The current bull market in context, plus inflation mentions, U.S. economic prowess, and active vs. passive

The Sandbox Daily (5.2.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

390 days and counting

fewer companies discussing “inflation” on earnings calls

U.S. economy continues to grow its share of world GDP

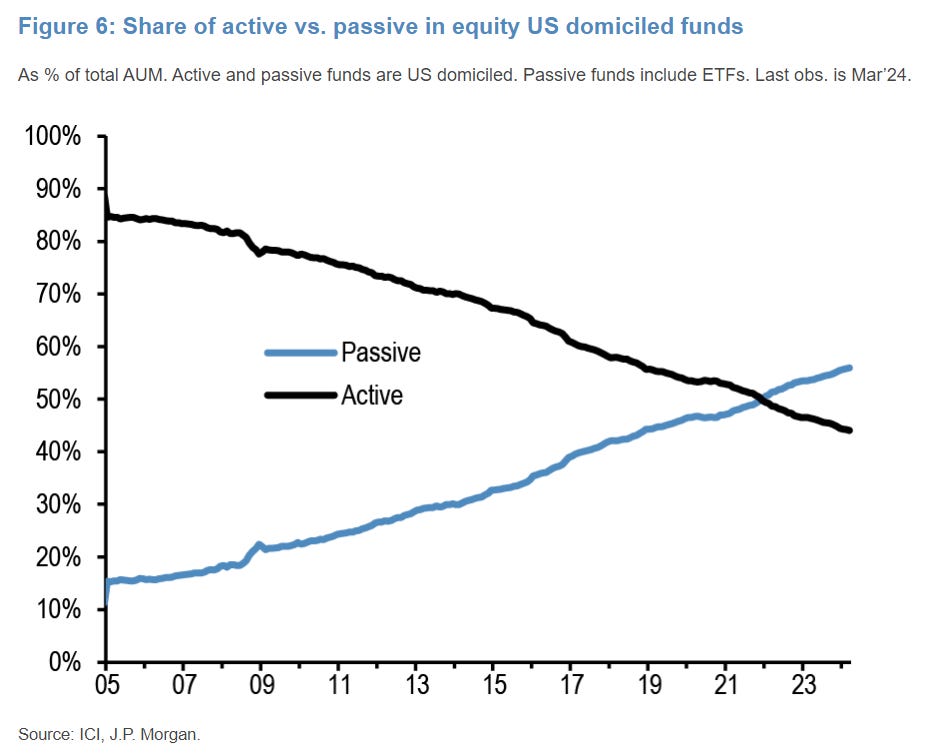

passive equity investing continues to take share from active investing

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 +1.81% | Nasdaq 100 +1.29% | S&P 500 +0.91% | Dow +0.85%

FIXED INCOME: Barclays Agg Bond +0.45% | High Yield +0.62% | 2yr UST 4.885% | 10yr UST 4.587%

COMMODITIES: Brent Crude +0.23% to $83.63/barrel. Gold +0.02% to $2,311.6/oz.

BITCOIN: +3.28% to $59,158

US DOLLAR INDEX: -0.37% to 105.360

CBOE EQUITY PUT/CALL RATIO: 0.84

VIX: -4.61% to 14.68

Quote of the day

“The future is not something we enter. The future is something we create.”

- Leonard Sweet

390 days and counting

If the current bull market ended today, it would be the shortest in post-war history!

Time is great, but investors often care more about magnitude.

The chart below shows the value of $1 invested at the previous bear market low for every bull market since WWII. The bold red line represents the current bull market. By comparison to the previous 12 bull markets, the contemporary bull has been subpar.

The present-day bull is now 390 trading days old and its return since inception of 40.7% ranks 10th out of 13. The strongest bull market at this point with a 94.5% gain was the 2020 post-pandemic run and the weakest performance was 11% in the 1946 bull market.

Source: Seth Golden

Fewer companies discussing “inflation” on earnings calls

The idea that broad inflation is reaccelerating after three straight months of upside inflation prints does not seem congruent with the messaging and data coming from Q1 earnings season.

Russell 3000 company mentions of inflation (or cost pressures) are now at 2-year lows, the same with discussions of price increases.

U.S. economy continues to grow its share of world GDP

The U.S. economy's share of the world GDP is set to reach the highest level in two decades. Since 2010, the U.S. share of global GDP has risen by about 5% and now accounts for ~26% of the world’s economy.

It’s not just stronger growth in the United States driving gains. Consider that Japan, Europe, and the United Kingdom are growing much slower and therefore losing share. China, the 2nd largest economy in the world, is showing signs it has slowed considerably. Meanwhile, India is growing rapidly but only represents a minor share of the global economy.

Source: Wall Street Journal, International Monetary Fund

Active vs. passive equity investing

The shift of tectonic plates from active to passive equity funds has been taking place for decades and the trend does not appear to be slowing.

Several factors are at play:

Cost: Passive equity funds, such as index funds and exchange-traded funds (ETFs), typically have lower fees compared to actively managed funds. These lower fees appeal to investors seeking to minimize expenses and increase their net returns.

Performance consistency: Empirical research has shown that, over the long term, actively managed funds tend to underperform their respective benchmarks after accounting for fees. Passive funds, which simply track an index, often deliver more consistent returns over time, making them an attractive option for investors seeking stability and predictability. We covered this topic previously in March (Active management is hard, really hard).

Absolute (under)performance: Actively managed funds have historically tended to underperform their benchmark over short- and long-term time horizons, irrespective of size, style, and geography. We covered this topic in January (Active manager performance) and again in March (It’s really hard to beat the market).

Transparency and simplicity: Passive funds follow a rules-based approach, often mirroring an index like the S&P 500 or the MSCI ACWI. This simplicity and transparency appeals to investors who prefer a straightforward investment approach without the complexities associated with active management strategies, or deviations in active share.

Improvements in technology: The proliferation of technology globally has not excluded disruptions to legacy financial institutions and mediums, making it easier for investors to access and invest in the market than ever before. Platforms offering commission-free trading and automated portfolio management have facilitated the growth of passive investing by reducing barriers to entry and providing simple, convenient access to a wide range of investment options.

Overall, the shift from active to passive equity funds reflects a broader trend towards cost-effective, transparent, diversified, and easily accessible investment options that align with investors' evolving preferences and expectations.

Source: J.P. Morgan Markets

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.