Forward expectations for U.S. large-cap stocks, plus 2024's calm market, global container prices, and small-caps make history

The Sandbox Daily (7.17.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

P/E ratios and forward equity returns

smooth ride higher for the S&P 500 in 2024

global container prices show renewed pressures on transportation and logistics

history made by small-caps

Let’s dig in.

Markets in review

EQUITIES: Dow +0.59% | Russell 2000 -1.06% | S&P 500 -1.39% | Nasdaq 100 -2.94%

FIXED INCOME: Barclays Agg Bond +0.07% | High Yield -0.11% | 2yr UST 4.436% | 10yr UST 4.159%

COMMODITIES: Brent Crude +1.60% to $85.07/barrel. Gold -0.24% to $2,461.9/oz.

BITCOIN: -0.48% to $64,606

US DOLLAR INDEX: -0.50% to 103.748

CBOE EQUITY PUT/CALL RATIO: 0.49

VIX: +9.78% to 14.48

Quote of the day

“No man ever steps in the same river twice. For it’s not the same river and he’s not the same man.”

- Heraclitus

P/E ratios and equity returns

As the forward S&P 500 multiple approaches 22x, future public equity returns become a bit more of a challenge.

The scattergram below provides a visual representation of the relationship between the market multiple and future returns over the next 12 months and 5 years. The downward sloping line is the linear regression, or line of best fit, showing higher P/Es are associated with lower subsequent returns than lower P/E ratios.

As you can see, market valuations do not impact/explain much about forward market returns over shorter time horizons, but over longer time frames, valuation matters.

Historically, more lofty valuations – i.e. higher P/E multiples – have led to market underperformance.

The one caveat here is that valuation is a terrible timing tool, as stocks tend to move above or below fair value regularly and can stay overbought/oversold for long periods of time.

Source: J.P. Morgan Guide to the Markets, The Daily Shot

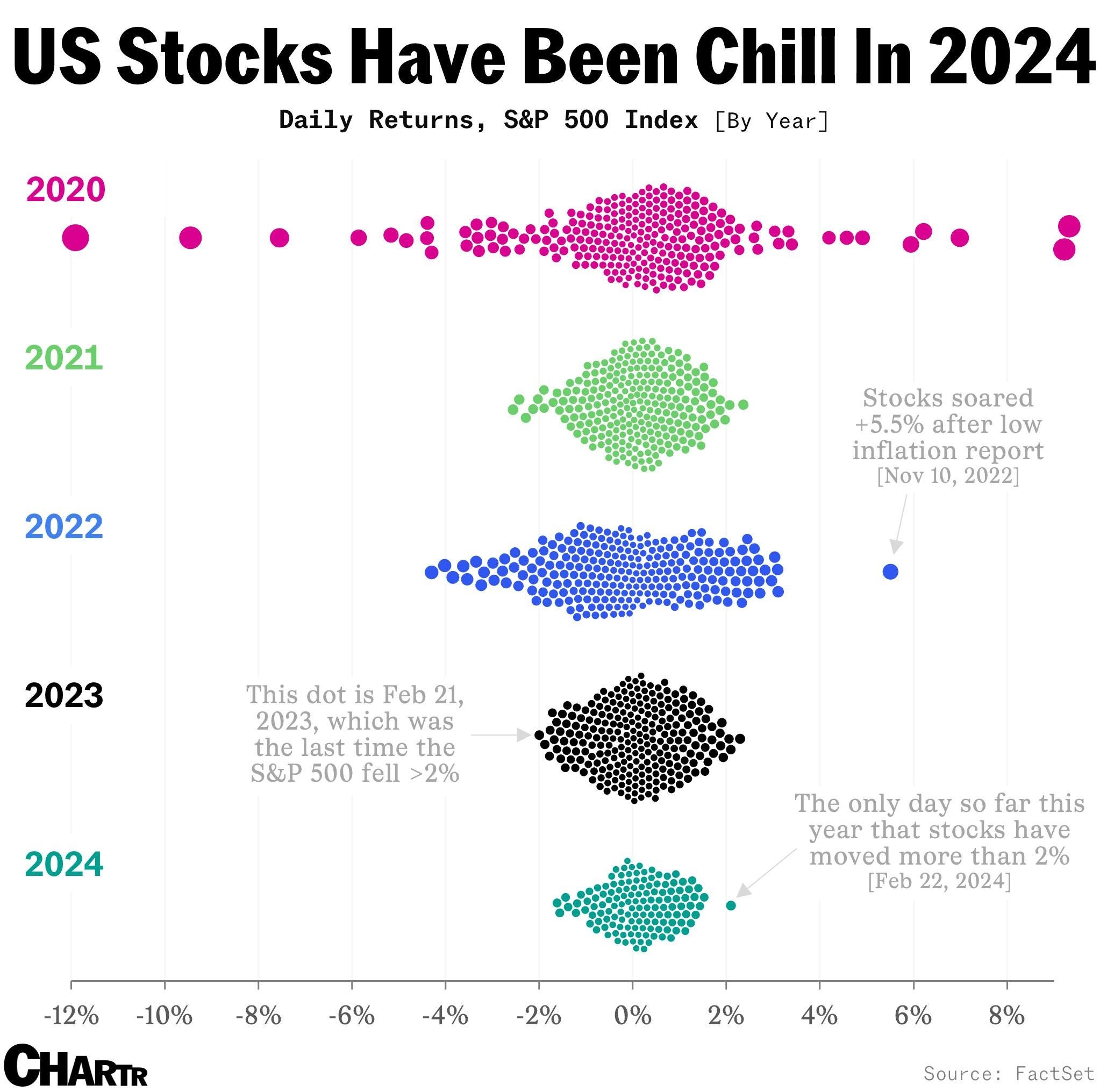

Smooth ride higher for the S&P 500 in 2024

The S&P 500 index has only moved more or less than 2% once all year, a +2.1% gain back in February.

The last time the U.S. large-cap benchmark fell by more than 2% was early 2023, or 512 calendar days ago.

Quiet strength is perfectly normal behavior during bull markets.

Source: Chartr

Global container prices show renewed pressures on transportation and logistics

Freight container prices are moving higher in 2024, up 272% on the year as the price of 40-foot containers reach their highest level since Q4 of 2022, per reporting from J.P. Morgan.

How did we get here?

The global supply chain is a fragile system consisting of numerous links and endless counterparties. Disruption to one can send cascading effects down the chain that needs to function properly and timely for the whole system to work.

The COVID-19 pandemic turned out to be an event of such a magnitude to either bring to halt whole industries and supply chains, or severely reduce their efficiency. Due to its complexity and transcontinental nature, container shipping was hit especially hard by Covid-19. Since the start of the pandemic, the shipping industry has had to struggle with port closures and congestions, labor shortages, difficulties with capacity utilization, as well as a lack of new shipping container stock. But that was 2021’s problem – see the grey line in the chart below.

Fast forward to today’s price surge, the more recent stress on container costs is due to sustained and frequent attacks on vessels in the Red Sea that has stretched capacity in an industry responsible for moving about 80% of all international goods trade, disrupting the normal flow and leading to bottlenecks in some of Asia’s biggest ports. See the red line in the chart above, which looks just like 2021. We provided a more thorough analysis on the Red Sea crisis back in January.

The rise in transportation costs and delay in delivery times are very specific to containers. Freight rates by truck, rail, and air have generally not increased by the same magnitude.

Torsten Slok, Apollo’s Chief Economist, had this takeaway regarding container freight rate implications:

If the global economy was slowing down rapidly, then all transportation costs would be falling. That is not what we are seeing, which suggests that global growth continues to be fine.

Source: J.P. Morgan Markets, Bloomberg, Torsten Slok

History made by small-caps

Yesterday’s close was the most overbought the Russell 2,000 small-cap index has ever been at 4.42 standard deviations above its 50-day moving average.

And that’s not even the best part.

Since 1928 for the S&P large-cap index, 1900 for the Dow Jones, and 1971 for the Nasdaq Composite, none of these benchmarks have ever been more overbought than the Russell is right now.

Source: Bespoke Investment Group, Bianco Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.