The role of housing on your personal balance sheet

The Sandbox Daily (4.27.2026)

Welcome, Sandbox friends.

Today’s Daily discusses:

the Cornerstone of Household Wealth

Let’s dig in.

Blake

Markets in review

EQUITIES: S&P 500 +0.12% | Russell 2000 +0.04% | Nasdaq 100 +0.01% | Dow -0.13%

FIXED INCOME: Barclays Agg Bond -0.15% | High Yield +0.04% | 2yr UST 3.799% | 10yr UST 4.341%

COMMODITIES: Brent Crude +2.78% to $108.26/barrel. Gold -0.91% to $4,697.7/oz.

BITCOIN: -1.04% to $76,912

US DOLLAR INDEX: -0.06% to 98.48

CBOE TOTAL PUT/CALL RATIO: 0.79

VIX: -3.69% to 18.02

Quote of the day

“Life is what happens when you’re busy making other plans.”

- John Lennon

Housing market remains a core part of both household finances and the broader economy

For many households, a home represents not only where they live and raise their family, but also their largest financial asset, monthly expense, and source of debt.

From a broader economic perspective, the housing market is deeply intertwined with economic growth, consumer confidence, the labor market, and interest rates.

So, while investor attention has been on geopolitics and market volatility this year, the fact that home prices remain near all-time highs continues to play an important role in financial planning.

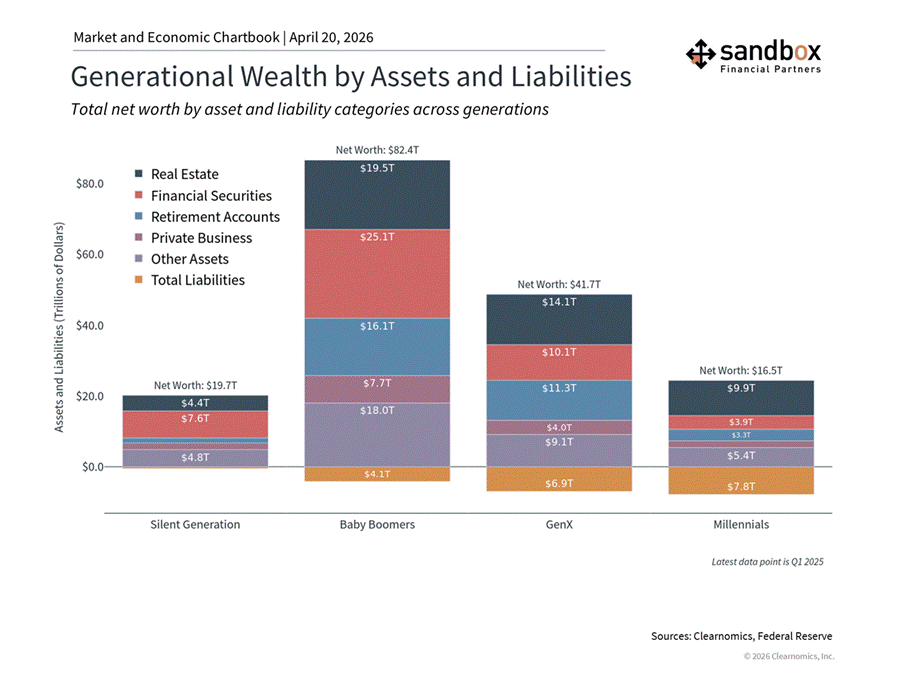

As the chart below illustrates, real estate is a hugely important component of household net worth across all generations.

For older Americans, real estate holdings often represent a significant share of total assets accumulated over decades. Baby Boomers, for instance, hold over $19.5 trillion in real estate, representing roughly 24% of their total net worth. For Gen X and Millennials, that share rises to approximately 34% and 60%, respectively.

Of course, real estate is also a significant source of outstanding debt for younger households that have not had time to pay off their mortgages or benefit from decades of housing market growth.

This “wealth effect” is important, especially when the stock market is volatile and the world feels uncertain.

When home values rise, homeowners tend to feel more financially secure and may be more willing to spend on goods and services, supporting broader economic growth. They may feel this way even if they do not actively access their home equity, such as through a reverse mortgage or home equity line of credit (HELOC).

This also highlights the importance of maintaining a holistic perspective around financial planning.

This is because short-term stock market swings, while never pleasant, are less impactful to an investor’s financial picture than they perceive in the moment, since much of their wealth is tied to other assets.

In fact, depending on the investor’s specific situation, prioritizing mortgages and other forms of debt may be more helpful than focusing on the stock market.

Inflation is another factor that is affected by housing costs, since it is the primary driver of the “shelter” category within the Consumer Price Index. Even before energy prices led to the latest jump in headline inflation, elevated shelter costs were an important reason that inflation has been slower to return to the Fed’s 2% target.

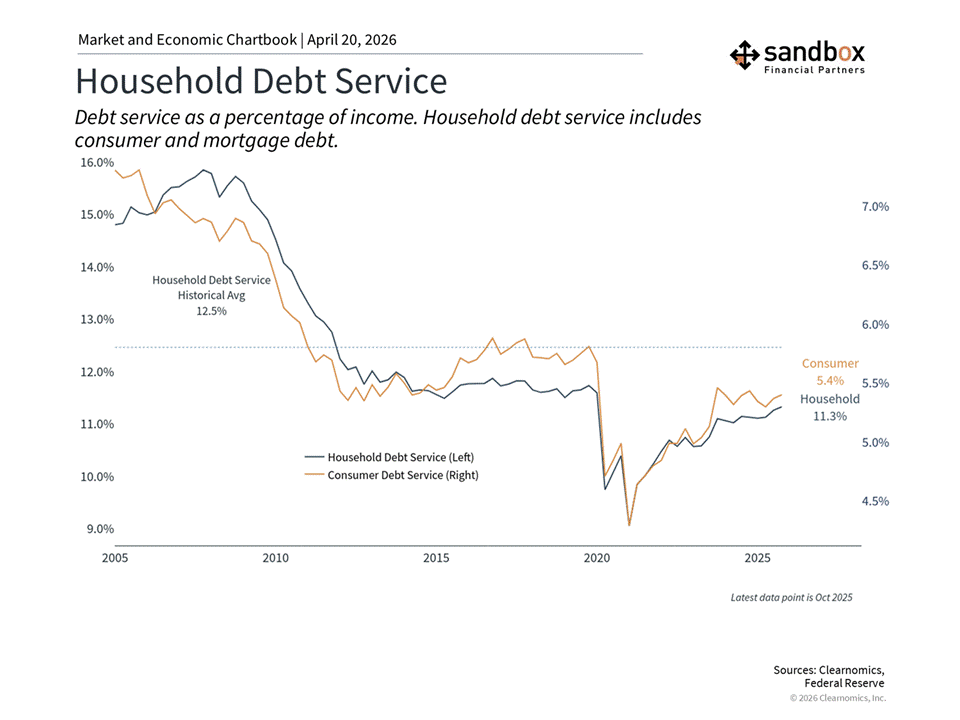

Of course, housing is not only the largest asset on most household balance sheets, but also the largest source of debt.

One encouraging aspect of today’s environment is that debt service levels (the size of debt payments relative to household income) are still moderate relative to history.

Mortgage underwriting standards have also been considerably more conservative since the 2008 Global Financial Crisis, when household debt levels were far higher.

Still, the burden of these debt payments is a real consideration for many households, particularly those who purchased homes in recent years at higher prices and interest rates.

From an economic perspective, healthy home prices could continue to support consumer balance sheets and the broader economy despite mixed activity.

From a financial planning perspective, it’s important for investors to have a clear understanding of their full financial picture – including their real estate.

While much ink has been written on stock market swings and the Middle East conflict year-to-date, the truth is that focusing on all aspects of your wealth is necessary in achieving personal long-term goals.

Source: Clearnomics

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures (click here)

Please see our SEC Registered firm brochure (click here)

Please see our SEC Registered Form CRS (click here)