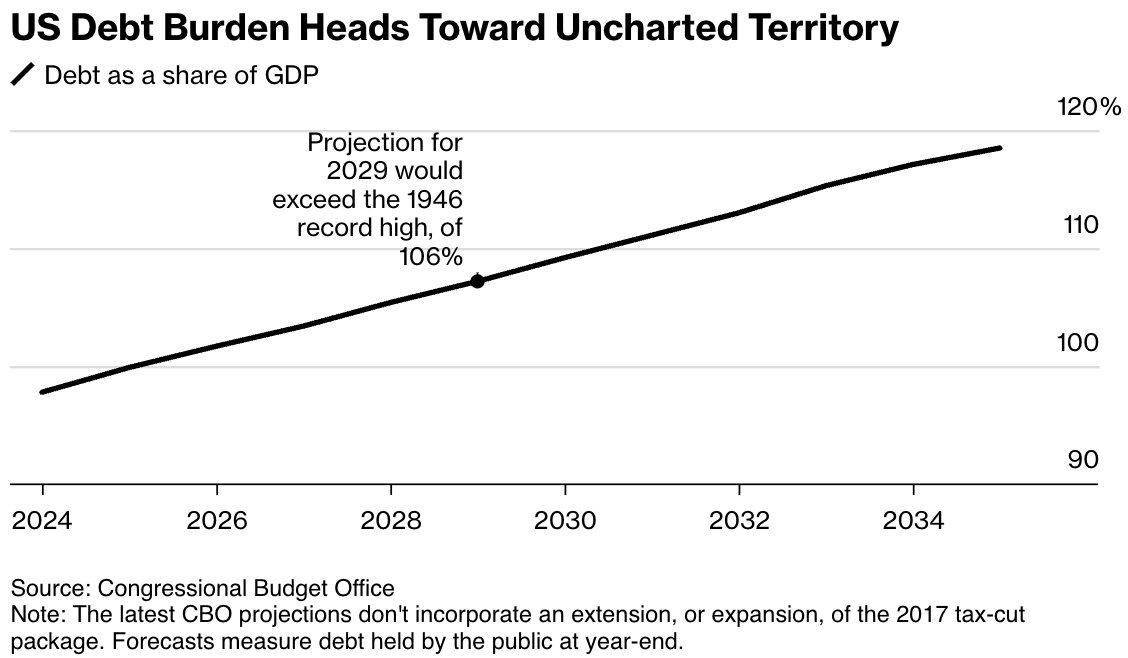

In its report, Moody’s said it expects federal debt to jump from 98% of the U.S. Gross Domestic Product (GDP) last year to 134% by 2035. Also notable, Moody’s stated the decade-plus increase in the deficit and interest payment ratios exceeds metrics from similar countries.

In other words, debt loads/trends are material on a stand-alone basis and a relative basis.

“Successive U.S. administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs,” Moody’s statement reads.

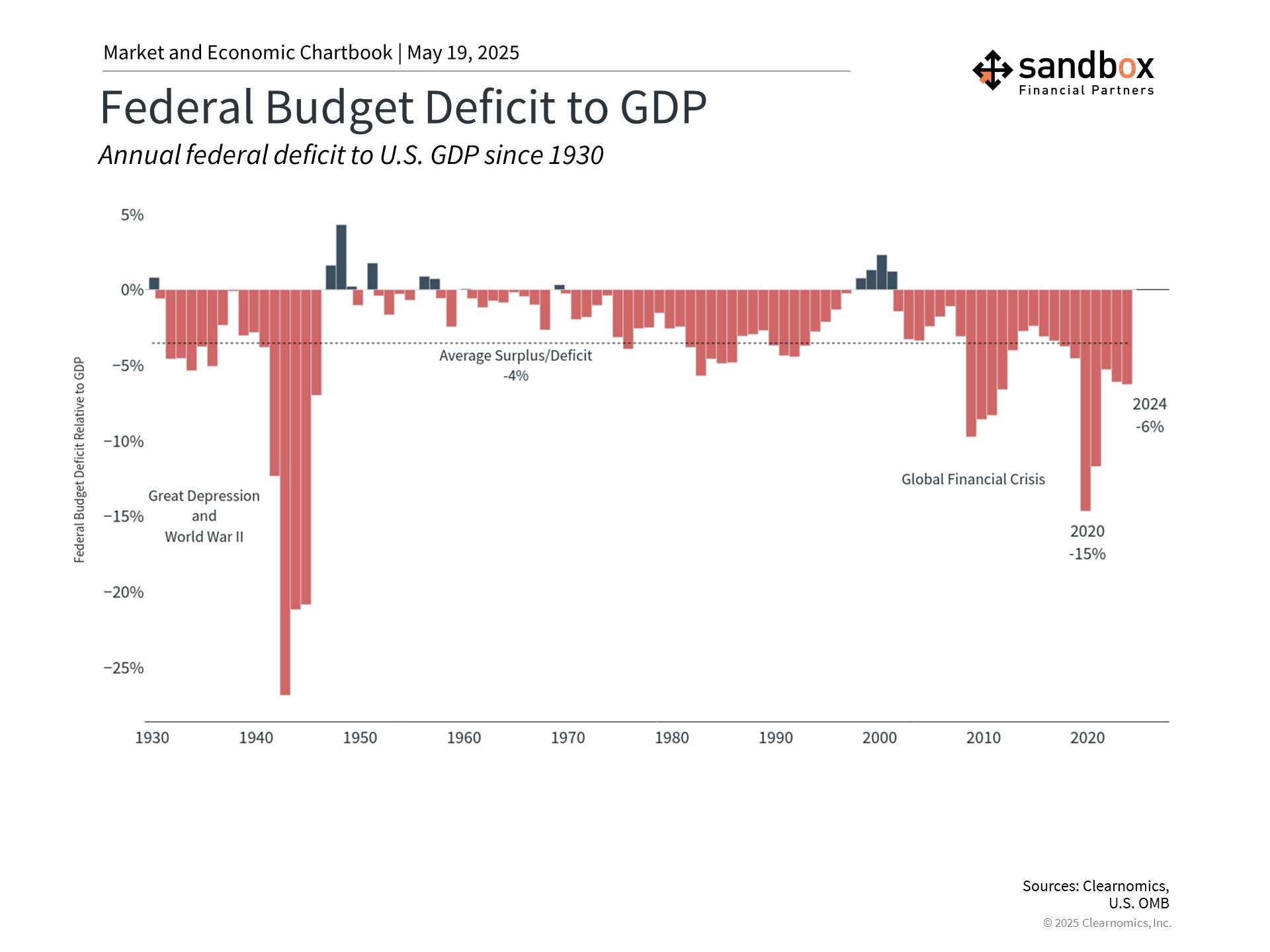

The federal budget deficit is nearing $2 trillion annually – over 6% of GDP – and total debt is now exceeding the size of the entire U.S. economy. The downgrade followed a year of negative outlook and comes at the same time that lawmakers work on a $4 trillion tax-and-spending bill that could add trillions more to the debt.

Many investors came into this trading week expecting some sort of visceral reaction in the markets.

Why?

The S&P 500 fell -6.7% in a single session in August 2011 when Standard & Poor's cut its rating on U.S. debt from AAA to AA+.

In August 2023, the S&P 500 lost -1.4% the day after Fitch's downgrade from AAA to AA+.

Unlike those prior instances, today’s market reaction was muted: while long-dated Treasury yields rose slightly, U.S. equities pared early morning losses to finish the day in the green, with the S&P 500 eeking out a small gain of +0.1%.

Specific to credit markets, the Moody’s decision signals increased risk for U.S. bond investors and could drive borrowing costs higher on the margin as investors may require a higher yield to buy U.S. Treasury debt.

In terms of forced liquidations (due to borrower restrictions that require holding securities of a minimum credit quality), most lending terms / credit agreements / derivative contracts were rewritten after the two previous credit rating downgrades to effectively exclude U.S. government securities. Essentially, U.S. Treasuries are always eligible collateral and the Moody’s downgrade last week won’t put counterparties in violation of covenants or in technical default.

Some were surprised to see the Moody’s downgrade of the U.S. credit profile as a nothingburger.

Jeff deGraaf of RenMac put it best: “This downgrade I’d liken to the 3rd or 5th analyst taking down their estimates or rating on General Electric. It just doesn’t matter at the margin. It’s going to be the 1st or 2nd movers that tend to matter the most.

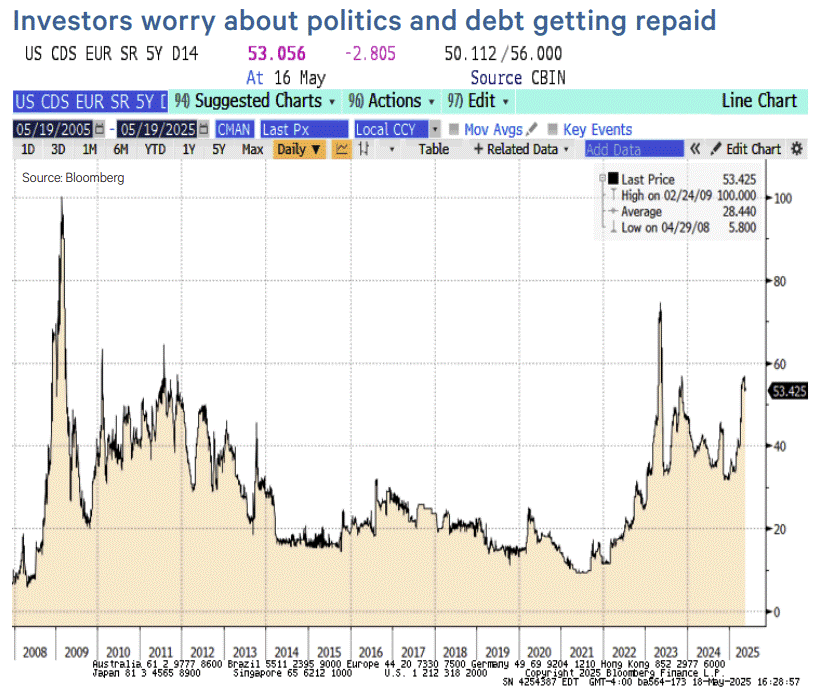

One measure to watch is the credit default swaps (CDS) on U.S. debt – remember those nightmares from 2008 and 2009?

Interestingly, CDS spreads have not improved materially since the first tariff reversal on April 9, suggesting investors are more concerned with the budget than the trade war.

Explore the U.S. deficit here for further information.

Sources: Financial Times, Clearnomics, Bloomberg

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures (click here)

Please see our SEC Registered firm brochure (click here)

Please see our SEC Registered Form CRS (click here)