Policy intervention: what to make of the Fed and Trump "puts"

The Sandbox Daily (4.16.2025)

Welcome, Sandbox friends.

Today’s Daily discusses:

policy intervention

Let’s dig in.

Blake

Markets in review

EQUITIES: Russell 2000 -1.03% | Dow -1.73% | S&P 500 -2.24% | Nasdaq 100 -3.04%

FIXED INCOME: Barclays Agg Bond +0.32% | High Yield -0.01% | 2yr UST 3.776% | 10yr UST 4.277%

COMMODITIES: Brent Crude +2.01% to $65.97/barrel. Gold +3.56% to $3,355.8/oz.

BITCOIN: +0.58% to $84,421

US DOLLAR INDEX: -0.93% to 99.286

CBOE TOTAL PUT/CALL RATIO: 1.02

VIX: +8.37% to 32.64

Quote of the day

“Amateurs think about how much money they can make. Professionals think about how much money they could lose.”

- Jack Schwager

Policy intervention

Markets have long operated under the shadow – or perceived safety net – of policy interventions, the so called “put.”

As President Trump’s global trade war upends the status quo, there is a belief that the Federal Reserve or the White House administration, whether in rhetoric or procedure, will step in decisively to prop up markets or stimulate the economy should conditions deteriorate beyond a tipping point.

These institutions have done so in the past, so investors today are wondering where the strike prices for these “puts” are currently placed.

The ramifications of this supposed “put” are anything but trivial. If markets begin to price in intervention as a backstop, it can distort risk premiums, encourage speculative behavior, and skew the natural pricing of assets. More importantly, it blurs the lines between fundamentals and political calculation – raising the stakes for both investors and policymakers.

Fed Puts

Given today’s rather hawkish rhetoric from Federal Reserve Chair Jerome Powell, it would appear the Fed put – as it pertains to interest rate cuts – seems a bit premature at present.

The Fed has already slowed its pace of Quantitative Tightening (QT), reserve balances (i.e. market liquidity) remain abundant, and the labor market continues to demonstrate resilience to the surprise of most.

The Fed put will likely depend on the near-term trajectory of the economy, either through 1) further sustained progress on inflation (now muddied and elongated by the coming tariff price bumps) or 2) the unemployment rate rising enough to have a shortfall in their maximum employment goal.

We know it’s not 4.2%, the current unemployment rate. The latest Summary of Economic Projections (SEP) showed an unemployment rate of 4.4% with two rate cuts. A reading of 4.3% might do the trick, but it could be higher at 4.4% or 4.5%.

Remember, the Fed is usually late than early.

Trump Puts

Although Treasury Secretary Bessent told Tucker Carlson market declines are “more a Mag 7 problem, not a MAGA problem,” it should be no coincidence the S&P 500 index triggered an intra-day bear market correction of -20% the same day President Trump pulled an about-face and issued the 90-day reprieve window on his reciprocal tariffs.

If the tariff pause feels like a lifetime ago, let me remind you the announcement was exactly one week ago today. See below.

The message from the White House shifted from “no negotiation on tariffs” to the “President has maximum leverage to negotiate.”

Bear markets are not healthy, and the administration – full of Wall Street veterans – knows this. As we saw last week, a decline of 20% or more did in fact trigger some moderation in the tariff agenda, so one Trump “put” has effectively been exercised.

What about increased financial stress?

As discussed last week, Trump blinked when it became crystal clear that we were seeing material problems in areas such as funding and safe assets, as well as the liquidity and functioning of the Treasury market and rising Treasury yields.

With marketable Treasury debt exceeding $26 trillion, the bond market is still in charge! As political strategist James Carville said years ago, the bond market can intimidate anyone – even President Trump!

Imagine the conversation Secretary Bessent had in the oval with the President telling him that 10-year yields were rocketing higher, not collapsing, and that the Treasury market was no longer functioning smoothly. This suggests a second Trump “put” was also exercised last week.

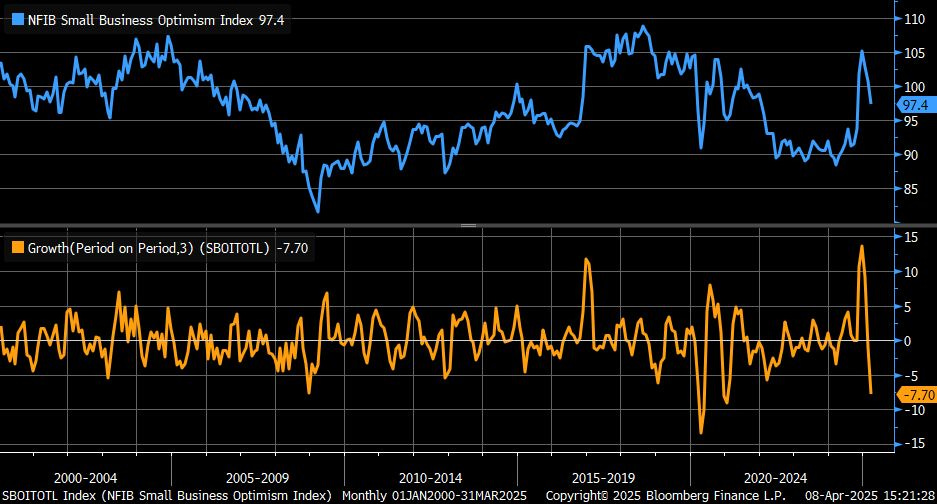

The third and final Trump “put” rests on the shoulders of small business owners, core to President Trump and his MAGA movement.

The NFIB Small Business Optimism Index retreated for the third consecutive month in March, retracing 2/3rds of its post-election rise before the tariff announcement. The Index may have well erased all its post-election rise and then some if the survey were retaken today.

This survey matters because it reflects the sentiment of a significant portion of Trump’s base, as well as Main Street across America. With one eye always open to the next election cycle, Trump and the Republican leadership are wise to heed the concerns of their party’s base.

With some varying measures of “puts” already exercised, investors are looking for the next signals from the Federal Reserve or the White House on further measures of policy relief.

Maybe they come, maybe they don’t.

We’re not out of the woods. In fact, it’s hard to even find the tree line.

Sources: Federal Reserve, J.P Morgan Markets, Truth Social, Bloomberg, Ned Davis Research

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures at the Sandbox Financial Partners website: