February jobs report, plus market concentration and weekend sprinkles (a new TSD feature)

The Sandbox Daily (3.8.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

February jobs report

market concentration

weekend sprinkles (a new section for TSD, see below for weekend pleasures)

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 -0.10% | Dow -0.18% | S&P 500 -0.65% | Nasdaq 100 -1.53%

FIXED INCOME: Barclays Agg Bond +0.09% | High Yield +0.03% | 2yr UST 4.478% | 10yr UST 4.077%

COMMODITIES: Brent Crude -1.35% to $81.84/barrel. Gold +0.95% to $2,185.8/oz.

BITCOIN: +1.48% to $67,439

US DOLLAR INDEX: -0.08% to 102.741

CBOE EQUITY PUT/CALL RATIO: 0.56

VIX: +2.08% to 14.74

Quote of the day

“The greatest danger for most of us is not that our aim is too high and we miss it, but that it is too low and we reach it.”

- Michelangelo

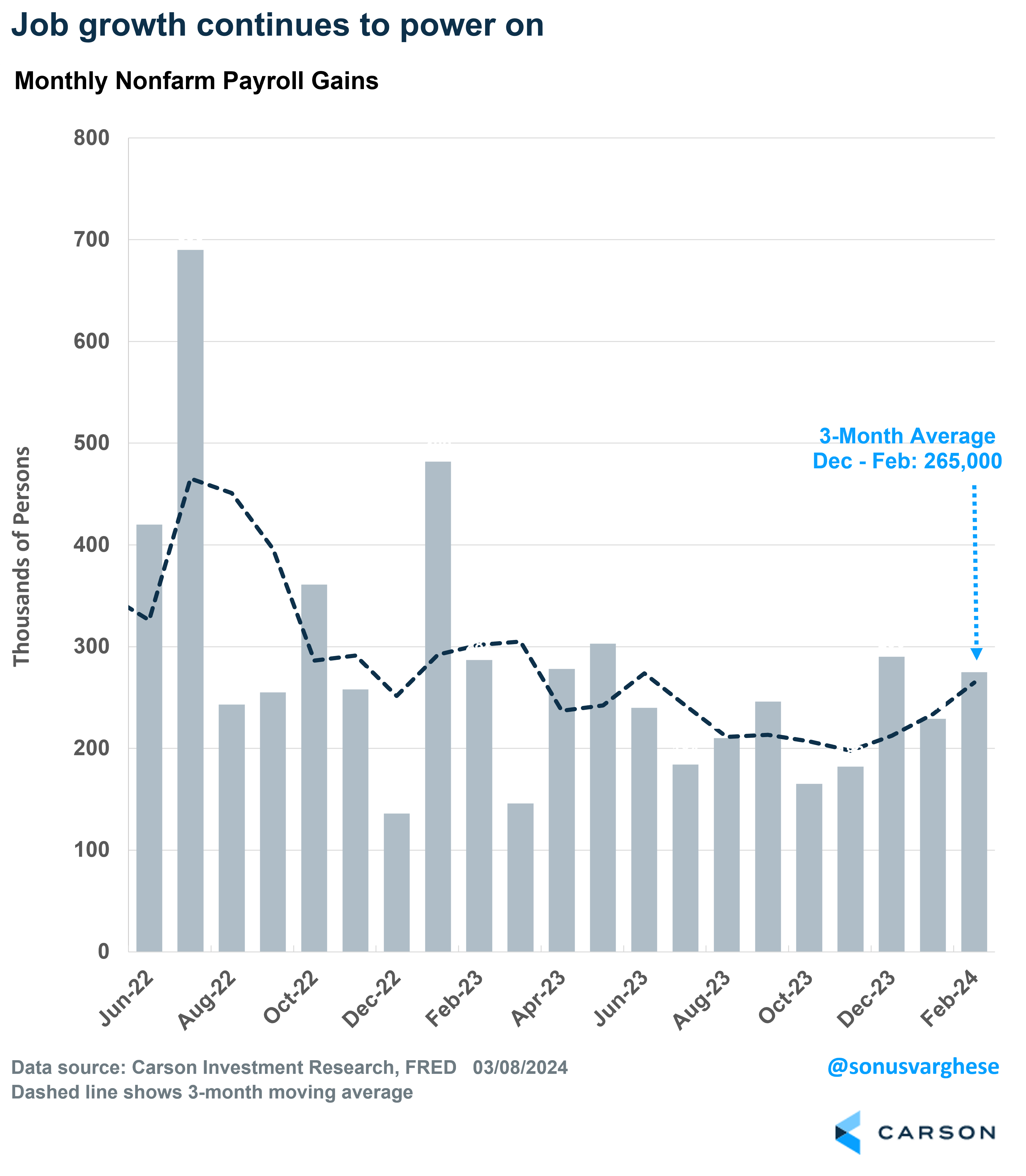

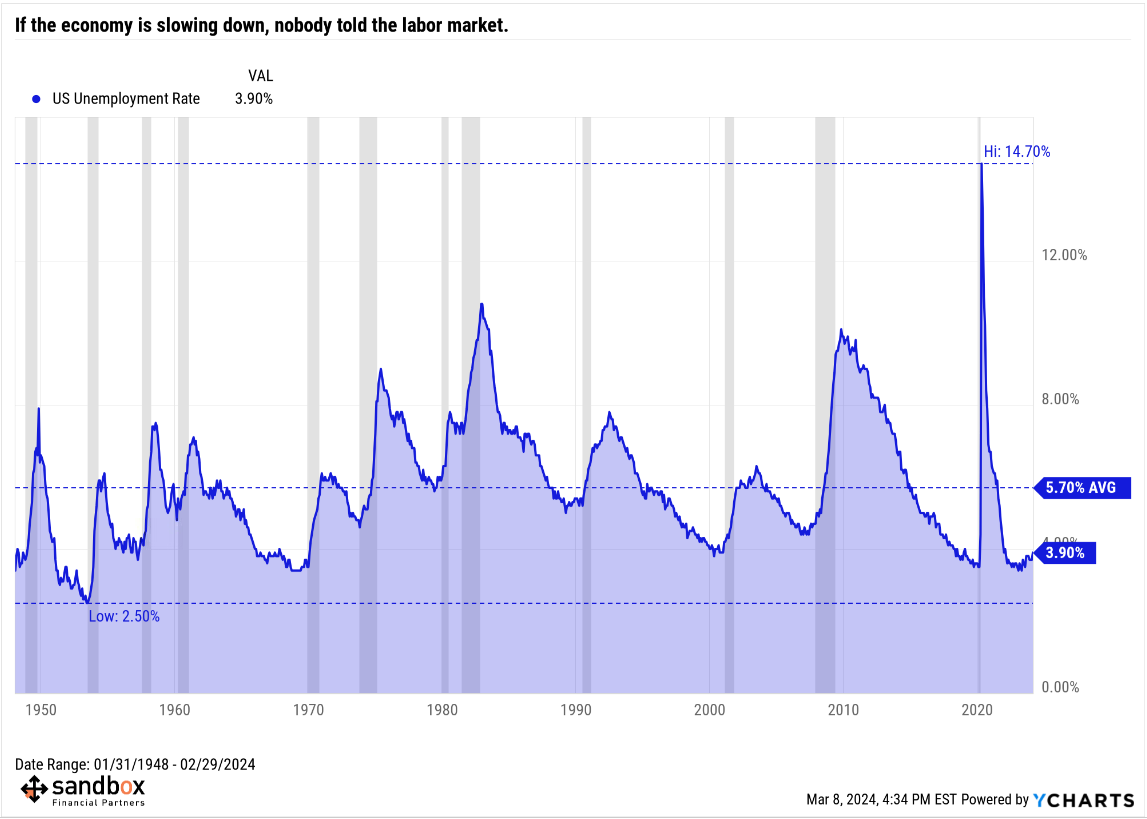

Jobs, jobs, jobs

If the economy is slowing down, nobody told the labor market.

February marked the 38th consecutive month of job gains – the 5th-longest period of employment expansion on record.

Today’s nonfarm payrolls report from the Bureau of Labor Statistics showed U.S. employers added 275,000 jobs in February, well above the consensus of 200,000 and further evidence the bedrock for economic growth remains quite sturdy.

Meanwhile, the prior two months were revised down (again) by a fairly sizable 176k jobs – so keeping track of the 3-month trend (+265k) helps reduce the month-to-month noise and distortions that accompany this jobs report, while also serving a reminder that we are adding jobs well above the pre-pandemic trend.

Meanwhile, the unemployment rate climbed to a 2-year high of 3.9%, which sounds a bit scary on the surface – until we remind ourselves that February marked the 27th consecutive month that the nation’s jobless rate has been at or below 4%, the longest stretch in more than 50 years.

Elsewhere, average hourly earnings, where much of the attention has been focused, slowed to just +0.1% MoM on top of downward revisions to December and January.

This is good news from the perspective of markets. Remember, higher wages increase the prospects of more inflation in the future which puts more pressure on the Fed to maintain their higher-for-longer message – not good for stocks that are expecting cuts as early as this spring summer.

Finally, the cohort in their prime working years (ages 25-54) who are employed relative to the population remains higher than pre-pandemic levels which is quite encouraging.

So that’s a lot of data and information. What does it all mean?

The labor market remains on strong footing, the tightness of the last two years is showing signs of easing, and in regards to markets and portfolios, likely keeps the Fed on track for a rate cut in Q2 (most likely in June).

Source: Ned Davis Research, Piper Sandler, Zero Hedge, Bloomberg, Sonu Varghese (Carson Group), Calculated Risk

Market concentration

The outperformance of the largest stocks has lifted U.S. equity market concentration to the highest level in decades.

Concentration of both market capitalization and earnings in the largest stocks has risen during the past decade and accelerated with the strength of the mega-cap tech stocks during the past year.

The 10 largest stocks now account for 33% of S&P 500 market-cap (well above the 27% share reached at the peak of the Tech Bubble in 2000) and 25% of earnings.

This concentration has helped drive a stretch of exceptionally strong U.S. equity market returns.

The S&P 500 has generated an annualized total return of +16% during the past 5 years, compared with a 30-year annual average of 10%.

The 10 largest stocks – just 2% of S&P 500 companies – have accounted for more than a third of the S&P 500 return in each of these five years. Even including the 36% decline in 2022, an investor who only owned the 10 largest S&P 500 stocks in each of the last five years would have enjoyed a compound annualized return of 20%.

Source: Goldman Sachs Global Investment Research

Weekend sprinkles

Here are some ideas that caught my attention this week – perfect for quiet time reading over the weekend.

Cliffwater – Private Equity’s Second(ary) Act (Phil Huber)

Irrelevant Investor – The fear of missing out (Michael Batnick)

Prime Cuts – How to make your life less hectic (Philip Pearlman)

The Art of Alchemy – How to find your voice (Frederik Gieschen)

Downtown Josh Brown – Adios, Don Julio (Josh Brown)

Discipline Funds – How do higher interest rates push inflation down? (Cullen Roche)

Brown Technical Insights – The Monday Morning Playbook (Scott Brown, CMT)

And here is the fun stuff that got me through the finish line (aka Friday):

Formula 1: Drive to Survive (Netflix)

Kid Cudi feat. Wiz Khalifa – Diamonds Lights Fast Cars (Spotify, Apple Music)

Harry Styles – Daylight (Spotify, Apple Music)

Justin Timberlake – Drown (Spotify, Apple Music)

Kyle Bass burned for blaming $85 room service bill on Biden (New York Post)

If you’re tired of your Steady Eddie steak sauce, try this Bobby Flay bourbon-ancho sauce on for size (assuming you have 1.5 hours to prep) – it’s mouth-wateringly delicious.

Enjoy your weekend sprinkles!

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.