Fed Chair Powell signals ‘time has come’ for September rate cut, plus earnings, strategists, and Babe Ruth

The Sandbox Daily (8.26.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

Fed Chair Powell signals ‘time has come’ for September rate cut

markets follow the direction of earnings

the best strategists

iconic Babe Ruth jersey goes yard with out-of-the-park sales price

Let’s dig in.

Markets in review

EQUITIES: Dow +0.16% | Russell 2000 -0.04% | S&P 500 -0.32% | Nasdaq 100 -1.04%

FIXED INCOME: Barclays Agg Bond -0.09% | High Yield -0.20% | 2yr UST 3.938% | 10yr UST 3.818%

COMMODITIES: Brent Crude +2.73% to $81.18/barrel. Gold +0.29% to $2,553.7/oz.

BITCOIN: -2.18% to $62,723

US DOLLAR INDEX: +0.17% to 100.891

CBOE EQUITY PUT/CALL RATIO: 0.55

VIX: +1.83% to 16.15

Quote of the day

“The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.”

- Jerome Powell, 2024 Jackson Hole Economic Symposium

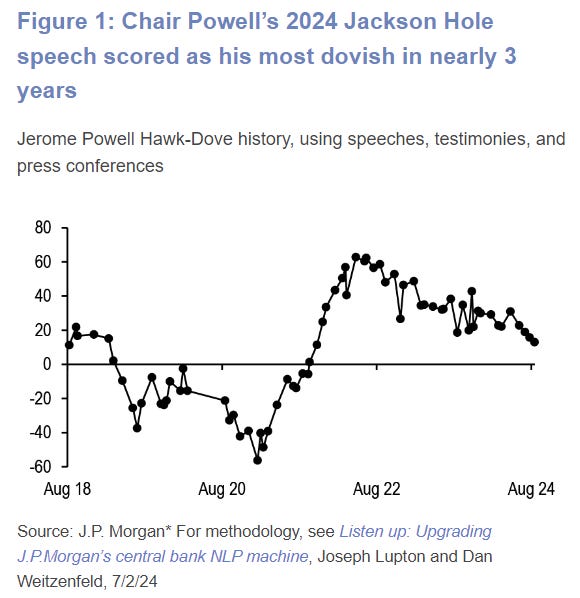

Fed Chair Powell signals ‘time has come’ for September rate cut

Fed Chair Jerome Powell’s remarks last week at the Jackson Hole summit left little doubt that the Federal Reserve will soon be cutting interest rates, as today’s Quote of the Day makes clear crystal clear to Lieutenant Daniel Kaffee and everyone else watching.

Powell didn’t tip his hand on the expected size of the adjustment, instead saying “the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.” While noncommittal on size, this was more open-ended guidance than what we’ve heard from some other Fed officials, who have recently spoken about “methodical” rate cuts.

Overall, Powell’s remarks quite leaned dovish in respect to recent years, as he stressed the FOMC’s attentiveness to labor market conditions. Powell did not express worry about the current state of the labor market, but also offered that the Fed does “not seek or welcome further cooling in the labor market.”

The upcoming inflation (PCE, CPI, PPI) prints matter, but the August jobs report and higher frequency weekly jobless claims will carry greater influence over the magnitude of the first cut that kicks off the upcoming easing cycle.

As Powell noted, “The current level of our policy rate gives us ample room to respond to any risks we may face, including the risk of unwelcome further weakening in labor market conditions.” If the August jobs report validates the July weakness, then the committee should quickly make use of that ample room.

While the labor market headlines stuck out, Powell also expressed growing confidence in inflation returning to 2%. In fact, much of the body of the speech was a retrospective on inflation developments over the past four years. In that, he attributed “much of the increase in inflation to an extraordinary collision between overheated and temporarily distorted demand and constrained supply.”

Earlier last week, the minutes to the July 30-31 FOMC meeting similarly skewed dovish and showed a committee more focused on labor market risks than the possibility of a renewed jump in inflation, even if Fed officials still judged current inflation as somewhat elevated.

Source: J.P. Morgan Markets, Bloomberg, Reuters

Markets follow the direction of earnings

With market volatility subsiding for now, investors have shifted their attention back to fundamentals such as corporate earnings.

Over the course of market cycles, the stock market tends to mirror the trajectory of corporate profits, rising as the economy grows. This is because shares of a stock represents an ownership claim on a company's profits. So, while markets can experience turbulence from time to time, a steadily growing economy and rising corporate profitability have historically fueled the stock market.

As shown below, while markets and earnings do not move in perfect lockstep, they follow similar patterns. The gap between the two accounts for perceived valuation, positioning, and sentiment. Valuations have been expensive in recent years, so market pullbacks can be healthy as investors adjust their expectations.

Over the past twelve months, S&P 500 earnings have risen to $232 per share, a healthy growth rate of 7.4% YoY. This has accelerated with second quarter S&P 500 earnings rising at a blended growth rate of 10.9%, according to FactSet. If these final numbers hold, this will represent the fastest pace since the end of 2021. Earnings began to rebound just over a year ago after struggling in 2022 and early 2023 due to recession concerns.

Source: Clearnomics

The best strategists…

When considering certain attributes or defining characteristics you should expect from your resident market strategist/analyst/trader/reporter, consider this list from Callie Cox of Ritholtz Wealth Management. This is one helluva starting point:

I’d add adaptability to this list.

Markets are dynamic and complex systems. Data points evolve. Trends change. New risks emerge. We cannot hang our hat on any one indicator. At different points of the cycle or calendar year, some indicator types are more critical than others.

The ability to adapt to changing conditions and update our outlooks and recommendations is absolutely essential. We must be open to new ideas and data. A great strategist should demonstrate flexibility and responsiveness to new information in their process. Our assessments and probabilistic outcomes should shift accordingly.

As Jimmy Dean once said: “I can’t change the direction of the wind, but I can adjust my sails to always reach my destination.”

Source: OptimistiCallie

Iconic Babe Ruth jersey goes yard with out-of-the-park sales price

A New York Yankees jersey worn by baseball legend Babe Ruth just became the most expensive sports memorabilia ever sold at auction.

The jersey worn by The Great Bambino when he "called his shot" in Game 3 of the 1932 World Series sold for $24.12 million with Heritage Auctions.

The Yankees won the game 7-5 and swept the Cubs the next day to win the series. This was also Ruth’s last World Series appearance.

The previous record price for any sports collectible sold at auction was for a rare mint condition Topps 1952 Mickey Mantle card, which sold for $12.6 million in 2022.

Below are the most expensive sports memorabilia and collectibles in history.

1932 Babe Ruth ‘Called Shot’ jersey – $24.1 million

1952 Topps Mickey Mantle card – $12.6 million

1998 Michael Jordan NBA Finals Chicago Bulls jersey – $10.1 million

Diego Maradona “Hand of God” jersey – $9.3 million

The Olympic Games Manifesto – $8.8 million

Lionel Messi set of six 2022 World Cup match-worn shirts – $7.8 million

Honus Wagner T-206 Baseball card – $7.25 million

1914 Babe Ruth rookie card – $7.2 million

Muhammad Ali “Rumble in the Jungle” belt – $6.2 million

Kobe Bryant 2007-2008 Lakers jersey – $5.8 million

Source: AP News, Heritage Auctions, ESPN

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.