Mag 7 gets wrecked, plus S&P 500 returns around 1st cut, active management, and big calls from Tom Lee and Neil Dutta

The Sandbox Daily (7.30.2024)

Welcome, Sandbox friends.

Tom Lee of Fundstrat calls on investors to “buy the fear, high probability of a 4-5% five-day equity rally post-FOMC,” while Neil Dutta of Renaissance Macro Research says the Fed is playing with fire and ought to make a “strong signal cuts are on the way to stabilize labor market conditions.”

Tomorrow, the Federal Open Markets Committee (FOMC) will release their official rate decision statement at 2:00pm followed by Federal Reserve Chair Jerome Powell’s press conference at 2:30pm. The broad consensus is that while rates are likely to remain unchanged, the statement may open the door for rate cuts as early as the next meeting scheduled for September 17-18. Not all market days are important; in fact, most aren’t. But, tomorrow is a BIG day for investors, monetary policy, and the market setup heading into year-end. If there’s just one guiding light we all should follow, it’s “don’t fight the Fed.”

Today’s Daily discusses:

welp, that was fast: tech gets wrecked

S&P 500 return decomposition around the 1st rate cut

active management is hard

commercial real estate maturity wall approaching

Let’s dig in.

Markets in review

EQUITIES: Dow +0.50% | Russell 2000 +0.35% | S&P 500 -0.50% | Nasdaq 100 -1.38%

FIXED INCOME: Barclays Agg Bond +0.10% | High Yield +0.05% | 2yr UST 4.359% | 10yr UST 4.141%

COMMODITIES: Brent Crude -0.81% to $79.13/barrel. Gold +1.27% to $2,456.3/oz.

BITCOIN: -1.67% to $66,002

US DOLLAR INDEX: -0.08% to 104.480

CBOE EQUITY PUT/CALL RATIO: 0.65

VIX: +6.57% to 17.69

Quote of the day

“The biggest communication problem is we do not listen to understand. We listen to reply.”

- Stephen Covey, The 7 Habits of Highly Effective People

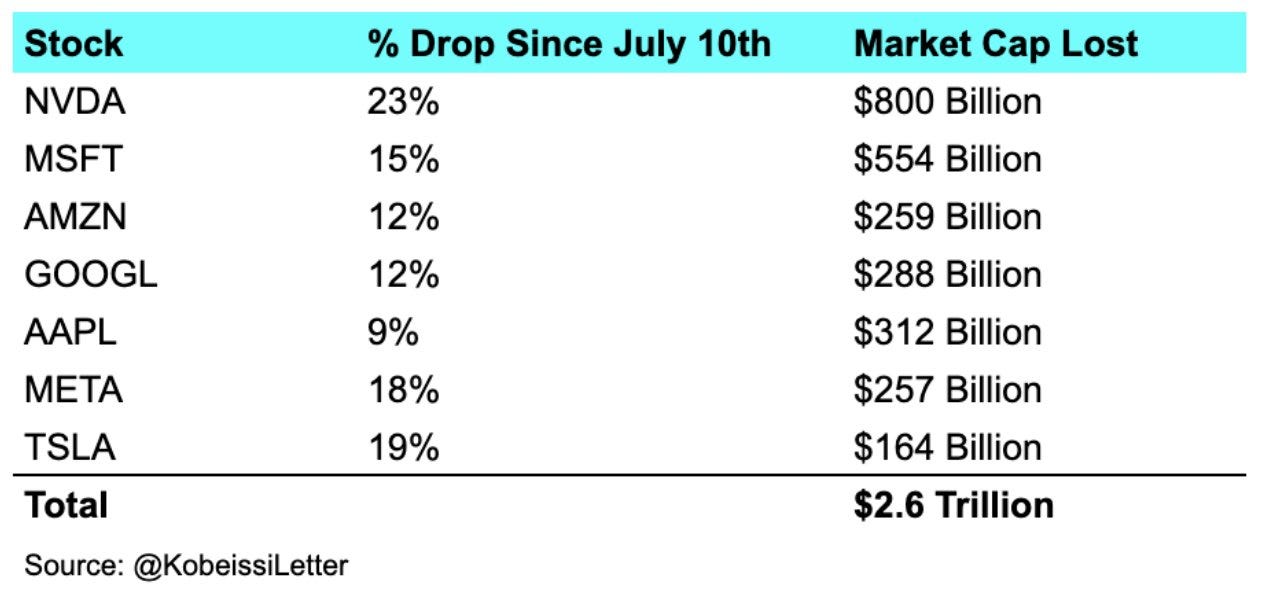

Welp, that was fast

The great summer rotation, as discussed in yesterday’s brief, is quickly stacking up a high body count across mega-cap tech leadership.

The world’s largest technology companies extended their slide on Tuesday, with the Magnificent 7 sinking another 2%.

Nearly half of the Mag 7’s year-to-date gains have evaporated in just three weeks.

“If the Fed does not signal a September rate cut, markets could get a bit ugly given recent tech weakness – especially if earnings underwhelm,” said Tom Essaye at The Sevens Report.

The combined losses for the Magnificent 7 – which is widely held by both institutions and retail, including most American’s 401(k) retirement accounts – are a combined $2.6 trillion.

Source: Mike Zaccardi, CFA, CMT, The Kobeissi Letter

S&P 500 return decomposition around the 1st rate cut

History shows that the S&P 500 return transitions from earnings growth to multiple expansion after the Fed’s 1st rate cut.

Could this happen again even as S&P 500 earnings have begun to accelerate?

The hope of an earnings rebound is one reason the stock market has rallied over the past year, driving up valuations.

Wall Street analysts expect EPS growth of +11% this year, and another +14.0% in 2025 and +12% in 2026.

Source: Ned Davis Research, FactSet

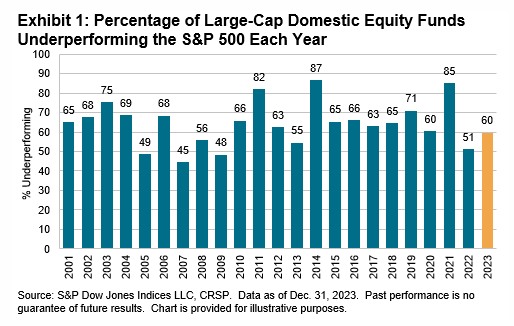

Active management is hard

Each year, the S&P Dow Jones Indices publishes its SPIVA Scorecard that compares actively managed funds against their appropriate benchmarks to better understand the performance of investment managers and illustrate performance across asset classes and styles.

Two common themes have emerged over time:

Actively managed funds have historically tended to underperform their benchmark over short- and long-term time horizons.

Even when a majority of actively managed funds in a category have outperformed the benchmark over one time-period, they have usually failed to outperform over multiple time periods.

Take 2023 for example, which was no different than any other year: 60% of all active large-cap U.S. equity funds underperformed the S&P 500. This was just below the 64% average underperformance rate over the 23-year history of SPIVA Scorecards.

International equities fared even worse, where 74% of funds in the Global category underperformed.

Over in bond land, fixed income results showed an underperformance rate of 59% across all fund categories.

The continued underperformance delivered by active managers further illustrates the challenges of outperforming the market on a consistent basis, as well as the explosive growth of index funds over the past 20-30 years.

Source: S&P Dow Jones Indices

Commercial real estate maturity wall approaching

The U.S. commercial real estate sector has been grappling with fundamental challenges over the past couple years: seismic secular shifts in commercial real estate utilization, diminished credit availability from banks, and high interest rates making debt service more burdensome for borrowers.

Compounding these problems, the commercial real estate debt market is facing a large wave of loan maturities, with many borrowers scheduled to repay a lump sum of principal amidst higher borrowing costs.

The scale of the current maturity wall is large in both absolute and relative terms.

$1.2 trillion of commercial mortgages are scheduled to mature this year and next, barring extensions.

Stated differently, almost a quarter of all outstanding commercial mortgages are maturing in 2024-2025, the highest recorded level going back to 2008.

Banks are the largest holder of this maturing debt, with a 40% share.

The debt market has so far weathered these challenges better than many had expected, for two key reasons.

1st, lenders have worked with borrowers to modify and extend maturing loans that might otherwise go down the path of foreclosure. 2nd, the pressure has largely been concentrated on office properties, with fewer signs of deterioration for other property types.

Source: Goldman Sachs Global Investment Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.