Private Credit feeling blue

The Sandbox Daily (3.3.2026)

Welcome, Sandbox friends.

Today’s Daily discusses:

Private Credit feeling blue

Let’s dig in.

Blake

Markets in review

EQUITIES: Dow -0.83% | S&P 500 -0.94% | Nasdaq 100 -1.09% | Russell 2000 -1.79%

FIXED INCOME: Barclays Agg Bond -0.11% | High Yield -0.20% | 2yr UST 3.510% | 10yr UST 4.059%

COMMODITIES: Brent Crude +5.31% to $81.87/barrel. Gold -4.03% to $5,097.4/oz.

BITCOIN: -1.26% to $68,064

US DOLLAR INDEX: +0.70% to 99.07

CBOE TOTAL PUT/CALL RATIO: 0.94

VIX: +9.93% to 23.57

Quote of the day

“The stock market is never obvious. It is designed to fool most people, most of the time.”

- Jesse Livermore

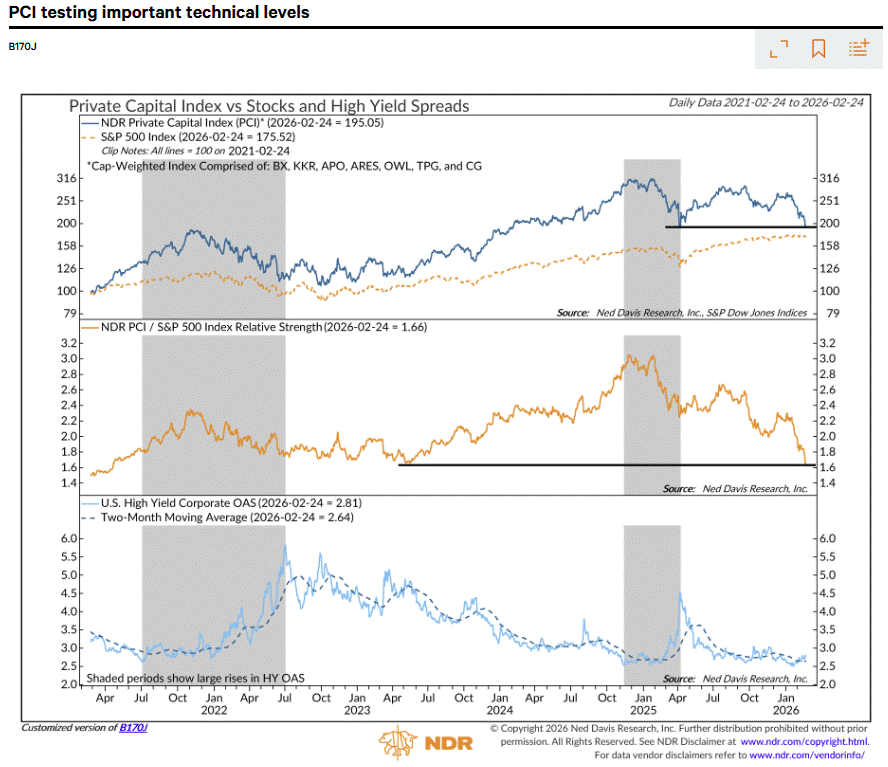

Private Credit feeling blue

Concerns over Private Credit have been bubbling up to the surface for quite some time.

Since October, following the failures of First Brands and Tricolor, several concerns have emerged:

Software exposure: fears of over-exposure to software companies that are suddenly at risk to material disruption from AI

Problems with underlying credits: after an extended period of cheap money, select loans are not working out as originally intended

Liquidity: the recent troubles with Blue Owl Capital Corporation II (OBDC II) to deliver investors accelerated liquidity splashed across major media outlets and publications, further intensifying concerns

Technical failure: the failure of these Asset Management companies in January 2026 to better their July-September 2025 peak following the April low indicated a deterioration in momentum

Valuations: even with this corrective wave, these Asset Management companies still sport loft multiples

Private Credit was hot and now it’s not. That has some parts of the financial world on edge.

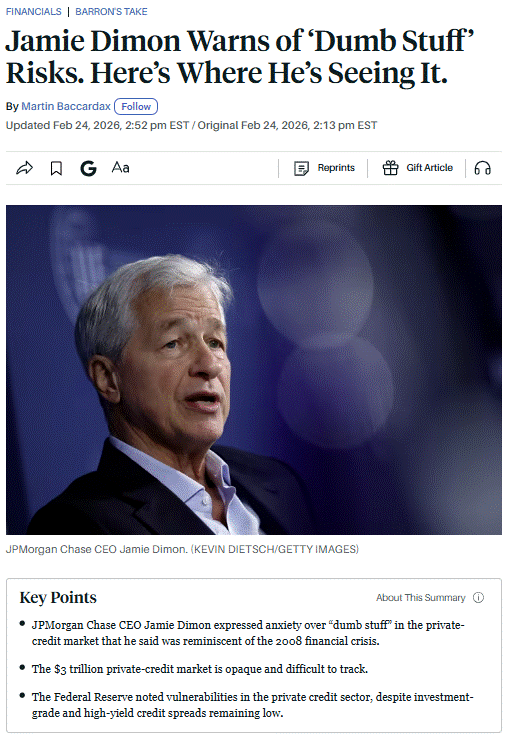

Last week, J.P. Morgan CEO Jamie Dimon piled on by warning of “dumb stuff” in the opaque private credit markets, drawing comparisons with the pre-GFC period.

Then Bloomberg reported that Boaz Weinstein of Saba Capital warned, “I think we are in the super-early innings of the wheels coming off the car.”

Even the Federal Reserve has expressed some concern about contagion in its latest minutes:

“A few participants commented that the financing of the AI-related infrastructure buildout in opaque private markets warranted monitoring.” Even more participants “highlighted vulnerabilities associated with the private credit sector and its provision of credit to riskier borrowers, including risks related to interconnection with other types of nonbank financial institutions such as insurance companies, and banks’ exposure to this sector.”

Simply put, credit worries are rising.

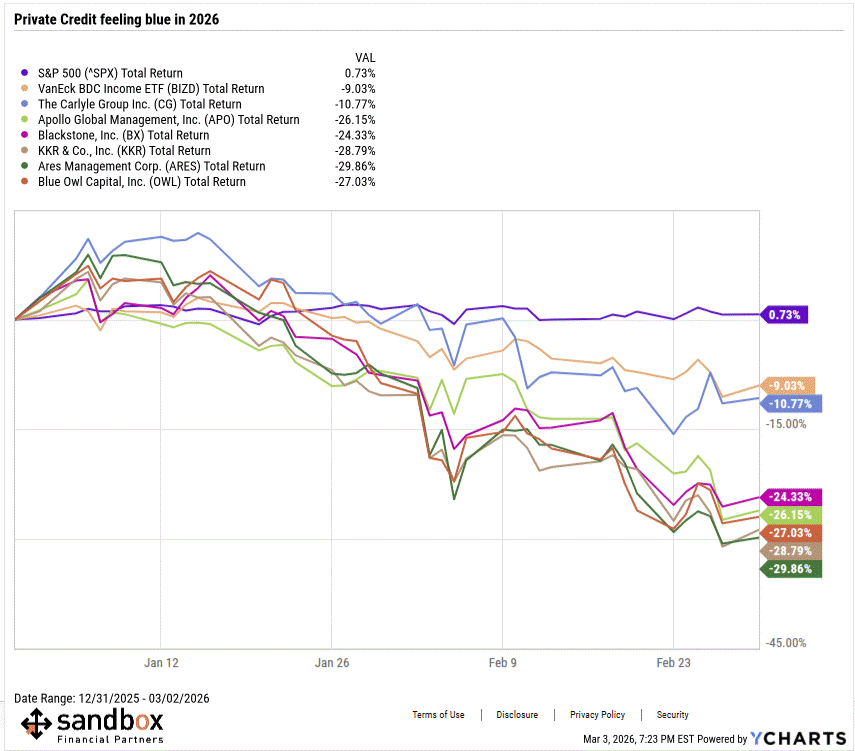

Hard to know the extent of the problem, but declining stock prices don’t exude confidence. Various Asset Management companies within the Financials subsector have taking a beating since mid-January.

These same concerns continue to show up in the prices of Business Development Companies (BDCs), as a representative ETF made another new low last week.

The converging trends of the AI boogeyman and the retail investing boom seem to be colliding at once and stressing a trillion-dollar-plus piece of the economy.

Since the Global Financial Crisis, Private Credit hasn’t really been tested by any kind of prolonged economic downturn.

And yet, barring some unexpected exogenous economic shock around the corner, I’m not seeing enough signs that a broader default cycle in Private Credit is looming imminently.

Financial conditions remain healthy, credit spreads are tight, and the U.S. consumer is resilient.

For now, this appears to be a case of rattled investors already jittery over an uncertain economy.

Sources: Ned Davis Research, Barron’s, Bloomberg, YCharts

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures (click here)

Please see our SEC Registered firm brochure (click here)

Please see our SEC Registered Form CRS (click here)