Spending underpins economic strength, plus the dollar's rough month and another tenuous jobs report

The Sandbox Daily (9.4.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

spending has moderated but remains durable

the U.S. dollar’s rough month

job openings fall to lowest level since January 2021

Let’s dig in.

Markets in review

EQUITIES: Dow +0.09% | S&P 500 -0.16% | Russell 2000 -0.19% | Nasdaq 100 -0.20%

FIXED INCOME: Barclays Agg Bond +0.44% | High Yield +0.37% | 2yr UST 3.762% | 10yr UST 3.758%

COMMODITIES: Brent Crude -1.82% to $72.41/barrel. Gold +0.09% to $2,525.4/oz.

BITCOIN: -0.32% to $57,945

US DOLLAR INDEX: -0.50% to 101.317

CBOE EQUITY PUT/CALL RATIO: 0.73

VIX: +2.90% to 21.32

Quote of the day

- Peter Bernstein, via Jason Zweig’s A (Long) Chat with Peter L. Bernstein

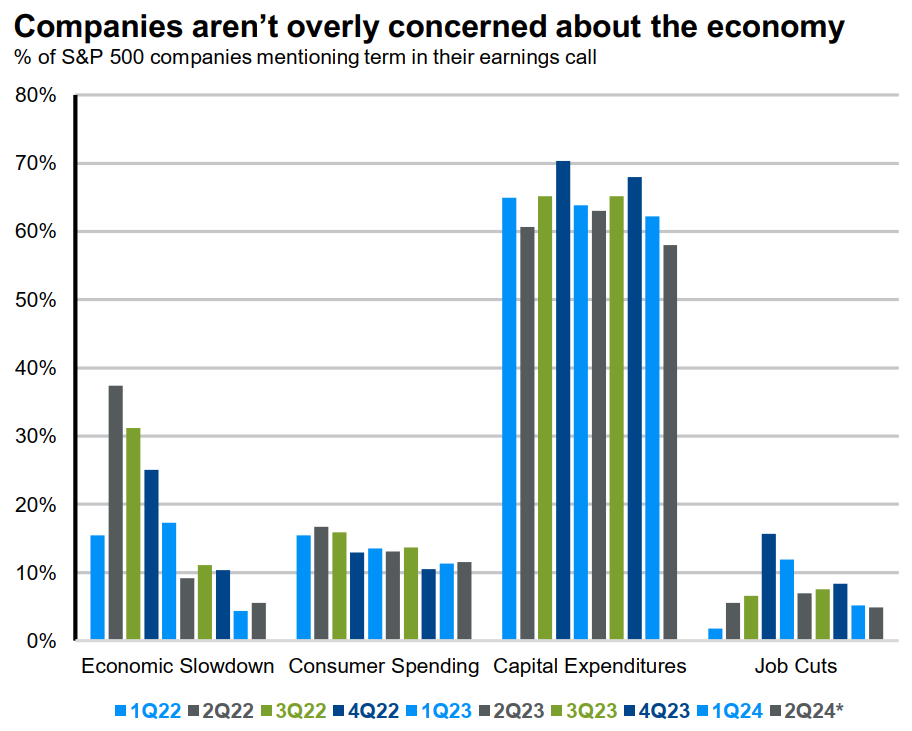

Spending has moderated but remains durable

The S&P 500 is currently battling with overhead supply – sitting just ~2.5% below all-time highs – while its underlying index constituents are on track to report 11-12% earnings growth in Q2.

Beyond the reporting numbers, earnings season provides a unique perspective for investors on the health of the economy and corporate America. Continued growth requires continued spending, and management commentary offers insight into two of the three sources of that spending: consumers and corporations.

Over the past month, companies have expressed cautious optimism. There’s been a slight uptick in mentions of an economic slowdown (albeit firmly off 2022 & 2023 levels), while consumer spending is coming a bit more into focus. The changes are small, however, and there hasn’t been much chatter about job cuts – indicating overall concern is muted from the C-Suites across America.

On the consumer side, executives have highlighted a divergence in spending behavior across income brackets. While growth remains robust at the upper-end, lower-end consumers appear increasingly value conscious. They’re still spending but just allocating dollars in a more discerning method – see our previous coverage on Retail Sales. This strong consumer spending has translated to strong corporate earnings.

At the same time, secular investment trends like AI, the energy transition, and onshoring should continue to boost capital expenditures. Balance sheets also remain robust, reducing the risk of something breaking.

Unlike typical late-cycle conditions, consumer spending has been financed by real wage growth rather than borrowing, and companies are still spending down the cash they accumulated during COVID.

In the wake of recent volatility, investors should anchor to the fundamental truth highlighted this earnings season: consumer and corporate spending is moderating but looks durable, so economic growth should be too.

Source: Fundstrat, Winfield Smart, MarketWatch, U.S. Bank

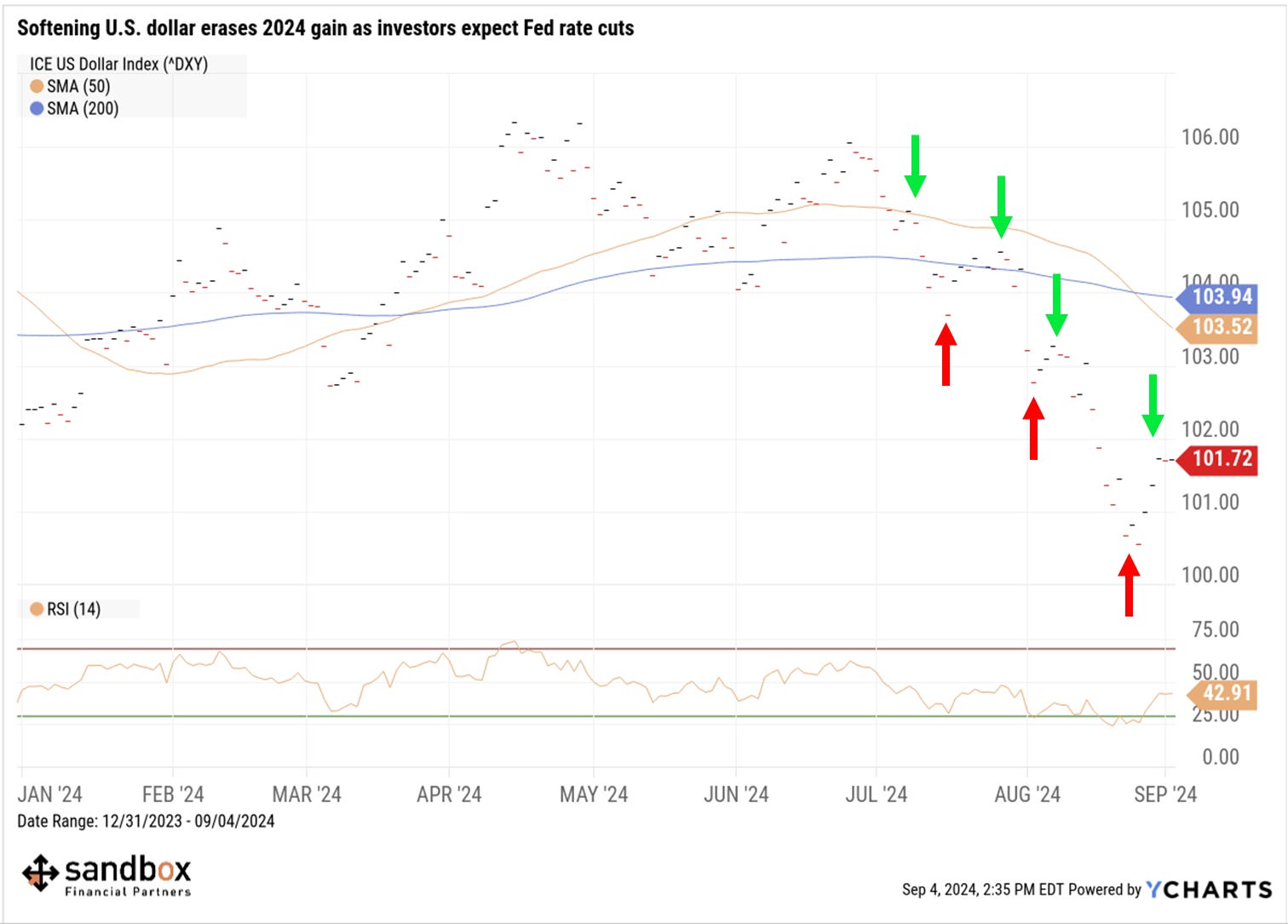

The dollar’s rough month

The U.S. dollar index ($DXY) has been under intense pressure over the last month.

It started with the sharp rise in the Japanese yen in early August, and the selloff deepened on Federal Reserve Chair Jerome Powell’s comments that the time has come to start cutting interest rates.

Each currency is closely correlated to its country’s interest rate and are quickly impacted when rates change. $DXY measures the U.S. dollar’s performance versus a basket of global currencies, so other nations’ central bank statements and economic reports affect the index as well.

Last week, the dollar index bottomed near $100.50 and rallied after a benign EU inflation report. The euro tumbled as interest rates in Europe – already a full point lower than the United States – are likely to be cut again next month.

Still, last week’s bounce in $DXY hasn’t changed anything from a longer-term trend perspective.

The index is still making lower highs (green arrows) and lower lows (red arrows). A bullish bounce was to be expected last week as the RSI momentum indicator fell firmly into oversold territory.

With rate cuts looming in the United States, the fundamental outlook for $DXY is likely bearish, lining up with the technical picture.

Assets that typically benefit from a falling dollar – think commodities, real estate, and non-U.S. equities – could see renewed interest from investors.

Source: YCharts, Eurostat, Financial Times

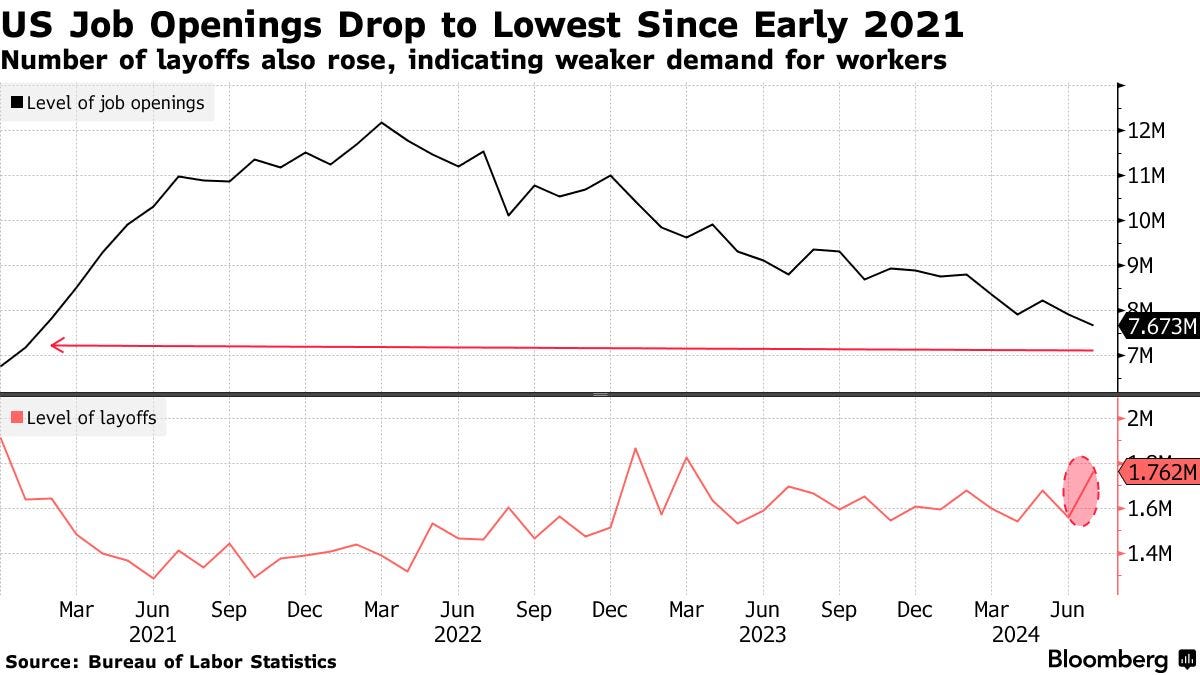

Job openings fall to lowest level since January 2021, reflects labor market in better balance

Each month, we turn to the Labor Department's Job Openings and Labor Turnover Survey (JOLTS) to understand the ebbs and flows of what's really happening among businesses and their workers.

Job openings across America decreased to 7.67 million in July from June’s downwardly revised 7.91 million reading, falling to the lowest level since January 2021 (7.19M). Job openings are down -13% from one year ago and down -37% from the peak level in March 2022.

The number of job openings has steadily declined since hitting the cyclical peak of 12.18 million vacancies in March 2022 when the Federal Reserve initiated its tightening cycle, but the number of job openings still remains ~15% higher than the 5-year period average pre-COVID (6.69M).

Meanwhile, the number of layoffs rose to 1.76 million, the highest since March 2023.

The other key metric in today’s report, the ratio of job-openings-to-unemployed-Americans, has been cut in half from its record high in 2022 to 1.07 now – well below the cycle peak of 2.03 and more or less in line with the general pre-pandemic levels and the 1.24 level in February 2020.

In simpler terms, this means there are 7.67 million job openings and 7.16 million unemployed workers.

The Fed is closely watching the progress of labor demand/supply rebalancing, and today’s report shows the labor market has certainly continued to move toward better balance. It’s yet another confirmation that labor market conditions have eased, green-lighting the start of Fed rate cuts later this month at their next policy meeting on September 17-18.

Importantly, these monthly JOLTS reports illustrate the kind of cooling that the Federal Reserve has hoped to see, with demand for workers slowing through fewer openings rather than spikes in outright job losses.

Source: U.S. Bureau of Labor Statistics, Ned Davis Research, Bloomberg, Advisor Perspectives

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.